- The First Claimant ("LCF") is in administration. The Second Claimants are the administrators of LCF.

- LCF raised money from retail investors by selling "mini-bonds". These were debt securities which were typically non-transferrable (so that there was no secondary market). Issuance of mini-bonds was not itself a regulated activity and the marketing materials for them did not require approval by any listing authority.

- Between 2013 and December 2018 LCF raised a total of over £237 million from about 11,600 bondholders. LCF presented itself to investors as a commercial lender to the SME sector in the United Kingdom. In fact it advanced the money it raised to a small number of connected companies, associated with four individuals, including its CEO. The Claimants contend that these advances were dressed up as commercial loans.

- One of the borrowers was the Third Claimant ("LOG"), a company incorporated in England and Wales which is now in administration. It borrowed about £122 million from LCF. The Fourth Claimants are the administrators of LOG.

- The Claimants were represented by Mr Robins KC, Mr Shaw and Mr Judd, instructed by Mishcon de Reya LLP.

- The First Defendant, Mr Thomson, was at all material times a director of LCF and, for most of its life, its CEO. The Claimants allege that Mr Thomson was also a beneficial owner of various direct and indirect recipients of money from LCF. Mr Thomson admits that he had a 5% beneficial interest in certain such recipients including LPE Support Limited ("LPE Support"), CV Resorts Limited ("CV Resorts"), CV Support Limited ("CV Support"), Waterside Villages plc ("Waterside Villages"), Waterside Support Limited ("Waterside Support"), Costa Property Limited ("Costa Property"), Costa Support Limited ("Costa Support"), Colina Support Limited ("Colina Support"), LOG, London Power Corporation ("LPC") and London Group LLP. Mr Thomson also admits that he was the beneficial owner of a company called London Financial. The nature of his admitted beneficial interest is disputed. Mr Thomson participated fully in the trial. He was represented by Ms. Dwarka-Gungabissoon, a solicitor advocate of Richard Slade & Partners LLP.

- The Second Defendant, Mr Hume-Kendall, was at all material times a director and a beneficial owner of various direct and indirect recipients of sums from LCF, including LOG and Leisure & Tourism Developments ("L&TD") and companies to which LOG and L&TD lent (or on the Claimants' case purported to lend) money. Mr Hume-Kendall was a director of LCF from 12 July 2012 to 15 August 2013, at a time when the company was dormant and was known (at various times) as Sales Aid Finance (England) Limited or South Eastern Counties Finance Limited ("SAFE"). Mr Hume-Kendall denies he had any involvement with LCF after 15 August 2013. The Claimants settled with Mr Hume-Kendall very early in the trial.

- The Third Defendant, Mr Barker, was at material times a director and a beneficial owner of various direct and indirect recipients of sums from LCF, including LOG. The Claimants settled with Mr Barker before the trial.

- The Fourth Defendant, Mr Golding, was at all material times a beneficial owner of various direct and indirect recipients of sums from LCF, including LOG. The Claimants also allege that Mr Golding was at all material times a shadow or de facto director of LCF, which Mr Golding denies. Mr Golding served a Defence, but was debarred from defending the proceedings owing to failures to comply with an unless order requiring him to provide disclosure of documents. He remains a live defendant against whom relief is sought. He did not attend the trial.

- The Fifth Defendant, Mr Careless, owned and/or controlled the Sixth Defendant ("Surge"), a marketing company engaged by LCF as its sales agent. These defendants ("the Surge Defendants") were represented by Mr Ledgister and Mr Curry, instructed by Kingsley Napley LLP.

- The Seventh Defendant, Mr Russell-Murphy, assisted SAFE in selling mini-bonds and, after Surge became the marketing agent for LCF, was engaged as a part of the sales team by Surge. He received payments from Surge, as did a company of which he was the sole director and shareholder, the Ninth Defendant ("GP"). The Claimants aver that Mr Russell-Murphy's knowledge is to be attributed to GP and to Surge. Mr Russell-Murphy admits that his knowledge is to be attributed to GP (as does GP) and does not plead to the allegation that it is to be attributed to Surge. Mr Careless and Surge aver that Mr Russell-Murphy was engaged on a consultancy basis and was not an employee of Surge; accordingly, Mr Careless and Surge deny that Mr Russell-Murphy's knowledge in its entirety can or should be attributed to Surge. Mr Russell-Murphy and GP served a Defence and gave disclosure of documents but did not attend the PTR or the trial. They remain live Defendants against whom relief is sought.

- The Eighth Defendant, Mr Sedgwick, was a solicitor. At various times he was a director and/or company secretary of various companies that were direct and indirect recipients of sums from LCF. He also drafted many of the documents for the transactions under which borrowing companies or their associated companies acquired assets from the individual Defendants (as explained below). He was also the owner and controller of LCF's security trustee, Global Security Trustees ("GST"), until 31 March 2018. He remains a live defendant. He represented himself at the trial.

- The Tenth Defendant, Mrs Hume-Kendall, is the wife of Mr Hume-Kendall and was the recipient of some sums that derived from LCF and/or LOG. The Claimants brought tracing claims against her, which she denied. The claims were settled early in the trial.

- There were also claims against the non-executive directors of LOG. These settled well before the trial.

The claims and defences in outline

- As already stated, LCF raised sums from members of the public through the issuance to them of mini-bonds. LCF issued 16,706 bonds to 11,625 members of the public, who collectively invested a total of over £237 million. LCF told the investors that it would generate returns on sums raised from bondholders by the onward lending of those sums.

- The Claimants allege that, in order to induce prospective bondholders to invest, LCF made various representations to them, through information memoranda, brochures, telephone calls and/or conversations, including as to LCF's overheads, the use to which LCF would apply funds invested by bondholders, the status of companies to which LCF would lend sums and the security of the investments made by bondholders. Mr Golding accepts in his Defence that he occasionally and informally discussed design matters in relation to LCF's marketing materials, but says he was not otherwise involved with and had no responsibility for the content of those materials. Mr Thomson, Mr Russell-Murphy, and GP admit that representations were made to prospective bondholders by the methods alleged but dispute the content of the representations made. Mr Careless and Surge contend that the Claimants' case on the alleged representations is inadequately pleaded. Mr Careless and Surge make no admissions as to whether the alleged representations were made or the precise meaning to be attributed to the words of the representations pleaded by the Claimants, but contend that a number of the alleged representations are contrary to the express wording of the information memoranda and/or brochures.

- The Claimants allege that the First to Tenth Defendants received substantial sums directly or indirectly from LCF, totalling £136,189,713.76, and that these sums were misappropriated from LCF and/or LOG by the First to Tenth Defendants. The various Defendants admit that they received certain sums but deny that these sums were misappropriated; rather, each contends that this was money to which they were lawfully entitled.

- As just stated, LCF lent the sums it received from bondholders to various companies. The Claimants allege that all these companies were connected to and/or controlled by the First to Fourth Defendants and, further, that the loans (and associated sale agreements) were a device to conceal the misappropriation of money from LCF by the First to Tenth Defendants.

- As noted above, one of the borrowers was LOG. This company also lent sums it borrowed from LCF to various entities. These entities were consequently the indirect recipients of funds from LCF. The Claimants allege that all of these companies, apart from Atlantic Petroleum p/f ("Atlantic Petroleum") and Independent Oil and Gas ("IOG"), were connected to and/or controlled by the First to Fourth Defendants and, further, that the making of the loans was (at least in part) a device to conceal the misappropriation of money from LCF and/or LOG by the First to Tenth Defendants. The Claimants contend that, of the approximately £122 million borrowed by LOG from LCF, only £38.4 million was applied by LOG to genuine commercial transactions.

