Mrs Justice Cockerill:

Introduction

- This is an application made during the course of long running and hard fought litigation[1] by Mr Georgy Bedzhamov on one hand and Vneshprombank LLC ("VPB") and Ms Lyubov Kireeva, his Russian trustee in bankruptcy ("the Trustee") on the other.

- The application is for declarations as to whether there is reasonable cause to suspect that A1 LLC ("A1") - a company which has to date funded VPB and the Trustee in this litigation - is owned or controlled by a designated person or persons within the meaning of Regulations 5 and 6 of the Russia (Sanctions) (EU Exit) Regulations 2019 ("the 2019 Regulations") following:

1) The designation of persons (Messrs Fridman, Khan and Kuzmichev) who were major shareholders in A1 until March 2022 and

2) Its sale (or - Mr Bedzhamov would say - apparent sale) shortly after that designation.

Mr Bedzhamov also seeks directions for the future conduct of these proceedings in light of any such declarations, including directions as to the payment and receipt of the outstanding costs order in favour of the Trustee and any future orders made in favour of the Trustee or VPB.

- Mr Bedzhamov's position is, in essence, that the litigation cannot now proceed smoothly without a determination as to whether there is reasonable cause to believe that A1 is owned or controlled by Designated Persons ("DPs"). If A1 is owned or controlled by DPs, then payments in the course of the litigation to the Trustee and VPB may benefit DPs and are therefore prohibited under the 2019 Regulations. The position of the Trustee and VPB is that no such determination is necessary, alternatively that the determination should only be made at the point which funds fall to be paid.

- The application has to some extent been prompted by judicial concerns, though it seems likely that the point would have been taken in any event, since sanctions questions have been ventilated in these proceedings as early as 2021. In the judgment [2023] EWHC 348 (Ch) (the "February 2023 Judgment") Falk LJ (sitting with Master Kaye) held (at [35]) that:

"Based on the evidence I have seen it is impossible at this stage to dispel the concern that the March 2022 transaction was not genuine, but instead arranged to give the appearance that A1 is no longer under the control of sanctioned individuals. It is important to note that the relevant regulations, the Russia (Sanctions) (EU Exit) Regulations 2019, make provision for action to be unlawful, at least without a licence, where a person either knows or has reasonable cause to suspect that the person or individual concerned is sanctioned".

- Following that expression of concern a structure was put in place for the determination of the sanctions issue in partnership with the determination of certain property issues. Matters have moved on however and this separate application was issued by Mr Bedzhamov in October 2023.

- As to the ambit of the dispute, the parties disagree on facts but also on the "trigger" for the 2019 Regulations to bite. In line with the obiter indication of Falk LJ, Mr Bedzhamov submits that dealing with funds which one has "reasonable cause to suspect" are owned or controlled by DPs is prohibited unless and until that suspicion is dispelled. The funds must be frozen in the intervening period. The Trustee and VPB say that the prohibition is only engaged if the funds are in fact proven to be owned or controlled by DPs.

- A1 LLC is no longer funding VPB or the Trustee, having been replaced by Cezar Legal Consulting Agency LLC ("Cezar") pursuant to agreements dated 27 March 2024. On 16 April those acting for Mr Bedzhamov indicated that both the proposed new funder and its third party payer are Russian companies and that further due diligence would need to be conducted before they could be satisfied that the issues before us were at all affected. On 25 April those acting for VPB indicated that the due diligence process was coming to an end and suggesting that the circulation of a draft might be delayed. That suggestion was disagreed with both by the representatives of Mr Bedzhamov and those acting for a related party in imminent litigation elsewhere. We have not been minded to delay circulation of the draft or hand down of the judgment.

- As noted on the title page, VPB and the Trustee were separately represented. However the two parties largely made common cause, dividing the submissions between Ms Barnes KC for the Trustee, who led on the issue of construction and Mr Randolph KC who dealt with the factual aspects.

Background

- The background to the wider litigation is set out in earlier judgments in this case and need not be repeated. A good understanding of it can be gleaned from reading:

1) [1]-[105] of the judgment of Snowden J [2021] EWHC 2281 (Ch);

2) The Judgment of Falk J [2022] EWHC 1166 (Ch).

It is however perhaps worth just noting that the claims are very considerable indeed, the VPB claim is pleaded at US$1.34bn.

- The critical base fact which leads to this application is that A1 is the litigation funder of VPB and the Trustee and therefore stands to obtain a financial benefit from recoveries obtained by them from Mr Bedzhamov. Part of those recoveries include the proceeds of sale from Mr Bedzhamov's interest in a property at 17 Belgrave Square and 17 Belgrave Square Mews, London, SW1X 8PG ("the Property"). That is understood to be his main asset in this jurisdiction. There have been three applications over the last three years for permission to sell this property.

- A1 is part of the Alfa Group, which was founded in 1989 and is described on its website as "one of the largest privately owned financial-investment conglomerates in Russia".

- According to Alfa Group's 2020 Annual Report, the three founders of the Alfa Group, who were described as its "main beneficial owners", are Mr Mikhail Fridman, Mr German Khan, and Mr Alexey Kuzmichev ("the Founders"). They were members of the Supervisory Board of Alfa Group.

- Also on the Alfa Group Supervisory Board are two other gentlemen who have a central role to play in this manifestation of the dispute. The first is Mr Andrei Kosogov. His biography in the Alfa Group Annual Report states this:

"Mr. Kosogov is a member of the Board of Directors of AlfaStrakhovanie Group, a member of the Board of Directors of Alfa-Bank (Russia), a member of the Board of Directors of ABH Holdings S.A., a member of the Board of Directors of Alfa-Bank (Kazakhstan) and a member of the Board of Directors of Alfa-Capital Management Company LLC. From November 2005 through June 2009, Mr. Kosogov acted as Chairman of the Supervisory Board of Alfa-Bank (Ukraine). From 2005 to 2011, Mr. Kosogov served as Chairman of the Board of Directors of Alfa Asset Management. From 2003 to 2007, Mr. Kosogov acted as Chairman of the Board of Directors of AlfaStrakhovanie Group. From 1998 to 2005, Mr. Kosogov was First Deputy Chairman of the Management Board of Alfa-Bank Russia and Director of its Investment banking division. From 1992 to 1998, Mr. Kosogov served as CEO of Alfa-Capital Management Company LLC. Mr. Kosogov graduated from the Moscow Power Engineering Institute in 1987. He was born in Sillamaё, Estonia in 1961."

- Mr Kosogov has therefore worked within the Alfa Bank business and for the Founders for over 30 years - indeed for practically all of his working life.

- The other is Mr Fayn (or Fain). Mr Fayn has been on the Supervisory Board of Alfa Group for several years. His 2020 biography states this:

"General Director of A1

Mr. Fain graduated with honors from the Moscow Institute of Chemical Engineering, Engineering Department in 1958. From 1958 until 1988, he was involved in a number of innovative engineering projects. Mr. Fain is the author of more than 70 scientific articles, manuals, books, monographs, and patents. He also holds the honorary title of active member of International Academy of Sustainable Development and holds a candidate's degree and is a professor in the field of applied mathematics. Mr. Fain is often cited by the leading Russian business periodicals as one of the most influential businessmen in Russia. He was born in Moscow, Russia in 1936."

- In his statement Mr Fayn indicates that he too has had a long association with the A1 group of companies "being CEO of A1 LLC and predecessor companies since 1992 ... associated with the group of companies A1 for over 20 years."

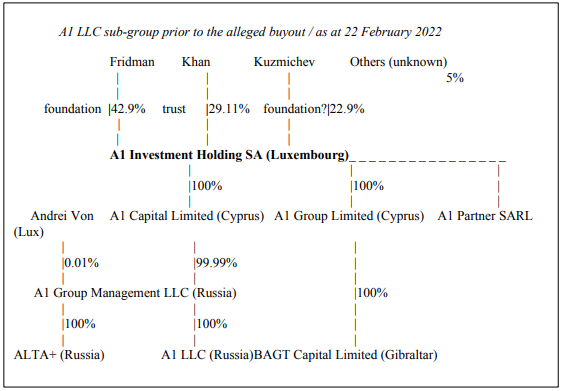

- The parties are agreed that up until March 2022, A1 was owned by a Luxembourg company called A1 Investment Holding SA ("A1 Investment"). As at 22 February 2022, the major shareholders in A1 Investment were Mr Fridman (42.9%), Mr Khan (29.11%) and Mr Kuzmichev (22.9%), with the remaining 5% held by unknown entities which are irrelevant for present purposes. Their respective shareholdings meant that no single person owned or controlled A1 Investment such that no decision could be taken by that person without the cooperation and agreement of at least one other person.