- The Claimants allege that in many instances borrower companies were incorporated only very shortly before entering into loans; the borrower companies often conducted no discernible business activity beyond borrowing money; borrowing companies failed to file statutory accounts; borrowing companies manipulated their accounting year-ends; the names of borrowing companies were changed for no discernible reason; loan debt was allocated arbitrarily to borrower companies apparently without reference to any genuine commercial need; very substantial loans were advanced to borrower companies without any written loan agreement in place; loan agreements were dishonestly back-dated; sums purportedly borrowed by one company were paid to some other recipient for no discernible reason; sums purportedly lent to borrower companies were paid directly or indirectly to certain of the Defendants; security agreements were incomplete or otherwise defective and substantial borrowing was unsecured or insufficiently secured; and LCF's security trustee was owned and controlled by Mr Sedgwick and, subsequently, Mr Thomson.

- The Claimants also allege that the alleged misappropriations were effected in some cases through the creation of dishonest transactions which had no commercial rationale but were implemented to disguise the misappropriation of bondholder money. These include transactions described as the Lakeview SPAs, the Elysian SPA, the Prime SPA, the LPT SPA and the LPE SPA.

- The Claimants also allege that LCF was operated as a Ponzi scheme and that payments of interest and principal to existing bondholders were funded by the proceeds of new bonds, rather than from income or other resources generated by the borrowing companies themselves. They allege that the borrowing companies never paid any amounts from their own resources to LCF and that any interest payable on their loans was covered by LCF allowing increases in the principal amounts they owed. The Claimants say that all repayments to existing bondholders were funded by sums raised from new investors.

- Mr Thomson admits that he had a 5% beneficial interest in a number of LCF's borrowers but denies any impropriety and maintains that all loans were backed by sufficient security. He contends that the business of LCF was legitimate throughout.

- Mr Hume-Kendall admitted (before settling) that he was interested in various of the borrowers of LCF and/or LOG but denied any impropriety and, in particular, contended that all lending by LOG was made in good faith for the purposes of LOG's business. He denied any wrongdoing.

- Mr Barker admitted (before he settled) that he, Mr Hume-Kendall, Mr Thomson, and Mr Golding were interested in various of the borrowers of LCF and/or LOG but denied any impropriety and contended that all lending by LOG was made in good faith for the purposes of LOG's business. He admitted receiving sums arising from share sales but said that they were proper sales and arose from the restructuring of the group of which LOG was part and the acquisition of certain technology companies by that group.

- Mr Golding admits in his Defence that he had a beneficial interest in companies which borrowed sums from LCF and/or LOG but denies any impropriety. Mr Golding says in his Defence that he was not a director of any of those borrowing companies and that (save in relation to FS Equestrian Services Limited ("FSES")) he was not involved in the decisions taken by those companies to borrow from LCF and/or LOG. Mr Golding also admits that he received sums pursuant to the share sales; he says these were bona fide and genuine commercial transactions pursuant to which he was entitled to the sums received in consideration for the sale of his various interests.

- Mr Sedgwick admits in his Defence that loans were made by LCF and LOG to connected entities but alleges that he was not aware that LCF only made loans to connected entities and denies any impropriety. He admits that certain companies had recently been incorporated but avers that was part of a restructuring exercise. He admits that he controlled LCF's security trustee but says that he relied on LCF's solicitors, Lewis Silkin, that the appointment of the security trustee was valid and appropriate. He admits his involvement in the share sales by Mr Barker and Mr Hume-Kendall but says that they were proper and arose from the restructuring of the group of which LOG was part and the acquisition of certain technology companies by that group.

- Mr Careless and Surge do not admit that there was any fraud or wrongdoing in the business of LCF. They deny that they participated in any wrongdoing there may have been. They say that their role was limited to providing LCF with third-party, outsourced investor facing services and they did not participate in the lending, treasury, or financial aspects of LCF's business; and always believed LCF's business to be genuine and legitimate.

- Mr Russell-Murphy and GP make no admissions as to the Claimants' allegations. Mr Russell-Murphy says that he was acting as a salesman and was entitled to receive the sums he did.

- As to the legal character of the claims, the Claimants allege that the representations made by LCF to bondholders were false and that the business of LCF was carried on with the intent to defraud bondholders and/or for the fraudulent purpose of misappropriating bondholder monies and/or was operated as a Ponzi scheme. The Claimants allege that each of the remaining live Defendants was knowingly party to that fraudulent trading and should therefore make contributions to the Claimants' assets. The relevant Defendants deny these claims.

- The Claimants also allege that that Mr Thomson and Mr Golding breached the duties they owed to LCF by reason of the matters set out above and that such breaches caused LCF loss and damage. Mr Thomson and Mr Golding deny these claims. As already noted, Mr Golding denies that he acted as a director of LCF and therefore denies that he owed any duties to LCF.

- The Claimants allege that the other live Defendants dishonestly assisted Mr Thomson and Mr Golding in breaching their fiduciary duties to LCF and are therefore liable to compensate LCF for the relevant losses. All the live Defendants deny these claims.

- The Claimants also make proprietary claims. The Claimants allege that Mr Thomson and Mr Golding caused LCF to pay away money in breach of their duties to LCF, to the First to Eighth and Tenth Defendants, and that these Defendants received such sums with knowledge of these breaches such that it would be unconscionable for them to gain or retain any beneficial interest in the assets received. The Claimants contend that such assets received by the First to Eighth and Tenth Defendants, or the traceable proceeds thereof, are held on constructive trust for LCF and/or subject to LCF's equitable interest therein. The relevant Defendants deny these claims. They say that there was no misappropriation. They also argue that the claims fail in law because the money which reached the Defendants were no longer the property of LCF, having been lent to borrowing companies or paid to Surge as fees.

Witnesses of fact

- The key events took place up to a decade ago. The factual history is complex and involved. The witnesses naturally struggled to remember the details and sequence of events. Memories are mutable and are influenced by the forensic process and by interests and motives. I shall assess the oral testimony as part of the entire evidence. In this case, there are extensive contemporaneous documents including emails, texts and other electronic messages. There are some gaps, as explained below, but it is generally an informative record.

- I have reached findings of fact on the basis of the witness testimony, the contemporaneous documents, the motives of the parties and others, the uncontested and uncontroversial facts, and the inherent probabilities.

- I will make specific observations about the witnesses' credibility when reaching findings of fact. Some comments are made here about my impressions of the witnesses.

- The Claimants' witnesses were Mr O'Connell, Mr Shinners, Ms Lloyd, Mr Hudson and Mr Pitt.

- Mr O'Connell is one of the administrators of LCF and LOG. He gave evidence about the states of affairs in the administrations. His evidence was clear and concise and was not seriously challenged. I accept it.

- Mr Shinners is one of the administrators. He gave evidence about the way the administrators dealt with the IOG assets owned by LOG. He explained that LOG was not itself a trading company and only held assets. He answered questions fairly and clearly and I concluded that his evidence was reliable.

- Ms Lloyd is an employee of the administrators' firm. She gave evidence concerning the decisions taken by them about the disposal of some of the assets in the administration of LCF. She was a cautious witness who was careful to limit her answers strictly to the question. At times she seemed nervous and somewhat defensive, but I saw no reason to doubt her evidence, which I accept as reliable.

- Mr Pitt is a chartered accountant who advised the administrators in relation to the sale of the Waterside site. He explained that the title was only sorted out in the summer of 2021. He was a straightforward and helpful witness. His evidence was not undermined by cross-examination, and I accept it.

- Mr Hudson is a forensic accountant. He has produced three witness statements dealing with the claimants' case that LCF operated a Ponzi scheme. He has undertaken a detailed analysis of bank statements, internal company ledgers and other books and has explained money flows between investors, LCF, the borrowing companies and various other entities. He summarised his conclusions in the form of witness statements. The Defendants did not object to the admissibility of his evidence but submitted that he was not an expert witness and that he had not sought to comply with the CPR provisions for such a witness. That is correct, but he was not put forward as an expert. He occasionally became argumentative under cross-examination, but I concluded that his evidence about the money-flows based on the bank and accounting records was presented in a helpful and convenient form, and the Defendants did not seriously challenge his summaries of what that evidence showed.

- I also heard evidence from Mr Thomson, Mr Careless and Ms Venn.

- Mr Thomson gave some evidence about his physical condition and mental health. In December 2023, he underwent surgery on his spine. This has left him in considerable pain for which he was still taking painkillers, including opioids, during the trial. I held a ground-rules hearing at which I directed that there would be appropriate breaks to allow Mr Thomson to leave the witness box and walk about to relieve his pain. I explained to Mr Thomson that he should indicate if he needed a break. I also ruled that the usual bar would not apply to discussions between Mr Thomson and his lawyers insofar as they concerned his health and pain tolerance while he was giving his evidence. In giving his evidence, Mr Thomson did ask for breaks from time to time. On some occasions it was necessary to stop the cross-examination earlier than usual to give him longer breaks. Counsel for the Claimants also agreed that he would seek to ensure that his questions were readily comprehensible. I was satisfied that he did so.

- As to Mr Thomson's mental health, I was provided with the evidence of a psychiatric consultant who explained that Mr Thomson was subject to anxiety and stress and presented signs of adjustment disorder, which could affect his concentration and focus. Mr Thomson's advocate asked that the details of his condition should not be publicly disclosed and there is no reason in this judgment to do so. The consultant psychiatrist concluded that Mr Thomson was able to understand the questions he asked during their consultation. I have taken this report into account when assessing Mr Thomson's evidence. I was satisfied throughout his evidence that Mr Thomson was able to understand the questions posed in cross-examination. He engaged with the details of the questions and sometimes asked for clarification. He also appeared to me to be aware not just of the meaning of the questions but of where he thought they might be leading.

- Mr Thomson was an extremely poor witness. My reasons for reaching this conclusion included the following:

i. The documentary record establishes that Mr Thomson was repeatedly involved in the creation and back-dating of documents for the purposes of misleading third parties, including auditors. I shall refer to numerous examples of this below. Mr Thomson accepted that some of the contemporaneous documents he was taken to contained lies or omissions. He sought to justify these as harmless lies or as a way of stalling or buying time. I reject this attempt to downplay his lies. They included deliberately lying to auditors about a non-existent key contract of LCF, lies in a mortgage application form and lies to his solicitors about how LCF had come to be listed on a website. They were serious lies and his attempts to justify them throw significant light on Mr Thomson's approach to truth-telling generally.

ii. I am satisfied that Mr Thomson gave evidence in court which was not only untrue but which he knew to be untrue. Indeed, he was serially untruthful, and it was hard to credit very much of what he said. Some examples are the alleged existence of two written agreements dated 15 July 2015 on their face, which I have concluded were only created much later, after the collapse of LCF; Mr Thomson's explanation for a series of payments made to him personally by Surge; Mr Thomson's evidence about the circumstances in which he signed tax returns for 2015/16 and 2016/17; his contention that he had handed control over One Monday Limited ("One Monday") to Mr Barker; and his contention that a signed copy of a service agreement between LCF and Surge was sent to him by Surge in October 2016.

iii. Mr Thomson was often evasive in answering questions, even in the face of documents which undermined the evidence he was giving.

iv. When he thought it suited his case, he claimed to remember conversations and oral agreements which were not referred to in his witness statement or reflected in the documentary record. But at other stages in his evidence, when it also suited him, he fell back on saying that he had no recollection at all, even when this was improbable.

v. As his evidence progressed, he was increasingly inclined to blame other people, saying they were responsible for tasks or communications and that he had little involvement, when the documents showed that he was indeed centrally involved.

vi. There were occasions when he disagreed with a factual proposition which had been taken verbatim from his own witness statement.

vii. His answers sometimes shifted and became inconsistent, within a short period of cross-examination.

viii. There was language in his witness statement which meant nothing to him and which had to be explained to him.

- For these reasons, I have treated Mr Thomson's evidence cautiously except where supported by documents or uncontested facts.

- Mr Careless began his evidence by giving short and clear answers. As the cross-examination went on this changed and he started to give long, digressive, self-exculpatory ones, often repeating refrains. I concluded that I must take a cautious approach to his evidence save where corroborated by documents or uncontested facts:

i. I found some of his evidence to be incredible as it was given. An example was his evidence about Surge's payments to Mr Golding of 1% of the gross receipts raised from new bondholders (amounting to 4% of Surge's fees). I could not accept his explanation that this was an introduction fee, since it was agreed long after Surge started working for LCF and there was no commercial reason Surge would have agreed to pay it other than to keep Mr Golding on-side and maintain its 25% commission.

ii. Another example was the payment by Surge of 0.5% of gross receipts (2% of Surge's fee) to Mr Thomson. I was unable to accept his evidence that this was for work conducted by Mr Thomson for Blackmore, another client of Surge.

iii. Many of Mr Careless's answers in cross-examination were long and formulaic, referring to LCF's lawyers and auditors, even when they had little to do with the question. I reached the firm impression that he was adhering to a preordained script rather than trying to answer the specific questions.

iv. His evidence about the sequence of events was often confused: he frequently referred to much later events (including the audits of LCF's accounts and meetings with Goldman Sachs) to explain his conduct on earlier occasions. Mr Careless was willing to accept on many occasions that he could not remember the sequence of events. This was realistic, but it undermined his insistence that he had a firm and clear memory of something that happened to be helpful to his case.

v. He accepted that he had rehearsed the relevant events in his mind a great many times over the intervening years and had been interviewed on several occasions, for which he had carefully prepared. It is entirely natural that there was much blurring and even confusion in his memory of the sequence of events. There is obviously much at stake in this case, and he has an interest in presenting his own conduct in the best possible light. But I have no doubt that it has affected his recollection of events which took place up to nine years ago.

vi. Mr Careless gave evidence to the administrators at a private examination under section 236 of the Insolvency Act 1986 in 2020 which is inconsistent with the evidence now given. At the date of the examination the administrators did not have all the documents now available to them. I have concluded that these changes in his evidence only came about because Mr Careless has now been confronted with further documents.

vii. The documents show that Mr Careless prepared for the private examination with a series of model answers, which he was tested on. These included that the 25% fee was a market fee and that he took comfort from the audited accounts. These are themes that Mr Careless repeated many times in his oral evidence at this trial.

viii. Some of the contemporaneous evidence shows that he was willing on occasion to tell deliberate lies about the relevant events. An example is an email of 1 April 2019 in which he described the steps he had taken in a proposed property transaction in the Isle of Wight. I found his evidence was not honest.

- Ms Venn worked with Mr Careless. (For some of the relevant period, before her marriage, she was called Kerry Graham, but for convenience she has been referred to throughout the trial as Kerry Venn.) She was a confident witness who generally gave her answers clearly. However, I concluded that I should treat her evidence cautiously save where corroborated by a document or the uncontested facts:

i. Ms Venn made it clear that she thought Mr Careless was wrongly accused of wrongdoing. There is nothing wrong with that, but I have no doubt that it coloured her recollection. She had read the transcripts of Mr Careless's cross-examination. Again, there is nothing inherently wrong with that but there were parts of her evidence which closely echoed Mr Careless's oral testimony.

ii. Ms Venn was integrally involved in the relevant events, which have led to huge publicity, and she has an interest in being seen in the best light.

iii. As her evidence went on, she gave longer, more argumentative answers. On a number of occasions, she stated confidently that she had or had not done or thought something only to be shown a document which undermined her answer and belied her confidence.

iv. It is also clear that soon after the closure of LCF's business she and Mr Careless were concerned to defend Surge's actions and that she and others collected materials to seek to justify what had happened. Hence Ms Venn has been preparing the defence of the allegations against the Surge Defendants for at least five years.