- Mr Bedzhamov's submission (which was not disputed) was that the organisation of the A1 LLC subgroup at this point can be represented thus:

- One member of the Alfa Group, Alfa Bank Russia, is a DP. A1 and A1 Investments are not DPs and are not subject to EU or UK sanctions, but they are sanctioned in the US as of 14 September 2023 "for operating or having operated in the financial services sector of the Russian Federation economy". They are also described in a US Treasury press release as "investment business of Alfa Group, a Russia-based entity connected to" the Founders.

- The Founders were all designated in the UK on 15 March 2022. Mr Kosogov and Mr Fayn are not designated. According to at least one press report Mr Kosogov has been the recipient of transfers from Mr Khan and Mr Kuzmichev of their interests in Alfa Bank and LetterOne.

- The next area of background is A1's role. It is not a typical litigation funder. It is described by the Alfa Group as "The investment business of the Alfa Group". As Falk J stated in her judgment of 5 August 2020:

"23. It is fair to say that A1's role is an unusual one that appears to go well beyond that of a conventional litigation funder. It is authorised by the DIA to manage the proceedings on its behalf. Mr Tchernenko, a senior staff member at A1, has what is described as day-to-day conduct of the proceedings, liaising as necessary with the DIA and being 'under their supervision'. Effectively, therefore, A1 is acting as the agent of the DIA (and thus VPB) for the purposes of this litigation. In particular, VPB's legal advisers take instructions from Mr Tchernenko and (at least when PCB was involved) he was said to be their primary point of client contact. I infer that, at least on a day-to-day basis, A1 are running the litigation."

- After the Trustee emerged the Trustee's application to be recognised was issued in February 2021. They appeared at their first hearing on 5 March 2022 and became involved in the proceedings. In the May 2022 Judgment, Falk J held (at [70]) that:

"I am driven to the conclusion that the Trustee's intervention was funded by A1 with a view to denying access to assets that Mr Bedzhamov (and through him his legal advisers) might otherwise reasonably have expected to have available for reasonable legal and living expenses under the WFO. I can see no other rational explanation."

- Mr Tchernenko has continued his involvement in the litigation. Ms Bloom continues to take instructions from him. He attended the hearing before us remotely. Besides being an employee of A1, he appears to be a member of A1 Law Office, an entity which, according to the Alfa Group's 2020 Annual Report, was established by A1 Investment.

- At the heart of the present dispute lies a question about the ownership and control of A1; that question arises because when the Founders were all designated in the UK on 15 March 2022, A1 was explicitly referred to in that context:

1) Mr Khan's designation referred to his role as "Chairman of the Supervisory Board of A1 Investment Holding S.A."

2) Mr Kuzmichev's designation was also updated to refer to his role on "the Board of Directors and Board of Administration of A1 Investment Holding SA" and he was also described as an involved person because he was associated with Messrs Fridman, Khan and Aven.

- It is potentially relevant background that others close to the Founders have also been sanctioned:

1) Mr Peter Aven, another member of Alfa Group's Supervisory Board was sanctioned on the same date in part because of his role as director of Alfa-Bank, which was itself sanctioned. As at the time of writing we understand that some of the EU sanctions against Mr Aven have been annulled by the CJEU, but he remains on the relevant EU Sanctions list. He also remains sanctioned by the UK and US.

2) Mr Fridman's executive assistant Ms Zairova was added to the OFSI Consolidated Sanctions List in April 2022 on the basis that she had held positions as a director of two entities owned by Mr Fridman and that "On 2 March 2022 FRIDMAN ceased to be the legal owner of both entities, together with a third entity...and on the same day ZAIROVA became the legal owner of all three entities. There is no evidence that these were arms-length transactions. As such, there are reasonable grounds to suspect that ZAIROVA is acting on behalf or at the direction of FRIDMAN." Mr Fridman like Mr Aven has had some of his EU sanctions annulled and remains sanctioned by the UK and US.

3) Mr Khan's wife, Anzhelika Khan, was designated in April 2022. The challenge to her designation was recently dismissed by Cockerill J: [2024] EWHC 361 (Admin). Ms Khan was designated not only because of her association with Mr Khan but also because she obtained financial and other material benefits from him. The judgment records these at [4] and [6], noting at [46] that "the largest and most recent gift... [in early March 2022], shortly before Mr Khan was designated and subject to an asset freeze- and with the risk of that event being the motive".

- VPB and the Trustee, have as already noted, essentially made common cause in this application and we hereafter refer to their joint submissions as those of VPB.

- VPB says that despite the designations referred to there is no sanctions issue because Messrs Khan and Kuzmichev divested themselves of ownership and control in advance of being sanctioned:

1) On or around 15 March 2022, before Mr Khan and Mr Kuzmichev were designated, they effected a sale of their shares in A1 Investment to Mr Kosogov. This is said to be an arms-length transaction whereby Mr Khan and Mr Kuzmichev did not retain any interest in or control of A1 Investment.

2) Mr Fayn purchased all of the shares in A1 from Mr Fridman, Mr Khan, Mr Kuzmichev, and Mr Kosogov on 22 March 2022 ("the MBO"). That sale, for the equivalent of £714, is hotly contentious.

- Another entity in the Alfa Group is BAGT Capital Limited ("BAGT"), a BVI company. It is not disputed that BAGT is part of the Alfa Group nor that it provided some funding in the form of loans to A1.

1) VPB is said to owe A1 US$20 million, but according to Ms Bloom for VPB, she was advised by Mr Tchernenko that "BAGT spent circa US$20 m in fees. It is entitled to recover that money from A1 LLC only if and when A1 LLC makes a recovery in the VPB claim". A1 therefore owes a large debt to BAGT.

2) As at 14 October 2020 A1 had made payments totalling £4,275,000 into court by way of security for costs, in addition to the £1m fortification for the Search Order. There was in the hearing before us some suggestion that at least some of this sum was financed by BAGT.

- The parties disagree as to the continued relevance of BAGT to the question of the ownership and control of A1. VPB contends that BAGT's involvement ceased before March 2022. Mr Fenwick does not contest that, but he argues that the debt owed to BAGT is significant for the purposes of determining A1's relationship with the Alfa Group today.

- Sanctions had been a live issue between the parties since about 2021 and came increasingly into focus after March 2022. Following the judgment of Miles J (sitting with Master Kaye) dated 16 June 2023 [2023] EWHC 348 (Ch) an order sealed on 19 July 2023 put in place a timetable for the determination of the sanctions issue as part of dealing with the issues in relation to the sale of the Property including the use and distribution of the sale proceeds. Any application was to be filed by 21 days from the Trigger Date defined in that Order as being "either the date on which the contractual documentation is agreed between the parties or any dispute as to the sale documentation is resolved by the Court." Neither event has happened to date, though an agreement was said to be in its final stages of formalisation.

The Legal Background

- The background to the UK sanctions regime is addressed in the judgments of Cockerill J in PJSC National Bank Trust v Mints [2023] EWHC 118 (Comm) ("Mints"), the Court of Appeal in the same case [2023] EWCA Civ 1132 and Garnham J in Shvidler v Secretary of State for Foreign, Commonwealth, and Development Affairs [2023] EWHC 2121 (Admin).

- The key instrument for present purposes is the Russia (Sanctions) (EU Exit) Regulations 2019 ("the 2019 Regulations"). Regulation 5 grants the Secretary of State the power to designate persons for the stated purposes.

- Regulation 6 ("Designation criteria") provides as relevant:

"(1) The Secretary of State may not designate a person under regulation 5 (power to designate persons) unless the Secretary of State—

has reasonable grounds to suspect that that person is an involved person, and...

(2) In this regulation, an "involved person" means a person who—

is owned or controlled directly or indirectly (within the meaning of regulation 7) by a person who is or has been so involved..."

- Regulation 7 defines the concept of "owned or controlled directly or indirectly":

"(1) A person who is not an individual ("C") is "owned or controlled directly or indirectly" by another person ("P") if either of the following two conditions is met (or both are met).

(2) The first condition is that P—

(a) holds directly or indirectly more than 50% of the shares in C,

(b) holds directly or indirectly more than 50% of the voting rights in C, or

(c) holds the right directly or indirectly to appoint or remove a majority of the board of directors of C.

(3) Schedule 1 contains provision applying for the purpose of interpreting paragraph (2).