v. I concluded that Ms Venn was concerned seriously to downplay some of the concerns she had at the time about Mr Thomson's honesty by putting her contemporaneous descriptions of him down to a personality clash and his misogyny. While there was an element of truth to that, I have no doubt that Ms Venn in fact often mistrusted Mr Thomson. The documents show that she did not trust him. Nor did others at Surge.

vi. Moreover, Ms Venn's oral evidence on a central point involved a significant shift from her witness statement. She said there that when there were concerns, she and Mr Careless normally asked Mr Russell-Murphy to speak to Mr Thomson and provide an answer and that Surge were always satisfied with the response. In her oral evidence, however, she said that what she meant was "loosely satisfied". She later said that she had obtained a satisfactory answer on a "low scale of satisfaction", which meant that she still had doubts about the relevant point but could not argue with what she had learnt. She also described a range of being satisfied from strong to weak and said that on some points she was only "weakly satisfied".

vii. None of this nuance appeared in her witness statement, which implied that Surge was completely satisfied by what Mr Thomson said. This was a significant shift. I came to the conclusion that when Ms Venn said in her statement she was satisfied she was generally saying that she was not in fact satisfied of the truth of what Mr Thomson had said, but that she did not have the material to prove that what he was saying was untrue. That is far removed from the impression given in her witness statement. As explained in detail below there are many documents showing that she did not trust Mr Thomson or LCF at all.

viii. Overall, I concluded that the contemporaneous documents provided a much better guide to the history than her statement and, indeed, her oral evidence, which was often a charitable reconstruction.

ix. I therefore treat her evidence with caution, although there were parts of Ms Venn's evidence which I accept. I also record that I did not think she was deliberately trying at any stage to mislead the court.

- The court may draw adverse inferences from the decision of a party not to give evidence: see Efobi v Royal Mail Group [2021] 1 WLR 3863 at [41].

- Mr Thomson explained in his witness statement that he was calling evidence from the audit partners at PwC and EY using witness summonses. He also said at pre-trial hearings that he would call not just the PwC and EY partners but also partners from Oliver Clive and Lewis Silkin. In the event no such witness summonses were served. There was no formal explanation for this, but counsel for Mr Thomson said that PwC and EY engaged City solicitors to contest any such summonses. Given that Mr Thomson has serious constraints on his access to resources (owing to proprietary freezing orders), I do not think I should draw adverse inferences from his failure to require the attendance of these witnesses.

- Though he appeared at the trial, Mr Sedgwick chose not to give evidence despite having served a witness statement. I explained to him that the Claimants might invite the court to draw adverse inferences from that decision. There were many points where Mr Sedgwick could have given evidence. These included his understanding of the representations that were made to bondholders and the underlying business of the borrowing companies, the purposes of the various SPAs and whether they were (as alleged by the Claimants) uncommercial transactions used to mask misappropriations, the role of Global Advance Distributions Limited ("GAD"), the role of the security trustee, and the backdating of documents. Mr Sedgwick did not explain his reasons for not giving evidence, other than by submitting that the Claimants had not proved their case. I have concluded that I should draw adverse inferences from his decision not to give evidence. I set out below the respects in which I consider adverse inferences should be drawn below.

- Mr Russell-Murphy has not been formally debarred from defending. He has not put in a witness statement or participated in the trial. The Claimants did not, however, invite me to draw adverse inferences against him from his failure to participate. Similarly, in circumstances where Mr Golding was debarred from defending the claim for failing to disclose documents, the Claimants did not invite the court to draw any adverse inferences against Mr Golding.

The expert evidence

- There was expert evidence on three issues: the market rate for the services provided to LCF by Surge; the value of LOG's interest in IOG; and the value of land in the Dominican Republic.

- On the first issues, the experts gave evidence on whether there was a market rate for the services provided by Surge and whether hypothetical parties transacting at a market rate would have agreed such a rate. The experts agreed that there was no generally accepted market rate for the set of services provided by Surge. On the second point, they differed.

- The Claimants called Dr Okongwu, who produced two reports. He is a well-qualified and experienced economics consultant. I considered that he gave careful and considered evidence. He listened meticulously to the questions and answered fairly. His reports were fully reasoned and contained numerous citations.

- The Surge Defendants called Mr Grainger. His experience has been as a regulatory and compliance consultant. He has broad and long-term experience in those fields. The Claimants made a number of criticisms of his evidence, including that: (a) he lacked relevant expertise and appeared to confuse personal experience of certain transactions, such as the cost of outsourced services, with expertise in those transactions; (b) he did not cite any relevant material concerning Surge's fees other than contemporaneous documents provided by Surge's solicitors; (c) his conclusions were based on assertion rather than reasoning; (d) some of his conclusions were circular; (e) he failed in the joint memorandum to address the differences between the experts on some issues, basing this on grounds of "irrelevance", even though he had originally raised those issues himself; and (f) he was partisan and unwilling to consider positions contrary to the case of Surge.

- I shall return below to the substance of this evidence to the extent that it matters. But at this stage I should record that I concluded there to be real force in each of the Claimants' criticisms. Mr Grainger failed to engage properly with examples which might lead to conclusions damaging to the Surge Defendants' case. He struck me as partisan. I concluded that where the experts differed, the evidence of Dr Okongwu was to be preferred to Mr Grainger's.

- But the key point to take from this evidence was that the experts were able to agree that there was no market rate for services of the kind provided by Surge.

- The second discipline was the value of LOG's interest in IOG. The Claimants' expert was Mr Osborne, a forensic accountant and valuer. He produced two reports. Mr Osborne's evidence was clear and was not seriously challenged in cross-examination. It was not suggested that he lacked expertise and I accept his evidence. Mr and Mrs Hume-Kendall instructed Mr Wright to give evidence on this issue. Mr Wright produced two reports. Following the settlement agreed between them and the Claimants, Mr Wright did not give evidence and no reliance was placed on his reports by the remaining Defendants.

- The third discipline was the value of the land in the Dominican Republic. The Claimants' expert was Mr Watson, an expert valuer with relevant experience with land there. He was the only expert who gave evidence in this field. He produced two reports, one dealing with the value of The Hill and the other addressing the value of The Beach. There was no serious challenge to his evidence in cross-examination and I accept it.

Findings of fact

- In reaching findings of fact, I shall not address every submission or item of evidence referred to by the parties but make findings on the points I consider material. I have, however, carefully considered all the evidence and submissions in reaching these conclusions. I apply the civil standard of balance of probabilities (while noting the seriousness of the allegations).

- Mr Thomson submitted that some of the facts covered during the trial were not properly in issue on the pleadings. His counsel did not object to these areas of the case being covered in cross-examination or to the documents being referred to during the trial. It is convenient to make relevant findings and then address the pleading points.

- I have drawn on the written closing submissions of the parties in compiling this section. The Claimants set out a detailed chronological summary of the documents. I invited counsel for the Defendants in their closing submissions to indicate any points of disagreement with that summary. Counsel for the Defendants did not object to this course. Much of the Claimants' chronological summary was not contested by the Defendants and I have drawn on it below, amending and supplementing it as appropriate. This does not of course apply to the inferences or findings of facts on the disputed issues which the parties have invited me to make. I specifically asked the parties to identify in their closing submissions the findings of fact they sought and the basis for these findings. They helpfully did this and I have taken account of their submissions.

- The arrangement of this section of the judgment is partly chronological and partly thematic.

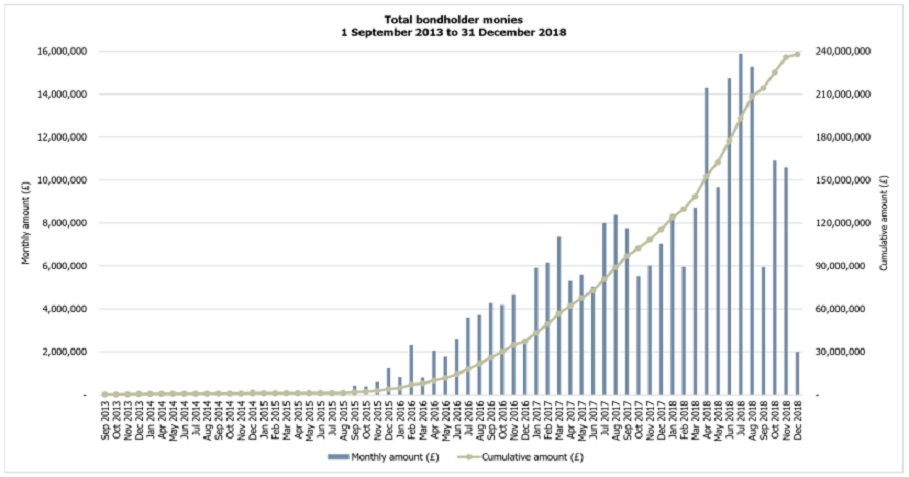

LCF's fundraising from bondholders

- The following graph shows the amounts raised by LCF from bondholders over the full period from its incorporation (as SAFE) until the FCA raid on 10 December 2018. There are certain landmark dates. Surge started selling bonds in August 2015. LCF started issuing ISA bonds in December 2017.

The Hill

- The early history conveniently starts with an investment scheme for the purchase of off-plan plots of land in the Dominican Republic of an area known as "The Hill" by investors who had paid deposits. The Hill was an undeveloped plot of c.136 hectares, about twenty miles from the north coast of the Dominican Republic, near a small village called Cupey.

- The plot was acquired by a Dominican Republic company, Inversiones 51588 SRL ("Inversiones"), in March 2012 for a sum of £708,752. Inversiones was a subsidiary of Sanctuary PCC, a Guernsey company which was itself a subsidiary of Sanctuary International Resorts Ltd ("Sanctuary"), a company connected with Mr Golding and Mr Hume-Kendall. I shall return to the dealings with The Hill.

- It is, though, convenient here to summarise the evidence about its value. There have been several valuations of The Hill. There was a draft valuation dated 24 December 2013 prepared by Jonathan Marshall which valued it at US$7.3 million. The report expressly stated that it was prepared for internal purposes and should not be relied upon for loan security. Mr Marshall was instructed to review a valuation conducted by a Julio Perdomo. Mr Marshall visited the Dominican Republic and met Mr Perdomo. The draft said that it was for the "fair value" of the land (i.e. the estimated price for a transfer between identified knowledgeable and willing parties that reflects the interests of the parties). He considered that the value reached by Mr Perdomo was excessive and applied a discount to it. His report was not a Red Book valuation and said that limited reliance should be placed on it.

- A revised draft valuation of The Hill by Jonathan Marshall was circulated on 20 March 2014. Again, it was for fair value. In this valuation, Mr Marshall estimated the value of the same site to be US$19.6 million. The draft report does not contain the earlier reservations about the estimate prices per square metre suggested by Mr Perdomo. He also included a residual valuation based on a proposed development plan. The draft explained that Mr Marshall had not undertaken a detailed development appraisal with cash flow forecasts and had ignored interest costs. The draft said that it was not a Red Book valuation, and that limited reliance should be placed on it.

- There were also three valuations of The Hill produced by the same Mr Perdomo who was referred to in Mr Marshall's draft reports. The first, dated 17 May 2017, assessed the value of The Hill at US$37,794,482.88. The bulk of this figure was accounted for by land which Mr Perdomo assigned a value to of US$100 per m2; this was substantially above the figure of US$16.60 per m2 he had discussed with Mr Marshall. The second, dated 10 May 2018, estimated the value of The Hill to be US$39,594,940.90. The third, dated 13 November 2018, assessed the value of The Hill at US$44,601,340.90. By this time, the land containing the bulk of the value was given a value of US$125 per m2.

- Mr Perdomo's methodology appears to have been to estimate the price per m2 of land from comparables and then multiply this by the relevant area, without applying any discount. The values he reached are much higher than those produced in Mr Marshall's reports and do not appear to have taken account of the extent of the development authorised on each comparable. The three reports do not state that they comply with Red Book requirements.

- There have been further valuations since the collapse of LCF. Cushman & Wakefield conducted a valuation of The Hill as at 1 June 2020 which gave it a market value (following 12-24 months of marketing) of US$2 million and a liquidation value (following 3-6 months of marketing) of US$1 million.

- Rofiasi Ingeneria conducted a valuation of The Hill as at 12 November 2020, which valued it at US$928,227.

- Mr Watson, the Claimants' expert in this case, has assessed the market value of The Hill (using the comparables method) as at 3 October 2023 to be US$5.43 million. He puts its value between April and November 2017 at US$4.55 million.

- I find that the value of The Hill at the material times was that given by Mr Watson. I also find that it would have been obviously reckless for any commercial lender to have relied on the draft reports of Mr Marshall or Mr Perdomo. Mr Marshall's reports were expressed to be in draft. They were not Red Book valuations. They referred to fair value rather than market value. The second report stated that he had conducted no detailed cash flow analysis for the development. The second report referred to comparable figures without discounting them for the reasons contained in the first report (which appeared sound). Mr Perdomo's reports used comparable figures without discounting them, as they should have done as explained in the first report of Mr Marshall. Moreover, the land had been bought as a bare plot in March 2012 for c. £700,000 and it remained in that state. There was no evidence that there was any change in the planning permission for it.

The Beach

- There was a second undeveloped site in the Dominican Republic known as "The Beach" (or "Magante"), consisting of 38 parcels of land.

- On 22 August 2012 Tenedora 98520 SRL ("Tenedora"), a subsidiary of Sanctuary, entered into a contact with numerous vendors to acquire the land in 38 parcels, for a total of c. US$3.5 million. This contract was unperformed for some years. In 2013, Mr Hume-Kendall and Mr Golding decided not to proceed with the acquisition and development of The Beach. It was not until late 2017 that Tenedora began to pay for and acquire some parcels (which were later registered in its name in 2018 and 2019).

- There have been various valuations of The Beach. I accept the Claimants' submission that it is extremely hard to compare the valuations because they cover different areas of land.

- Under the 22 August 2012 sale contract, the 38 parcels of land totalled 241,707.44m2 (i.e. c. 24 hectares).

- Mr Marshall prepared a draft desktop appraisal in about May 2014 which said the site extends to 23.5 hectares. This was said to be for fair value. It was not a Red Book valuation. Mr Marshall reviewed a report dated 21 May 2013 by Mr Perdomo. He referred to a proposed development plan for 320 units for a luxury spa and resort. As to Mr Perdomo's comparables, Mr Marshall observed that these had taken little account of the extent of the development on each comparable or factors like location, situation, lot size, planning permission, road access and development timescale. Mr Marshall's draft report said that he considered Mr Perdomo's site value to be excessive and that it would not be prudent to use it. Using the residual method Mr Marshall derived a value of US$37.95 million. He said that the appraisal was very limited in scope and had been undertaken without the benefit of a full investigation as to costings and comparables and that the addressee (International Resorts Group plc ("IRG")) should therefore place limited reliance on the figures.

- There was an appraisal produced in November 2016 by one Rafael Oviedo concerned with an area of some 25.8 hectares, comprising thirty-two certificates of title from different owners. Mr Oviedo was described as an "architectural planner". He appears to have given various views about market value, one of US$11.61 million (as the land currently was), US$16.777 million (with non-objections to its development) and US$25.8 million (with a full development project approved). The appraisal was not a Red Book valuation, and its purpose is unclear. Nor did it contain any reasoning to support the conclusions.