(4) The second condition is that it is reasonable, having regard to all the circumstances, to expect that P would (if P chose to) be able, in most cases or in significant respects, by whatever means and whether directly or indirectly, to achieve the result that affairs of C are conducted in accordance with P's wishes."

- Regulation 7(2) is to be interpreted in line with Schedule 1. Paragraph 3 of Schedule 1 ("Joint arrangements") provides:

"(1) If shares or rights held by a person and shares or rights held by another person are the subject of a joint arrangement between those persons, each of them is treated as holding the combined shares or rights of both of them.

(2) A "joint arrangement" is an arrangement between the holders of shares or rights that they will exercise all or substantially all the rights conferred by their respective shares or rights jointly in a way that is pre-determined by the arrangement".

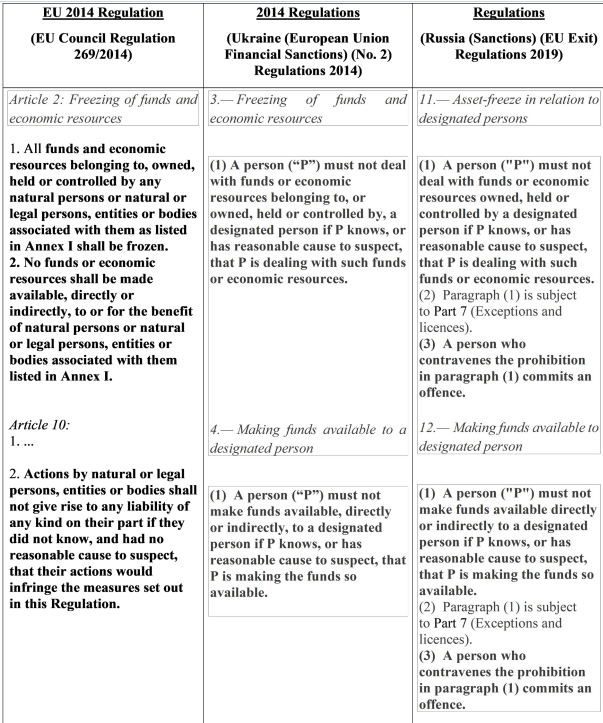

- The correct interpretation of Regulation 11 ("Asset-freeze in relation to designated persons") is the main focus of the argument. The foundation of the argument is that if A1 was owned or controlled by a DP, dealing with funds paid by the Trustee and/or VPB would engage Regulation 11 which provides:

"(1) A person ("P") must not deal with funds or economic resources owned, held or controlled by a designated person if P knows, or has reasonable cause to suspect, that P is dealing with such funds or economic resources....

(3) A person who contravenes the prohibition in paragraph (1) commits an offence."

- Regulations 12 to 15 (which are materially identical to each other for present purposes) may likewise be engaged if Mr Bedzhamov pays money to the Trustee and/or VPB - as is a distinct possibility in the circumstances outlined above.

- Regulation 12 ("Making funds available to designated person") provides:

"(1) A person ("P") must not make funds available directly or indirectly to a designated person if P knows, or has reasonable cause to suspect, that P is making the funds so available....

(3) A person who contravenes the prohibition in paragraph (1) commits an offence.

(4) The reference in paragraph (1) to making funds available indirectly to a designated person includes, in particular, a reference to making them available to a person who is owned or controlled directly or indirectly (within the meaning of regulation 7) by the designated person."

- Other parts of the Regulations to which reference was made in argument were Regulations 25, 64 and 70.

- Regulation 25 ("Making available or acquiring restricted goods and restricted technology") was relied upon for its contrasting drafting:

"(1) A person must not—

directly or indirectly make [restricted goods] or [restricted technology] available to a person connected with Russia;

directly or indirectly make [restricted goods] or [restricted technology] available for use in Russia;...

(3) A person who contravenes a prohibition in paragraph (1) commits an offence, but—

(a) it is a defence for a person charged with an offence of contravening paragraph (1)(a) or (c) ("P") to show that P did not know and had no reasonable cause to suspect that the person was connected with Russia;

(b) it is a defence for a person charged with the offence of contravening paragraph (1)(b) to show that the person did not know and had no reasonable cause to suspect that the goods or technology were for use in Russia; ..."

- Regulation 64 ("Treasury licences") states:

"(1) The prohibitions in regulations 11 to 15 (asset-freeze etc.) ... do not apply to anything done under the authority of a licence issued by the Treasury under this paragraph...

(2) The Treasury may issue a licence which authorises acts by a particular person only—

in the case of acts which would otherwise be prohibited by regulations 11 to 15, where the Treasury consider that it is appropriate to issue the licence for a purpose set out in Part 1 of Schedule 5, F14..."

- Schedule 5 ("Treasury licences: purposes") Part 1 ("Asset-freeze etc.") includes:

"Legal services

(3) To enable the payment of—

(a) reasonable professional fees for the provision of legal services, or

(b) reasonable expenses associated with the provision of legal services."

- Regulation 70 ("Finance: reporting obligations") sets out the circumstances under which a report must be made to the Treasury:

"(1) A relevant firm must inform the Treasury as soon as practicable if—

(a) it knows, or has reasonable cause to suspect, that a person—

(i) is a designated person, or

(ii) has committed an offence under any provision of Part 3 (Finance) ..., and

the information or other matter on which the knowledge or cause for suspicion is based came to it in the course of carrying on its business.

(1ZA) A relevant firm must also inform the Treasury as soon as practicable if—

(a) it knows, or has reasonable cause to suspect, that it holds funds or economic resources for a prohibited person; and

(b) the information or other matter on which the knowledge or cause for suspicion is based came to it in the course of carrying on its business.

(1ZB) Where the relevant firm knows, or has reasonable cause to suspect, that it holds funds or economic resources for a prohibited person, it must by no later than 31st October in each calendar year, provide a report to the Treasury as to the nature and amount or quantity of those funds or economic resources held by that firm as of 30th September in that calendar year."

- OFSI has issued General Guidance on Financial Sanctions (updated on 13 February 2024) (the "OFSI Guidance"), on which reliance was placed in particular by Mr Bedzhamov. The Guidance states at 3.1.2 under the heading "What you must do":

"If you know or have "reasonable cause to suspect" that you are in possession or control of, or are otherwise dealing with, the funds or economic resources of a designated person you must:

· Freeze them

· Not deal with them or make them available to, or for the benefit of, the designated person, unless there is an exception in the legislation that you can rely on or you have a licence from OFSI

· Report them to OFSI (see Chapter 5 of this guidance)

Reasonable cause to suspect refers to an objective test that asks whether there were factual circumstances from which an honest and reasonable person should have inferred knowledge or formed the suspicion."

- Ownership and Control is addressed at 4.1. As to minority interests, the OFSI Guidance states at 4.1.2 that:

"If a designated person has a minority interest in another entity, this does not necessarily mean that financial sanctions also apply to them as the ownership and control criteria may not have been met. It will be necessary to consider whether a designated person is in control - for example, because the affairs of the entity are conducted in accordance with the designated person's wishes. If they are, then the ownership and control criteria will be met."

- As to Joint Interests, the OFSI Guidance states at 4.1.3 that:

"If two or more persons hold shares or rights jointly, each of them will be treated as owning those shares or rights. This also applies to joint arrangements where all holders of shares or rights exercise their rights jointly. In this case, all parties subject to the joint arrangement are considered as owning those shares or rights."

- As to Aggregation, the OFSI Guidance states at 4.1.4 that:

"When making an assessment on ownership and control, OFSI would not simply aggregate different designated persons' holdings in a company, unless, for example, the shares or rights are subject to a joint arrangement between the designated parties or one party controls the rights of another. Consequently, if each of the designated person's holdings falls below the 50% threshold in respect of share ownership and there is no evidence of a joint arrangement or that the shares are held jointly, the company would not be directly or indirectly owned by a designated person.

It should be noted that ownership and control also relates to holding more than 50% of voting rights, the right to appoint or remove a majority of the board of directors and it being reasonable to expect that a designated person would be able in significant respects to ensure that the affairs of a company are conducted in accordance with their wishes. If any of these apply, the company could be controlled by a designated person."

- Paragraph 5.1.1 of the OFSI Guidance states that Relevant firms (as defined in the Regulations) must inform OFSI as soon as practicable "if they know or reasonably suspect a person is a designated person".

The Issues

- There are two main issues.