- In May 2018 Mr Perdomo produced a report in which he valued land labelled as Magante I, comprising a total of c. 29.8 hectares. He said the market value was c. US$42.5 million. He used a comparative approach. The report was not a Red Book valuation. There appears to have been no adjustment of the comparables listed by Mr Perdomo for location, size, planning or road access.

- Mr Perdomo produced another report in November 2018 for land called Magante I and Magante II, giving the area of the former as 29.8 hectares (hence larger than his earlier report). He gave the same value of c. US$42.5 million for Magante I.

- After the collapse of LCF, a firm called Rofiasi was instructed to value a site of 29.5 hectares, comprising parts of Magante I and Magante II. Rofiasi plotted Magante I as consisting of only some 15.2 hectares.

- Mr Watson has valued the same area of 15.2 hectares on 2 October 2023. He valued it at £4.9 million.

- I find for these reasons that the historical valuations are of extremely limited value.

- I find that, in any event, Tenedora only ever owned certain of the parcels of land and never owned the entire site. It only began to acquire the parcels in 2017. I also find that it is difficult to place a value of the parcels owned by Tenedora because, without owning substantially all the parcels, it would not have been possible to develop the resort.

- I find that the value of The Beach at the material times was no higher than that given by Mr Watson. I also find that it would have been obviously reckless for any commercial lender to have relied on earlier other reports and appraisals. Mr Marshall's was in draft and was not a Red Book valuation. It referred to fair value rather than market value and said that it contained no detailed cash flow analysis for the development. Mr Perdomo's reports used comparable figures without discounting them (as should have been done for the reasons explained in the draft report of Mr Marshall). There were discrepancies in the areas covered. Moreover, the original contract was to buy the land as bare plots for a total of c. US$3.5 million and they remained in that state. There was no evidence that there was ever any change in the planning permission for the plots. As just explained such plots as were owned by Tenedora from 2017 onwards were not contiguous, and substantially the entire site was required for the proposed development to take place.

The Sanctuary investors

- Sanctuary was initially owned by Mr Golding's brother, Mr Ryan Golding (20%), Mr Mark Ingham (40%), and Mr Andy Woodcock (40%).

- Sanctuary marketed the sale of off-plan villas on The Hill before any development had taken place. Investors paid deposits. Sanctuary agreed to pay interest on the deposits and agreed that if an investor changed their mind, the investor did not have to pay the balance and acquire the property but could exercise an option to be repaid 120% of the deposit. Sanctuary took deposits from over 280 investors. Mr Ingham and Mr Barker were closely involved in this process.

- I find that the sales team who introduced purchasers to Sanctuary were paid 20% of the deposits.

- Mr Russell-Murphy was also involved. He sent invoices to Ecoresorts Sales Limited, a company which engaged in marketing the villas. Sanctuary made payments to him. He also had dealings with Sanctuary's investors.

- The investment scheme ran out of money and was unable to proceed with the development. The Hill remained an undeveloped, bare, plot.

- By early 2013 Sanctuary became unable to pay the monthly interest due to investors.

- At this stage Mr Hume-Kendall became involved with Sanctuary. He developed a rescue package for the Sanctuary investors. Mr Thomson was also involved.

- Mr Hume-Kendall and Mr Thomson were at the time directors of a company called Sustinere Group Plc, which was involved in developing the rescue package. Sustinere made payments to Sanctuary to prevent it becoming cash flow insolvent. Some of the shares in Sanctuary were transferred to Mr Thomson.

- By May 2014 at the latest, Mr Thomson became the owner of 100% of Sanctuary PCC on trust for Mrs Hume-Kendall, Mr Golding and his family, and Mr Thomson.

- In May 2013 Sanctuary sent letters to the Sanctuary investors about the rescue package involving Sustinere. The letters said that the investor was a regulated UK PLC formed 35 years ago and that its directors and managers had all previously held senior positions in some of the UK's largest firms and had a wealth of experience in the leisure and investment sectors. They also referred to Buss Murton as one of the UK's oldest and respected law firms. Mr Sedgwick was a partner in Buss Murton.

- In June 2013 there was a roadshow to promote the rescue package, led by Mr Hume-Kendall. At roadshow meetings, the investors were told that: (i) they would have the benefit of security through a UK trust holding security over the land at The Hill; (ii) there would be an improvement in the terms of the buyback option; (iii) their existing option over land at The Hill could be transferred to land at The Beach on the same terms; and (iv) monthly interest payments on sums invested would be restarted.

- In order to benefit from this package of rights, investors would need to pay an additional deposit amount. Most of the existing investors agreed to this deal. The additional deposits were paid to Buss Murton.

- Trust arrangements were put in place in respect of the deposits. I find that under these arrangements (a) the shares in Inversiones came to be held by Sanctuary PCC on trust for a company called El Cupey Limited, and (b) the single share in El Cupey Limited came to be held on trust for Sanctuary investors, whether or not they had signed up to the rescue package. Mr Thomson and Mr Hume-Kendall were the initial directors of El Cupey Limited.

- As explained below, there were various later reorganisations of the ownership structure. But throughout these changes the trust arrangements persisted, under which the shares in Inversiones (which owned The Hill) remained beneficially owned by the Sanctuary investors.

- New contractual arrangements were put in place for those Sanctuary investors who had agreed the rescue deal. The additional deposits from such investors amounted to c. £2.4 million.

- The monthly interest liability of Sanctuary to its investors was c. £88,000 per month from 2013 to the first half of 2016, at which point it reduced to £30,000 per month.

- The total liability of Inversiones to the Sanctuary investors in relation to their buyback options was recorded as £27,282,386 as at June 2017. This was the principal amount of the liability covered by the El Cupey trust arrangements at that date.

- I find that a large portion of the additional sums of c. £2.4 million raised under the rescue package were in the event paid to companies owned by Mr Golding, Mr Golding's brother, Ryan Golding, and Mr Hume-Kendall. They were not used in the development of either The Hill or The Beach.

- Specifically, One Monday Limited, a company associated with Mr Thomson, received payments of c. £1.2 million from Sanctuary. One Monday then made various payments in late 2013 and early 2014 including £535,000 to Clydesdale Property Developments Limited (Mr Golding's company), £200,000 to LV Management (Mr Hume-Kendall's company); £37,500 to Mr Thomson personally, and £50,000 to Ryan Golding.

- LV Management received a further £370,000 directly from Buss Murton's client account (where Sanctuary's funds were held) and £60,000 was transferred to Sustinere. As explained in more detail below, I am satisfied that Mr Thomson was in control of One Monday at the time of these payments and that he knew about them.

- Turning more specifically to Mr Thomson's role in these transactions, he had been a director of Sustinere since 22 March 2013. Mr Thomson directed Sustinere to provide financial support to Sanctuary in May 2013. As a director of Sustinere, Mr Thomson was involved in formulating the terms of the "rescue package" provided to Sanctuary in mid-2013. He explained in his witness statement that he "was involved in the planning and financing" of the Sanctuary project. Though he attempted in his oral evidence to distance himself from his involvement, I find that he was aware of the rescue deal and (as just explained) what happened to the sums paid through One Monday. He also knew that Sanctuary had sold villas off-plan to investors and that the villas had not been built. He also knew that Sanctuary had taken deposits from investors in the Sanctuary scheme and that interest payments were due to these investors.

- As already noted, Mr Thomson became a shareholder of Sanctuary in June 2013 and Mr Thomson came (by May 2014) to own 100% of Sanctuary PCC, which he held on trust for Mrs Hume-Kendall, Mr Golding and Mr Thomson.

- Mr Thomson was also a director of El Cupey Limited between 18 July 2013 and 1 August 2013. In this capacity, he signed a trust deed dated 30 July 2013 by which Sanctuary PCC agreed to hold its shares in Inversiones on trust for El Cupey. He therefore knew that The Hill was (through Inversiones) held on trust for the Sanctuary investors.