1) The issue of construction. Does the Regulation engage if there is reasonable ground to suspect that an entity is owned or controlled by a sanctioned person or entity? Or is that question not relevant until or unless it is proved that there was as a matter of fact such ownership and/or control?

2) The issue of fact: If the former is the correct construction, is there, on the facts here, reasonable grounds to believe that A1 remains controlled by the sanctioned former owners?

- There is then a contingent further issue which arises if the latter construction is correct: is the regulation nonetheless engaged because the Court can and should conclude that A1 remains controlled by the sanctioned former owners?

- The extent to which it is appropriate or necessary to decide all of these issues will be considered further below.

The Law

- The first issue obviously requires an exercise of statutory construction. Those principles (which apply to delegated legislation as well as to primary legislation) have been set out in my judgment in Mints [2023] EWHC 118 (Comm) [64], approved by the Court of Appeal at [2023] EWCA Civ 1132 [185].

- The other points on which reliance were placed by the parties were not contentious. They were:

1) When looking at legislative intent in the legislative context, "context" means the entire statutory scheme within which the particular provision is contained. See, e.g. Rossendale BC v Hurstwood Properties (A) Ltd [2022] AC 690, 704F-G [16] (Lord Briggs and Lord Leggatt warning against "tunnel vision" in statutory interpretation);

2) The Court should "seek to avoid a construction of a statutory provision that produces an absurd result, since this is unlikely to have been intended" by the legislator. Secretary of State for Work and Pensions v Johnson [2020] EWCA Civ 778 at [48]; R v McCool [2018] UKSC 23, [2018] 1 WLR 2431 at [24]-[25] (per Lord Kerr);

3) "Absurdity" includes "virtually any result which is impossible, unworkable or impracticable, inconvenient, anomalous or illogical, futile or pointless, artificial, or productive of a disproportionate counter-mischief". Bennion, §13-1. However it is a high test. On the authorities (in particular SSWP v Johnson and R v McCool) it appears that, to be absurd, a construction has to wholly undermine the statutory scheme;

4) Statutory provisions are presumed not to be otiose or redundant. Bennion, paragraph 1.53;

5) Where Parliament or delegated legislation has used broad terms, these will generally be construed broadly. General words are to be understood generally. Bennion §356;

6) The Crown is not bound by a statutory provision except by express words or necessary implication. R (Black) v Secretary of State for Justice [2018] AC 215, [36] (Baroness Hale, PSC);

7) The English approach to statutory construction places more weight on language, in contrast to the European approach which places greater emphasis on purpose. Ministry of Defence and Support for Armed Forces of the Islamic Republic of Iran v International Military Services Limited [2019] EWHC 1994, [2019] 1 WLR 6409 at [37]; R (Certain Underwriters of Lloyd's London) [2021] 1 WLR 387 at [34].

- There is also some uncontentious relevant law on the subject of the test of "reasonable cause to suspect":

1) The test imports an objective element requiring an evidential foundation. R v Lane and Letts [2018] UKSC 36 at [22] and [24], identifying the objective nature of the standard in the context of the terrorist financing offence in s.17 of the Terrorism Act 2000;

2) It must be fact-based and genuinely reasonable. R (Ahmed) v HM Treasury [2009] 3 WLR 25, [135] (Sedley LJ);

3) It requires that on the available information, a reasonable person would, not might or could, suspect that in e.g., a Regulation 11 case, a person whose funds or economic resources are dealt with is a designated person within the meaning of the Regulations. R v Lane and Letts [24]; R (Ahmed) v HM Treasury [136] where Sedley LJ described the 'may be' test as "on any rational view, a bridge too far";

4) The question whether there are reasonable grounds to suspect must be considered in the round, in a fair-minded review which takes into account all relevant information including undermining material and initial suspicions may be dispelled by information or evidence which undermines what might otherwise be reasonable grounds. National Crime Agency v Baker & Ors [2020] EWHC 822 (Admin) (Lang J);

5) It is necessary to guard against making unreliable assumptions and to exercise caution in treating complexity of corporate structures as grounds for suspicion. NCA v Baker [95]-[100];

6) The accuracy and credibility of the sources of evidence relied upon should be evaluated and verified, although such evidence is not limited to that which would be admissible in court. LLC Synesis v Secretary of State for Foreign, Commonwealth and Development Affairs [2023] EWHC 541 (Admin) (Jay J) at [73] "the Court will normally expect that at least some recognition has been given to its inherent quality";

7) R (Rawlinson & Hunter Trustees) v Central Criminal Court; R (Tchenguiz & Or) v Director of the Serious Fraud Office [2013] 1 WLR 1634, [89]: whether a statutory test of reasonable suspicion is met must be carefully considered and the applicant's presentation subject to rigorous and critical analysis.

8) Speculation as to continued control by a DP over a non-designated entity does not establish a triable case of such continuing control. Litasco SA v Der Mond Oil and Gas [2023] EWHC 2866 (Comm) [63]-[64].

Issue 1: The Issue of Construction

- It was contended for Mr Bedzhamov that Regulations 11, 12 and 14 clearly prohibit a person ("P") from: (a) dealing with funds or economic resources, owned, held or controlled by a DP if P knows, or has reasonable cause to suspect, that P is dealing with such funds or economic resources; (b) making funds or economic resources available directly or indirectly to a DP, if P knows, or has reasonable cause to suspect that P is making such funds or economic resources available. It was contended that the legislative text is clear, that the reasonable cause approach is supported by the primary purpose of the regulations (to freeze assets) and that this interpretation of the Regulations is supported by:

1) The OFSI Guidance at 3.1.2;

2) The White Paper on the United Kingdom's future legal framework for imposing and implementing sanctions (April 2017) (at p.24):

"Businesses have a responsibility to freeze accounts and other financial products if they know or have reasonable cause to suspect that they are in possession or control of funds or economic resources of a sanctioned person."

3) OFSI's Guidance on Enforcement and Monetary Policies:

"In the regulations the prohibitions will specify that a prohibition is breached where the person knew or had reasonable cause to suspect that they were in breach of the relevant prohibition."

4) Other materials including the FCA guidance dated 28.03.22 and the Law Society Guidance dated 12.12.23, itself referring to the OFSI Guidance.

- The net result in Mr Bedzhamov's submission was that any person who has prima facie reasonable cause to suspect must freeze the assets or commit the offence unless it is possible to dispel the suspicion. If it is not possible to dispel the suspicion "you must put some kind of temporary freeze on until you either get satisfactory evidence or the matter goes before a court or arbitrator." It was said that to conclude otherwise would be to create a trap because a person who has reasonable cause to suspect A is controlled by a DP would not have a basis to refuse to deal with A; but could later be found to have committed a criminal offence if it were concluded that A was in fact owned or controlled by a DP.

- Although the argument was skilfully put, we have no hesitation in concluding that it is wrong. The starting point, as made clear in the authorities cited above, is the words. Regulation 11 says this:

"(1) A person ("P") must not deal with funds or economic resources owned, held or controlled by a designated person if P knows, or has reasonable cause to suspect, that P is dealing with such funds or economic resources.

(2) ...

(3) A person who contravenes the prohibition in paragraph (1) commits an offence."

- The natural reading of that is in line with the arguments advanced for VPB/the Trustee. The key passage is the beginning of the regulation: "A person ("P") must not deal with funds or economic resources owned, held or controlled by a designated person".

- The construction urged by Mr Bedzhamov is some distance from that wording. Indeed it was pointed out by VPB that if Mr Bedzhamov was correct, it would require the statutory provisions to be read as follows, using Regulation 11 as an example ("read in" text underlined):

"(1) A person ("P") must not deal with funds or economic resources owned, held or controlled by a designated person if P knows, or has reasonable cause to suspect, that P is dealing with such funds or economic resources owned, held or controlled by a designated person.

(2) ...

(3) A person who contravenes the prohibition in paragraph (1) commits an offence."

- Mr Bedzhamov did not contend that this version did not accurately reflect his construction.

- Putting the two versions so close together makes the point: this is a significant difference. It is unimaginable that experienced legislative drafters would have put forward the first version if what they were seeking to put in place was the latter.

- So much for the first iteration of the construction exercise. But the matter only becomes clearer as one progresses.

- Perhaps the most telling point was that if Mr Bedzhamov were right, Regulations 11-15 would prohibit dealing with funds or economic resources held by a person in respect of whom there are reasonable grounds to suspect is, but who in fact is not, a DP (or owned or controlled by a DP within the meaning of Regulation 7); and that a person who did so would, under Regulation 19, be liable for conviction on indictment - a conviction punishable with up to seven years' imprisonment.