- Mr Thomson also signed the new contracts with the Sanctuary investors who had signed up to the rescue scheme on behalf of Sanctuary. I find that he was aware of the terms of those contracts. These included that additional payments made by the Sanctuary investors would only be distributed in accordance with the instructions of the trust in favour of the Sanctuary investors; and the trust would ensure that sufficient funds were paid out of the deposits into accounts reserved to pay for planning consents and other purposes that the trust considered to be in the best interest of the Sanctuary investors as a whole. These contractual arrangements were vague and loosely worded. But I find that the impression given to the Sanctuary investors who signed up to the rescue package was that the additional funds would be deployed in obtaining planning permission and then developing the land. It was not explained to those investors that the funds they were paying over would almost immediately be paid out to the shareholders or others interested in the ownership of Sanctuary.

- Mr Thomson also knew that additional deposits paid by Sanctuary investors who had signed up to the rescue package in an amount of c. £2.4 million were paid to Buss Murton; and that c. £88,000 was payable each month in interest payments to Sanctuary investors. Mr Thomson also knew, from an email sent to him on 14 May 2014 by Mr Sedgwick, that the potential liability of Inversiones to the Sanctuary investors was c. £23.5 million as at that date.

- Mr Thomson also knew that neither he, Mr Golding nor Mrs Hume-Kendall, had paid the previous owners of Sanctuary for the shares in Sanctuary or Sanctuary PCC.

- Mr Thomson also knew that because of the trust arrangements in favour of the Sanctuary investors, there was no free equity in The Hill.

- Mr Thomson denied in his oral evidence that he knew that The Hill had been purchased by Inversiones for £708,752. I find that he did know this. A copy of the agreement documenting the purchase was in LCF's books and records and a copy of the agreement was attached to an email sent to Mr Thomson by Mr Ingham on 9 May 2017.

- I find that Mr Thomson knew that Jonathan Marshall had produced a draft report in December 2013 that valued The Hill at US$7.3 million. He was sent the draft report by Mr Hume-Kendall on 24 December 2013. This report caused concerns because it was a lower value than had been anticipated. Mr Thomson was copied into the relevant emails.

- Mr Thomson said at various stages in his evidence that he did not read emails if the subject line indicated that it was within someone else's remit, even if the email was marked "urgent" and related to the accounts of a company of which he was a director. I reject this evidence. I find that, save where there is good reason to suppose otherwise, such as ill health at a given time, Mr Thomson in general read emails sent or copied to him. I find in this particular instance that he knew about the concerns about Mr Marshall's draft appraisal.

- I have already referred to the revised draft valuation report produced by Mr Marshall. Mr Thomson knew of this because it was sent to him by Mr Hume-Kendall on 30 March 2014. I have already commented on this. It was a draft desktop appraisal, not a Red Book valuation, and said it should not be relied on as a valuation report. Mr Thomson also knew from its contents that it omitted finance costs and that it was predicated on further income from the Sanctuary investors being available to fund the development of The Hill, when (as he knew) no such payments would be due until completion. I also find that Mr Thomson would have noted the substantial increase between the value in this and the earlier appraisal from Mr Marshall. As already mentioned, I find that no prudent businessman would have placed any reliance on this draft appraisal. It placed a value on the land at an amount hugely above the purchase price paid by Inversiones, despite almost nothing having been done since the date of the purchase. I find as a fact that Mr Thomson placed no reliance on it.

- Mr Thomson later made use of a May 2014 draft appraisal from Mr Marshall for The Beach which contained a figure of $37.9 million. I shall return to this. I find that no prudent lender could have placed any reliance on this heavily caveated draft desktop appraisal without requiring a proper Red Book valuation. Mr Marshall expressly said in the document that he did not conduct any due diligence on the development plans and the report stated, "You should therefore place limited reliance upon these figures and we would recommend that no irrevocable decision is taken with regard to the property without commissioning a formal valuation report". I find that Mr Thomson did not actually believe the land to have a value of $37.9 million or anything approaching it.

- I find that Mr Thomson knew that Tenedora had no valuable interest in The Beach. He knew that Tenedora had entered into an agreement giving it the right to acquire the plots of land comprising The Beach for the payment of a total sum of US$3.5 million but had not actually acquired them.

- I am also satisfied that Mr Thomson knew that until late 2017, Tenedora did not actually acquire any of the plots of land at The Beach. He claimed in oral evidence that he thought Tenedora had been proceeding with the purchase in the meantime. But he was informed by Mr Ingham, by email on 15 April 2016, that Tenedora did not own any of the land at The Beach and Mr Lee repeated this to Mr Thomson in an email on 16 March 2017. I reject Mr Thomson's evidence that he was unaware of these facts. This would have been particularly vital information for him as a director of LCF (as The Beach formed part of the supposed security for LCF's lending) and he would have been interested in its value. I find that he knew the truth.

- Though Tenedora eventually acquired some of the parcels making up The Beach in 2017, it never in fact acquired the parcels needed to enable the proposed development. I am satisfied that Mr Thomson knew this: he continued to have an interest in what was happening to the development and would have been told the true position.

- I have already mentioned that substantial payments were made to One Monday from the further sums raised from the Sanctuary investors. Mr Thomson was a shareholder of One Monday from 5 May 2010 until its dissolution on 2 February 2016 and was a director of One Monday from 9 May 2012. I find that throughout his time as a director, Mr Thomson controlled One Monday's finances and banking arrangements.

- Mr Thomson gave oral evidence that at some unidentified point early in the history, he had handed control of One Monday over to Mr Barker and Mr Michael Peacock and that Mr Barker was added to the bank account mandate. I reject this evidence. My reasons include these:

i. Mr Thomson was unable to say when the transfer of control happened. He said it was early in the history. He was then shown an email sent to him on 30 September 2013 referring to an agreement to which One Monday was a party. He said that it was not black and white and that there was a gradual handover period. He was unable to say when control of the bank account was supposedly handed over to Mr Barker. He eventually accepted that he could have been kept informed about payments made to and from One Monday and that he may have had a hand in administering the payments.

ii. Mr Thomson stated on a CV to be sent to the FCA in October 2016 that he was the managing director of One Monday. When confronted with this document he said in cross-examination that it would have been an old CV on file which Mr Huisamen had attached to an email. But he was then taken to an email dated 11 October 2016 which he sent to Mr Huisamen with the draft CV attached and which showed that he, Mr Thomson, had recently drafted the CV. The CV described him as the managing director of One Monday. I concluded that Mr Thomson's evidence about the CV was deliberately misleading.

iii. Mr Thomson's name was also referred to in a form provided to the FCA dated 16 October 2016 which stated that he was a director of One Monday. He signed the form. I reject Mr Thomson's evidence that this was filled out by Mr Huisamen and that he signed it without reading it. I reject Mr Thomson's evidence that he had been so casual: the form said that giving false information to the regulator could be a criminal offence. I find that he knew that it was sent in this form.

iv. Mr Barker was never placed on the banking mandate for One Monday (whereas Mr Thomson was).

v. I find it probable that both Ms Nicola Wiseman (who worked with Mr Thomson) and Mr Thomson attended a meeting with the Bank of Scotland in July 2014 to discuss various banking arrangements and at which getting Mr Thomson a debit card for the One Monday account was discussed. The email dated 21 August 2014 sent to Mr Thomson and Ms Wiseman by the BoS employee referred to a meeting the previous day and specifically identified some actions for "Nicky". This suggests that the meeting was with them both.

vi. There would in any case have been no reason for the separate debit card for Mr Thomson if he were no longer involved with One Monday. Mr Thomson could not explain this in cross-examination.

vii. Ms Wiseman kept Mr Thomson informed about One Monday's finances at least into 2014.

viii. Mr Thomson signed the LCF annual report dated 30 April 2015 which stated that he was a director of One Monday. He accepted in cross-examination that he had not by then told the accountants that he had handed over control of One Monday to Mr Barker and Mr Peacock.

ix. Oliver Clive, his accountants, wrote to Mr Thomson in October 2015 about the possible striking-off of One Monday, after the supposed handover of the Company to Mr Barker.