- As VPB rightly says, this would represent a "monumental extension of criminal liability" and would self-evidently offend against the principle of strict interpretation of penal legislation. It was pointed out that there is no offence known to English law of thwarting a purported intention of legislation. As Lord Diplock put it in R v Bhagwan [1972] AC 60, 80H-81A and p82H:

"My Lords, I know of no authority which would justify your Lordships in holding it to be a criminal offence for any person, whether or not acting in concert with others, to do acts which are neither prohibited by Act of Parliament nor at common law, and do not involve dishonesty or fraud or deception, merely because the object which Parliament hoped to achieve by the Act may be thereby thwarted."

- It was also submitted that were Mr Bedzhamov's construction to be favoured, this would be to overstep constitutional boundaries and make new law. This point was dealt with at length by VPB but it was not squarely engaged with by Mr Bedzhamov. Two responses, neither of them persuasive, were advanced.

- The first was to say that the requirement in Regulation 11 that the funds or economic resources be owned, held or controlled by a DP is, instead, a defence to the criminal offence rather than part of the prohibition and an element of the offence. This contention is not supported by the statutory wording.

- There is also a burden of proof issue which engages fundamentally with the nature of criminal liability and which is perhaps not instinctive to those who primarily inhabit civil proceedings. In criminal proceedings the burden of proof generally lies on the prosecution; but where defences are concerned it shifts to the defendant. Therefore, defences in criminal legislation are clearly framed as such so that where a requirement (as to fact or a mental element) is a defence, it is clear to the defendant what they have to prove. Ms Barnes KC referred us to a number of examples. One of these was article 7 of the Terrorism (United Nations Measures) Order 2006, one of the statutory instruments at issue in Ahmed v HM Treasury [2010] 2 AC 534:

"Freezing funds and economic resources of designated persons

7(1) A person (including the designated person) must not deal with funds or economic resources belonging to, owned or held by a person referred to in paragraph (2) unless he does so under the authority of a licence granted under article 11 ...

(4) In proceedings for an offence under this article, it is a defence for a person to show that he did not know and had no reasonable cause to suspect that he was dealing with funds or economic resources belonging to, owned or held by a person referred to in paragraph (2)."

There one can see the offence and defence clearly and separately delineated.

- Mr Bedzhamov's contention that the "reasonable cause to suspect" operates as a defence to the criminal offence therefore also offends the principle of strict interpretation of penal legislation because it would shift the burden of proof onto the individual, thereby reading down the criminal law protections which the legislator provided to that individual.

- Mr Bedzhamov's second response was to argue that this was not a problem because a breach of this prohibition falls outwith the enforcement regime of the Regulations. That is an unattractive approach for all sorts of reasons. Amongst them is the fact that this does not of course evade the problem with the prohibition against doubtful penalisation. But also, if this were correct, this would (i) establish a set of prohibitions within Regulations 11-15 shorn of any enforcement mechanism; (ii) require different readings of same words within the prohibitions dependent upon situation; (iii) be inconsistent with the previous EU and UK implementing regulations; and (iv) be rooted only on a particular reading of non-statutory OFSI guidance.

- The point is rendered in our judgment absolutely conclusive against Mr Bedzhamov when one considers the history of the relevant measures. This lies in the 2014 EU Regulations from which, as was noted by the Court of Appeal in Mints, the 2019 Regulations derive. And, as the Court recorded at [189]:

"The intention of Parliament and the Government was to continue the EU regime without substantive change and "differences are to be explained as putting the same thing differently".

- Article 2 of the 2014 EU Regulation required Member States to freeze "[a]ll funds and economic resources belonging to, owned, held or controlled by [DPs]" and ensure "[n]o funds or economic resources shall be made available, directly or indirectly, to or for the benefit of [DPs]". Thus it is perfectly clear that in the EU Regulations from which the Regulations derive, the test as to ownership and control was (and is) a purely factual test. It did not prohibit the dealing with (or provision etc of ) funds or economic resources to persons in respect of which there was only reasonable cause to suspect they were DPs. The mental element of knowledge or reasonable cause to suspect was introduced separately (in Article 10(2)) as a requirement before a person could be liable for a breach of the asset freezing measures in Article 2: "Actions by natural or legal persons, entities or bodies shall not give rise to any liability of any kind on their part if they did not know, and had no reasonable cause to suspect, that their actions would infringe the measures set out in this Regulation". It is worth pausing here to note that this provision makes clear that no liability arises unless (i) ownership in fact and (ii) knowledge or reasonable cause to suspect. This is the antithesis of liability diluted by either defence or non-enforcement.

- This wording therefore makes clear that the 2014 EU Regulation bites on funds in fact controlled etc by DPs. Regulations 3 and 4 of the 2014 UK Regulation (the Ukraine (European Union Financial Sanctions) (No 2) Regulations) implemented these prohibitions with the required mental element rolled up into the one Regulation. Those regulations are then in substantially the same terms as Regulations 11 and 12 of the 2019 Regulations. The continuum of statutory approach is illustrated in the table attached to this judgment as Appendix 1.

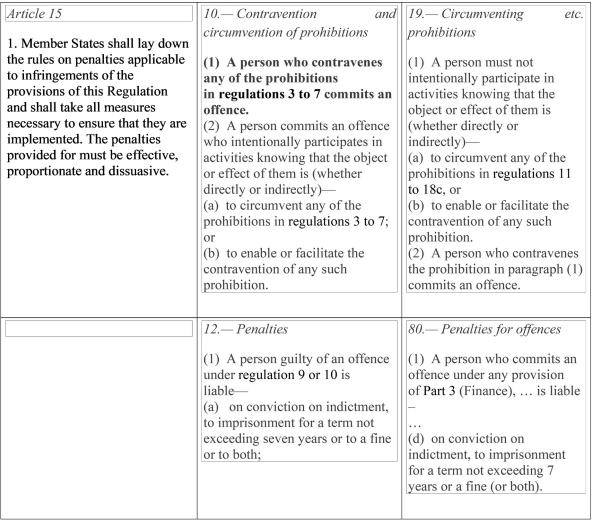

- The second part of the EU regime which is relevant is Article 15(1) of the 2014 EU Regulation which required Member States to establish an enforcement regime of "penalties applicable to infringements of the provisions of this Regulation ...[which] must be effective, proportionate and dissuasive." This was an obligation to ensure that all breaches of the prohibitions were enforceable through a penalty scheme. That is what the UK implemented through Regulations 10 (the offence creating provision) and 12 (penalties) of the 2014 UK Regulations.

- The 2019 Regulations implement this same scheme, albeit with the offence creating provisions in each of the relevant regulations which establish the relevant prohibition (Regs 11-15) and only the circumvention offence contained within a separate regulation (Reg 19). Regulation 80 provides the same maximum penalty following conviction on indictment (7 years imprisonment). Mr Bedzhamov's suggestion that the Regulations now also contain a new prohibition to which a penalty does not attach is inconsistent with this EU and pre-Brexit background and the Parliamentary intent to continue the EU regime without substantive change.

- With such a clear route demonstrated, the argument as to the impact of the Guidance is doomed to fail. Guidance can be significant in interpreting legislation - but whether it is or not depends upon the Guidance. In Mints [2023] EWHC 118 (Comm) [171] part of this court rejected reliance on the same OFSI guidance as being not "the kind of reasoned Guidance" which may provide "comfort or any pause for thought". The reasons why were helpfully unpicked for us in argument: it is not the kind of Guidance which actually analyses the provisions, it is ex post facto and it appears (on examination of its genesis) to have been based on a draft of the provisions which was different to the form of prohibitions ultimately enacted. The point is similar to that made by Lord Sales in PACCAR Inc & Ors.) v Competition Appeal Tribunal & Ors [2023] UKSC 28 at [94]:

"In my judgment this principle does not apply where the later legislation sought to be relied on is subordinate legislation made by the executive rather than an Act of Parliament. Therefore it does not authorise use of the DBA Regulations 2013 as an aid to interpretation of the 2006 Act. If the position were otherwise, it would undermine the emphasis given in the authorities to the importance of subordinate legislation being broadly contemporaneous with the primary legislation which falls to be interpreted: paras 44—47 above. It would also confer an unjustified power on the executive to take action later on which might modify the meaning which is given to words used in earlier primary legislation."

- Nor can the argument by reference to Regulation 70 make any difference. As Ms Barnes submitted, it is erroneous to elide Regulation 70, which has a different purpose, with the earlier regulations.

- It follows that we conclude that the correct construction is clearly that contended for by VPB. There is therefore no need to address the other iteration of the argument advanced for VPB by reference to the actus reus and mens rea of the offence. That argument aligned with, but did not seem to add significantly to, the argument.

Issue 2: Reasonable Cause to Suspect?

- In one sense therefore the "reasonable grounds to suspect" argument becomes irrelevant; and indeed it was VPB's submission that we should only deal with this point if we reached the conclusion that there was no reasonable cause to suspect.

- For VPB the submission was made that while it would be of utility to the parties to know whether there was not reasonable cause to suspect ownership and control, it was not helpful at this stage to decide the point. That is because even if the question of ownership were determined or the construction point went the other way, it is a question which in practical terms would only have utility judged at the time when any payment came to be made - for example in the context of distribution issues or in relation to costs. It is the situation then which would determine whether the regulations would be engaged and would bite upon the parties.

- We are of course very alive to the question of the purpose of the present aspect of the decision in isolation and at this point. However, that approach - the half way house of dealing with the negative conclusion only is unworkable. In essence if we adopted that approach we would be dealing with the point explicitly if we reached a negative conclusion, and tacitly (by failing to deal with it) if we reached a positive conclusion. The correct approach must be either to stop at the issue of construction, or to decide the point - in either direction. Even if a positive conclusion cannot be dispositive it can provide guidance and may provide a further court with the means of abbreviating (and hence expediting) its decision.

- There are two other reasons for dealing with the point. The first is that in circumstances where Mr Bedzhamov did not accept that the application must fail if we reached this conclusion, but instead doubled down and invited the conclusion that the factual test of ownership or control was met, it is appropriate to consider the reasonable grounds test, essentially as a stepping stone to the factual conclusion sought. The second is of course the possibility of a contrary view being taken on the prior point on appeal - remote though we may consider that contingency to be.

- The argument on reasonable grounds to suspect was advanced by reference to a number of threads of the evidence. It was said that:

1) There is reasonable cause to suspect that there was a joint arrangement between Messrs Fridman, Khan and Kuzmichev before or at the time of the Alleged Buy Out, such that their share ownership of A1 Investment should be aggregated, and each of them is to be treated as holding the combined shares of all three. There is therefore reasonable cause to suspect that A1 Investment and A1 were owned or controlled by a DP or DPs at the time of the Alleged Buy Out;

2) The factual circumstances of the Alleged Buy Out (including the purported change in ownership of A1 Investment around the same time on undisclosed terms) strongly suggest that the Alleged Buy Out was not a genuine and arms' length transaction but instead a sham, designed to circumvent the impact of sanctions, such that A1 remains sanctioned.

3) This itself covers several strands:

a) The alleged change in ownership of A1 Investment: in particular the alleged transfer of Mr Khan and Mr Kuzmichev's shares to Mr Kosogov on an unspecified date before 31 March 2022 on undisclosed terms;

b) Timing of the disposal, including questions about whether the disposal to Mr Fayn took place before the transfer of shares to Mr Kosogov;

c) The purchase price, which is said not to reflect A1's real financial position;

d) What are said to be concerted declarations as to the effect of these transactions.

4) Finally, it was said that the history of the application and the case more broadly disclosed a lack of candour.

- We will deal with these points in turn.

Joint arrangement (before March 2022)

- This is a key starting point to the argument. The question here is really one about aggregation. None of the Founders controlled A1 individually. The question is whether, at least before the middle of March 2022, they should each be treated as jointly owning or controlling it. There is then a question about whether, later in the day and after the sale/transfer there are still such indications such that we should conclude that Regulation 7(2) or 7(4) is engaged.

- The OFSI Guidance says this about aggregation:

"When making an assessment on ownership and control, OFSI would not simply aggregate different designated persons' holding in a company, unless, for example, the shares or rights are subject to a joint arrangement between the designated parties or one party controls the rights of another... Consequently, if each of the designated person's holdings falls below the 50% threshold in respect of share ownership and there is no evidence of a joint arrangement or the shares are held jointly, the company would not be directly or indirectly owned by a designated person".

- In terms of illustrating the kind of situation where a joint arrangement might be found, reliance was placed by Mr Bedzhamov on the approach in Shvidler v FCDA [2023] EWHC 2121 (Admin) which invoked the concept of "acting in concert". The meaning of a "joint arrangement" for ownership and control purposes was considered by Garnham J in that case, which concerned a judicial review of the Foreign Secretary's decision to designate Mr Shvidler on the basis that he was a business partner and close associate of Mr Roman Abramovich, and there were reasonable grounds to suspect that he had received significant financial benefits from him and he had been a nominee director of a company (Evraz) in relation to which Mr Abramovich could be treated as more than 50% of the shares or voting rights of the company. Garnham J accepted (at [103]) that:

"Given that Messrs Abramovich, Abramov and Frolov are treated by Evraz as "acting in concert", there are reasonable grounds to suspect that there exists a "joint arrangement" between them within the meaning of paragraph 3. Accordingly, each of them is to be treated as holding the combined shares of all three, and Mr Abramovich can be treated as owning, directly or indirectly, more than 50% of the shares and voting rights in Evraz."

- Given the equivalency of the terms in that judgment it is material to consider the definition of "acting in concert". The FCA Handbook notes that there is no definition of "acting in concert" in the Financial Services and Markets Act 2000 but suggests that persons will be acting in concert when each of them decides to exercise his rights linked to the shares in accordance with an explicit or implicit agreement between them. The UK Takeover Panel defines "acting in concert" as "persons who, pursuant to an agreement or understanding (whether formal or informal) co-operate to obtain or consolidate control... of a company or to frustrate the successful outcome of an offer for a company".

- Looking then at the facts of this case, prior to mid March, it is not in dispute that Messrs Fridman, Khan and Kuzmichev together held 95% of the shares in A1 Investment, which indirectly owned A1. The other 5% shareholding has not been revealed. That might not itself justify a conclusion that there was a joint arrangement in place. However, that evidence does not stand alone. On the contrary the back story of the company and the association of the individuals provides strong further reinforcement to the suggestion. In particular there is the fact that A1 was founded together by these same three persons, and that they have ever since worked together. That perception seems to have driven the co-ordinated approach to designating the Founders. In addition some reflection back from the more detailed evidence on shareholdings post March indicates that the shareholdings of the Founders were disposed so that Mr Fridman had 42.9% (i.e. the largest shareholding, but not a majority), while Messrs Khan and Kuzmichev between them controlled 52.01% (the total of Mr Khan's 29.1% and Mr Kuzmichev's 22.9%). Thus, together any two of them had a good functioning majority vote; and together their control was effectively complete. That situation where none could control individually and any two could control is amply resonant of a joint arrangement. In addition, later events resonate with this picture.

- We do therefore conclude that there is reasonable cause to suspect that there was a joint arrangement between the Founders up until the time of the disposal of the Founders' interests in or control over A1 LLC.

Arms' length disposal?

Circumstances of the disposal

- The disposal of A1 may be said to have two parts. One is the disposal of the shareholding in A1 Investment. The other is the sale of A1 LLC.

- VPB says that on or around 15 March 2022, before Mr Khan and Mr Kuzmichev were designated, they resigned from the Board of A1 Investment and effected a sale of their shares in A1 Investment to Mr Kosogov. This is said to be an arms' length transaction whereby Mr Khan and Mr Kuzmichev did not retain any interest in or control of A1 Investment. This point is significant because if (i) the share transfer was not before 15 March or (ii) the share transfer was before 15 March but that was not an arms' length disposal, A1 would have remained controlled by DPs after 15 March, and any purported disposal would be in breach of the sanctions regime.

- Ms Bloom for the Respondents states that: (a) as at 22 February 2022, the shares were 95% owned by the Founders; and (b) as at 31 March 2022, the shares were owned 42.9% by Mr Fridman and 52.1% by Mr Kosogov. The Respondents' evidence does not however reveal when the shares were transferred (in the period between 22 February and 31 March) and therefore: (a) who owned the shares when the Founders were designated on 15 March; or (b) who owned the shares when sale of A1 occurred on 22 March 2022.

- A precise account of when and how the resignations took place remains obscure. The evidence of Ms Bloom points to extracts dated 10 March and 18 March from the Luxembourg Registre de Commerce et des Société They disclose that Mr Kuzmichev and Mr Khan were on the board at 10 March. Ms Bloom says that:

"The 10 March 2022 extract does not identify Mr Fridman as having a role on the supervisory board of A1 Investment Holding SA and Mr Khan's name no longer appears on the 18 March 2022 extract. The only reasonable inference to be drawn from these documents is that the resignations had been tendered prior to these dates."

- As to shareholding there is evidence that at 31 March 2022, the major shareholders of A1 Investment were Mr Fridman (42.9%) and Mr Kosogov (52.1%). These holdings are through another Luxembourg company called CTF Holdings SA ("CTF"). This is at least apparently confirmed by a Luxembourg share register dated 28 March 2022, though it leaves a question as to the date of the disposal and whether it predated 15 March. Mr Randolph KC stated that no equivalent document showing the position on 15 March 2022 is available because there is an inherent administrative delay in updating the Luxembourg share registry. There is no evidence confirming this.

- That was the state of play on the evidence formally adduced. There was then reliance placed on some documents attached to a letter from Keystone Law sent on 2 March 2024 (i.e. 2 days before the start of the hearing). Those documents (said to be extracts from the Luxembourg share registry) appear on their face to show a sale of shares in CTF from Winstonhill Limited and Matson Holding Corporation (whose ultimate beneficial owners are Mr Khan and Mr Kuzmichev respectively) to Slavisilla Holdings Limited occurring on 15 March 2022. The effect of that transaction would be that the shareholders in CTF were Haberfield Limited and Slavisilla Holdings Limited, whose ultimate beneficial owners are, according to the letter, Mr Fridman and Mr Kosogov respectively. However, given the late production of these documents, the lack of proper verification or explanation thereof, and the lack of evidence that they were prepared contemporaneously, little if any weight can be placed on them.

- The conclusion we reach on the share transfer is that there is no clear or reliable evidence of the transfer of shares to Mr Kosogov having taken place before the designation of the Founders.

- As for the sale of A1, the case put is that Mr Fayn purchased all of the shares in A1 from Mr Fridman, Mr Khan, Mr Kuzmichev, and Mr Kosogov on 22 March 2022 ("the MBO").

- It has emerged during the course of evidence for the hearing that Mr Fayn was a 0.01% shareholder in A1 from around 2017-2020, was previously a 0.01% shareholder in Alfa-Eco LLC (A1's predecessor) and has also held a 0.01% shareholding in OOO Investment Company A1. It was submitted with, we consider, some force that these previous shareholdings suggest that Mr Fayn has previously acted as a nominee shareholder for entities in the Alfa Group.

- for example to portray Mr Fayn as a business operator who would wish to own and operate A1 himself?

- That is the picture which Mr Fayn seeks to paint. In his statement Mr Fayn explained the Alleged Buy Out as follows:

1) [6]: "Due to complicated geopolitical situation it became obvious that A1 LLC would no longer be able to operate normally and that there was a risk of default on its obligations to fund the litigation against Georgy Bedzhamov... and that this default would cause damage to my personal reputation. I therefore negotiated a purchase of all of the shares in A1 LLC. The transaction completed in March 2022 and was financed from my personal funds."

2) [7]: "The company was purchased at the market price, taking into account the current financial position of the company, political and economic risks."

3) [9]: "I hereby confirm that I own and control A1 LLC in full. There is no agreement with any third parties as to how I will operate or manage A1 LLC..."

4) [10]: "I confirm that I am absolutely independent of any third persons, including but not limited to, German Khan, Anzhelika Khan, Petr Aven, Mikhail Fridman and Alexey Kuzmichev and that none of them can affect my affairs or the affairs of A1 LLC so as to make them to be conducted in the interest of such other persons and in compliance with their wishes."

- There are however problems with this account. The starting point is that it is apparently common ground that the change was triggered by the designations (or the "complicated geopolitical situation"). The sale of A1 is acknowledged by Mr Fayn to be motivated at least in part by the "complicated geopolitical situation" and "political and economic risks". That appears (and was not denied) to be a reference to the possible detrimental effect on A1 of being connected to DPs, especially "on its obligations to fund the litigation against Georgy Bedzhamov".

- That situation could trigger a genuine sale; but it also offers a reason for a cosmetic disposal. Then there is the lack of rationale for the purchase by Mr Fayn, or account by him of his ability to actively run the business. Mr Fayn is about eighty years old. He has never apparently previously taken a major position in any of the companies. There therefore are certainly peculiarities about the sale to Mr Fayn, even before the financial situation is considered. There is nothing in Mr Fayn's apparent history, based on the materials to which we were directed, which would indicate that he was a likely purchaser and controller of A1. That and his apparent previous roles as a nominee shareholder give some cause to believe that the sale to him was not arms length.

- There are two other timing issues which are said to add some further doubt into the mix. The first is the timeline on the explanation of the sale. Ms Bloom's evidence is that she was first notified of the Alleged Buy Out on the day it took place, i.e. on 22 March. Mr Bedzhamov (via his solicitors) was informed of the Alleged Buy Out on 26 April 2022 in the following terms:

"The structure of A1 Investment Holding SA is however no longer relevant since we are instructed that the entire legal and beneficial ownership of A1 LLC is now owned by Mr Fayne, a non-sanctioned individual.".

- But it was not until 23 December 2022 that it was revealed to Mr Bedzhamov and the Court that Mr Fayn paid a mere £714 for the entire share capital of A1. This lack of openness does align more readily with a non arms' length disposal than with one which is entirely above board and commercial. However, we do not think that it can properly be said to add much reliable basis for suspicion.

- There is then the question of the timing of the sale itself. As Mr Fenwick KC pointed out, assuming the disposals were made on the dates asserted, there would not be a problem as to direct ownership after designation, and there is no breach of sanctions/circumvention because the sanctions are not yet in place. However he says that when one "pans out" from the individual transaction and looks at (i) the evidence which there is of a wider range of disposals covering this company and its associated companies (see above in the factual background section) (ii) press reports concerning near simultaneous disposals of shareholdings in Alfa Bank and another company (iii) all of the shares in the various holding companies being transferred to Mr Kosogov, it becomes arguably artificial to look at this disposal in isolation.

- As to this we are not minded to put any weight on this point. We appreciate the suspicions raised in the minds of Mr Bedzhamov and those acting for him by the press reports, but we have to bear in mind the distinction noted in the authorities between fact based suspicion which does (not might) follow from particular evidence and reflexive assumption based on unverifiable and untestable sources.

A1's Financial Position

- This is relevant to the question of the reality/commerciality of the sale. If the price paid was not a market price that would provide material which would (not might) tend to suggest that the control of A1 remains with the Founders.

- The sale is said to be an arms' length transaction at market price, though that price was the equivalent of £714. The low price is said to be due to A1's financial difficulties: according to A1's balance sheet as at 31 December 2021, it had a negative balance of around £4.3 million.

- We have been shown A1's balance sheet for 2021, which on its face indicates a net deficit. Mr Fenwick agrees that the balance sheet shows a deficit but contends that it does not reflect the true position. There are two notable issues taken with the balance sheet.

- The first is that it can be fairly clearly seen that some of what would, as a matter of English accountancy practice, undoubtedly be considered part of A1's assets do not appear on the balance sheet. In particular:

1) The debt owed to A1 arising from money advanced to VPB for the purposes of this litigation is absent. That is the US$20 million mentioned above;

2) The about £4 million which has been paid into court as security for costs and £1 million held by Keystone Law, VPB's solicitors, as fortification for the worldwide freezing order and search order of 27 March 2019;

3) No value has been given to the claims in these proceedings.

- Is there a good reason for this? There is no evidence of foreign accountancy practice which would justify a different approach (though Mr Randolph attempted to suggest that as regards the claim it had no value until it succeeded) and therefore we must deal with this on the basis of what this Court would regard as conventional practice.

- As far as the debts are concerned, unless A1 considers that VPB has no prospects of recovery in respect of these funds and the debt is written off, that is an odd omission. Similarly, it is conventional as a matter of English accountancy practice to assign a value to a claim which is considered to have any prospects of success, as a chose in action. If that is the case it would follow that, as Mr Bedzhamov contends, A1's true financial position is significantly healthier than that disclosed by its balance sheets. If this is right, it of course has an impact on the true market value of A1 and in turn colours the circumstances of the sale to Mr Fayn.

- The other issue relates to the nature of A1's debts. Under "Non-current liabilities", the balance sheet shows a sum in the row "Borrowed funds" equivalent to approximately £10.35 million. Conventionally a borrowing figure would correlate to a figure elsewhere covering interest on borrowings. Yet in the cash flow statement, the line "Interest on debt obligations" shows a nil figure. That raises questions. If borrowings are not leading to interest payments that would tend to suggest zero interest loans or other non-standard commercial arrangements. For the Respondents Ms Bloom, relaying information from Mr Tchernenko, points to the row under "Short-term liabilities" named "Borrowed funds" as the interest owed on borrowed funds, which was 90,351,000 roubles. Mr Fenwick's rejoinder was that if that is indeed the interest accruing on borrowed funds, it has not been paid to the lender as it does not appear in the relevant lines of the cash flow statement, which is again indicative of "non-standard finance".

- To meet this point, Mr Randolph took us to the next page of the balance sheet which contains a row named "Interest payable". But, as is perhaps apparent from this account, in evidential terms that was hardly helpful. It is unclear what the figure of 27,928,000 roubles in that row indicates. It was not referred to in Ms Bloom's witness statement and the figure does not match that said to be interest owed on borrowed funds. When asked whether the evidence was incomplete or incorrect, Mr Randolph replied that "Ms Bloom is entirely correct" that the 90,351,000 rouble figure reflects the interest owed, but the 27,928,000 rouble figure is the interest "actually paid or payable".

- As we noted in the hearing, however, that is not the point reflected in the evidence. VPB were on notice that Mr Bedzhamov was taking issue with this aspect of the balance sheet since at least 26 January 2024. Despite that, there is no evidence before us as to the meaning of the "Interest payable" figure. Furthermore, Mr Fenwick is right to say that even assuming "Interest payable" to mean what it says, that is distinct from interest actually paid, which may be indicated by the nil figure under "Interest on debt obligations". This interpretation of the numbers also roughly accords with the increase in interest accrued under "Short-term liabilities" by 27,929,000 roubles from 2020 to 2021, i.e. the liability to pay interest increased by the full amount, which suggests that no interest was in fact paid out. It does not aid VPB's case if the interest simply accrues on A1's balance sheet without A1 actually paying any money to its lenders. In these circumstances, we feel unable to place weight on Mr Randolph's explanation.

- There are other issues with the financial documents. For example, A1 Management Company LLC appears to have received £2.7 million by way of "dividends, interest on debt financial investments and similar income from equity participation in other organisations", e.g. from its subsidiaries, in 2021. The evidence before us suggests that the only subsidiary that was capable from making such a payment was A1, but it is not possible to discern how these payments were made from the A1 Balance Sheet. Ms Bloom says she is advised by Mr Tchernenko that this analysis is wrong, and this is supported by a report from "Finexpertiza", who she is instructed are A1's auditors. However, this report simply serves to confirm the discrepancy between the accounts of A1 (which was unable to pay dividends as a loss-making entity) and the accounts of its parent company A1 Group Management LLC (which reported receiving a dividend that could only have come from A1).

- The other document to which we should refer is a very short letter from Baker Tilly Legal Rus JSC dated 10 October 2022 which is said to verify the valuation of A1 for sale. In full, the letter (addressed to Mr Fayn) states: "In response to your inquiry dated 05 October 2022 (hereafter, Inquiry), we inform you that having performed our in-depth valuation analysis we can conclude, that the price paid for the sale of 100% stake in Al LLC indicated in the Inquiry is above its market value of 1.00 ruble." No information is provided as to how that valuation was arrived at or of what the "in depth valuation analysis" comprised - although on the face of it, it appears to have been conducted in somewhat under five days - part of which was the weekend. In those circumstances we are also unable to place any real weight on this document.

- It follows from the above that we do conclude that the evidence on the financial position of A1 is such as to provide some basis for concluding that the sale was not an arms' length commercial sale.

The Declarations

- It is suggested by Mr Bedzhamov that the grounds for suspicion thus far accumulated are further amplified by the position on the declarations which have been given. Specifically, Ms Bloom exhibits largely identical declarations by Mr Fridman, Mr Khan, Mr Kuzmichev, and Mr Kosogov made in June or July 2022 stating:

"I [name of seller] am writing to set out various matters relating to my previous beneficial ownership of shares in A1 LLC... and the consequences of their sale to Mr Alexandre Fayn on 22 March as follows:

1. I do not retain any shares in A1 LLC.

2. I do not have any legal beneficial interest in A1 LLC.

3. I do not exercise any control, directly or indirectly, over Mr Alexandre Fayn or A1 LLC.

4. I do not have any commercial dealings with A1 LLC.

5. I am not entitled to any money from A1 LLC or Mr Alexander Fayn by reference to my shareholding or subsequent disposal of those shares."

- Later, a second set of declarations by Mr Fridman, Mr Khan, and Mr Kosogov with different wording but to the same effect were exhibited. These were made between 28 February 2023 and 1 March 2023.

- Mr Bedzhamov contends that the declarations and their terms suggest an agreement and understanding between the Founders which reinforces the evidence that they would appear to dispose of their shares in A1 Holding to avoid that entity being majority owned by DPs.

- Again, we understand the reason why this point is being run. However, the declarations should in our judgment fairly be evaluated against not just the facts of the disposals but also against the facts of the dispute. In those circumstances - in particular where the question of sanctions had already been raised in the litigation a degree of co-ordination in responding to the case is understandable and means that the evidence cannot be said to be such as would as opposed to could give rise to suspicion.

Failure to respond to enquiries/Lack of candour

- Mr Bedzhamov also argues that there has been a general lack of candour and reluctance to provide information and that this including the refusal to provide basic information such as the date of the transfer and the sale price strongly supports the reasonable cause to suspect that this was not a bona fide share transfer.

- As already noted we do consider that the approach to information provision aligns better with a non bona fide transfer; but we do not consider that it should properly be regarded as supportive evidence. We therefore do not take this into account in reaching our conclusion.

Conclusion

- Taking together all the matters which we do consider amount properly to evidence we are (by some margin) persuaded that were the test "reasonable cause to suspect" it would be met on the facts of this case. This is not a situation where there is one query or area where suspicions arise. It is a case where there are multiple overlapping indications which suggest that the transfer and sale were not arms length transactions.

- The starting point of course is the finding which is made above as to the original joint arrangement. But that is not evidence of itself, merely background.

- Primary amongst the points which indicate that there is reasonable cause to suspect that that joint arrangement is still in place is the unsatisfactory nature of the evidence about the sale price. The figure given for the sale price is surprising on its face. The financial documentation adduced (in a lengthy and full exchange of evidence) fails to provide a coherent or robust justification for that figure. On the contrary there are what seem like obvious omissions, and the explanations given are inadequate and do not tie in with the rest of the document. The so called "verification" of the value is broad brush in the extreme and not at all what might be expected by way of professional valuation.

- Then there are the bases for reasonable cause lying within the structure and timing of the disposal. There is very slight evidence of the share disposal or its timing. That disposal is not to a neutral third party but to a long term employee of the Founders. The sale too is to a long term employee, with some evidence of his previously acting as a nominee shareholder.

- Accordingly, were it necessary to do so we would conclude that there is reasonable cause to suspect that, despite the share transfer in A1 Investment and sale of A1 to Mr Fayn there is reasonable cause to suspect that A1 is owned or controlled by a designated person or designated persons within the meaning of Regulations 5-6 of the Russia (Sanctions) (EU Exit) Regulations 2019.

Contingent Issue: Ownership and Control in fact

- This was not an issue originally in play. The relief sought as put in the application made by Mr Bedzhamov was as follows:

"A declaration as to whether, in light of the evidence before the Court, there is reasonable cause to suspect that A1 is owned or controlled by a designated person or designated persons within the meaning of Regulations 5-6 of the Russia (Sanctions) (EU Exit) Regulations 2019".

- This was echoed in the skeleton served which:

1) At paragraph 1 stated that Mr Bedzhamov "seeks a declaration as to whether there is reasonable cause to suspect that A1 LLC ("A1"), the declared funder of these proceedings, is owned or controlled by a designated person ("DP") or designated persons ("DPs")";

2) At paragraph 61 posed the issues as being that of construction, followed by "Whether there is reasonable cause to suspect on the facts .... What are the consequences if there is reasonable cause to suspect?"

- In oral submissions however the ground shifted significantly with Mr Fenwick inviting us, if we decided against him on construction (as we have done), to go further than the question of reasonable cause:

"Now that the evidence which both parties were entitled to put in, including an expectation of expert evidence which never came to pass, an expectation of evidence about those funded by −−those who are creditors of VPB, the court may now be in a position where it actually has to decide on the evidence before it whether, on the balance of probabilities, on that evidence, there is ownership or control."