- I conclude that Mr Thomson's evidence that he had handed over control of One Monday's banking to others (and so lacked knowledge of its affairs) was a deliberate lie, which he told to distance himself from the damaging evidence that One Monday had been used as a conduit for paying a large proportion of the additional deposits made by Sanctuary investors to himself, Mr Golding, Mr Hume-Kendall and others; rather than it being used for the development of The Hill.

- I am satisfied that Mr Thomson knew that some £1.2 million of the additional deposits received from the Sanctuary investors was transferred from Sanctuary PCC's client account with Buss Murton to One Monday and that One Monday made the payments already identified. I also find that Mr Thomson knew that these payments made to the various individuals (or their companies) of parts of the additional deposits was contrary to the interests of the Sanctuary investors. He also knew that the investors had been led to believe that the additional deposits would be applied in the further development of the land.

- As to the involvement of Mr Golding in the dealings with Sanctuary, I am satisfied that:

i. Mr Golding's brother, Ryan, had been involved in Sanctuary from the outset. This is probably how Mr Golding became involved. Mr Golding participated in formulating the rescue package and its terms. The documents show that he was also aware of the trust arrangements involving El Cupey.

ii. Mr Golding knew that additional deposits paid by Sanctuary investors who had agreed to the rescue package amounted to c. £2.4 million and that c. £88,000 was payable each month in interest payments.

iii. Mr Golding knew that Mr Marshall's draft valuation of The Hill was for US$7.3 million and that this was lower than had been anticipated as the value for the site.

iv. Mr Golding and Mr Hume-Kendall decided not to proceed with the purchase of plots making up The Beach and that Tenedora therefore acquired no interest in land in that site before 2017.

v. Mr Golding received £535,000 from Sanctuary via One Monday and Clydesdale Property Developments. He knew that this money was not being invested in the land, as had been promised to investors.

vi. By May 2014 (and probably earlier), Mr Golding and his family were the beneficial owners of 71.25% of the shares in Sanctuary PCC. He probably had a beneficial interest in Sanctuary on the earlier dates when Mr Thomson acquired legal title to shares in it.

- As to the involvement of Mr Sedgwick, I am satisfied that:

i. Mr Sedgwick arranged for payments to be made from LCCL to Sanctuary via Sustinere.

ii. Mr Sedgwick knew of the creation of a rescue package by Mr Thomson and Mr Hume-Kendall as directors of Sustinere, and of the terms of the rescue package.

iii. Mr Sedgwick managed the receipt of additional sums of c. £2.4 million paid by the Sanctuary investors under the terms of the rescue package. These were paid into Sanctuary's client account with Buss Murton.

iv. Mr Sedgwick wrote to the Sanctuary investors setting out the terms of the revised agreement (which was with Inversiones) and enclosing a new contract. He was therefore aware of the terms of the revised contracts with the Sanctuary investors. I find that he knew that the investors were given the impression that the additional deposits would (at least very substantially) be applied in obtaining planning permission and developing the land; and that investors were not told that a large portion of their money would immediately be paid out to those interested in the shares in Sanctuary.

v. Mr Sedgwick made payments from Sanctuary's client account with Buss Murton to One Monday, Sustinere and LV Management (which I find he knew was Mr Hume-Kendall's company). I am satisfied that Mr Sedgwick knew that this was contrary to the impression given to the Sanctuary investors.

vi. Mr Sedgwick also made payments from Sanctuary PCC's client account to Mr Russell-Murphy. He therefore knew of the amount of the commissions being paid to Mr Russell-Murphy.

vii. Mr Sedgwick engaged in setting up the trust arrangements by which Sanctuary PCC held its shares in Inversiones on trust for El Cupey. Mr Sedgwick witnessed Mr Thomson's signature on the trust deed dated 30 July 2013 and executed by Sanctuary PCC and El Cupey; and sent the signed trust deed to Messrs Thomson, Hume-Kendall and Andrew Visintin. He was also aware of the subsequent continuations of those trust arrangements. Mr Sedgwick was also involved in preparing a further trust deed by which Buss Murton Nominees agreed that it would hold the share in El Cupey on trust for the Sanctuary investors. Mr Sedgwick knew, because of his involvement in the El Cupey trust arrangements, that Sanctuary PCC itself did not have any equity in the land.

viii. Mr Sedgwick also knew that c. £88,000 was payable each month in interest payments to the Sanctuary investors, and that the potential liability of Inversiones to the Sanctuary investors was c. £23.5 million.

Paradise Beach

- The next asset to address was called Paradise Beach. This was a resort in Cape Verde. It was owned by a company called Paradise Beach SA. A company called Stirling Mortimore had a purchase contract and agreed to assign its position to CV Resorts, the intended purchaser (a company associated with Mr Golding, Mr Hume-Kendall and others). By a contract with Paradise Beach SA executed on 13 April 2015, CV Resorts agreed to pay various sums for phases of the development. The constituent elements and payment instalments required CV Resorts to pay c. €57 million (c. £41 million at the then exchange rate) to acquire the resort.

- In closing submissions, Mr Sedgwick contended that 30% of the price had already been paid by the date of the contract because CV Resorts took over the deposits that had been paid by the previous purchaser. He did not however give evidence and his assertion could not be evaluated in cross-examination. On the documents and evidence before the court (including (a) the contracts in fact signed with Paradise Beach SA in April 2015, (b) the revised contract of May 2016: see below and (c) a spreadsheet circulated by Mr Sedgwick, which said that the only amount deemed to have been paid was c. €184,000) I am satisfied that €57 million was payable.

- In August 2015 Savills advised Mr Thomson that the market value of the site was c. €40.5 million. Savills also advised that the "worth value" (the value to the owner or prospective owner such as for investment purposes) was €56.72 million.

- In light of Savills' valuation, the right to acquire Paradise Beach with a market value of €40.5 million for a price of €57 million was therefore worthless. Mr Thomson (who had been given a preliminary opinion of value by Savills in July 2015) said in an email dated 20 July 2015 that they would be "overpaying by quite a margin".

- It will also be noted that Savills sent an email to Mr Thomson on 26 August 2015 which said that with a reduced marketing period (and other negative assumptions) the site would have a market value of €17.6 million.

- In the event, none of the land at Paradise Beach was actually acquired. There remained simply a contractual right to acquire the site on paying the sum of €57 million.

- As things transpired CV Resorts failed to pay the instalments due under the contract and this led to a legal dispute with Paradise Beach SA. Paradise Beach SA wrote a letter on 19 November 2015 claiming that CV Resorts was in breach of contract. It said that if CV Resorts did not remedy all its breaches, the contract would be terminated.

- This dispute continued and ultimately it resulted in an agreed variation to the terms of the purchase agreement in May 2016, which postponed the dates for the payment of the instalments. The total price remained €57 million.

- CV Resorts again failed to pay the instalments, and the dispute with Paradise Beach SA was revived. This continued during 2016 and into 2017. Paradise Beach SA gave notice terminating the contract in June 2017.

- I am satisfied that CV Resorts never acquired Paradise Beach and that the right to acquire the site did not have any value.

- Mr Thomson was a director of CV Resorts between 23 January 2015 and 15 August 2015 and was therefore a director at the time at which CV Resorts entered into the contract with Paradise Beach SA.

- I find that Mr Thomson participated in arranging the Paradise Beach deal, along with Mr Hume-Kendall, Mr Golding, Mr Sedgwick and Mr Ingham. He met the beneficial owners of Paradise Beach SA, Messrs John and Ned Cotter. He accepted in his witness statement that he "had some hand in" making a working financial model of the estimated values of the properties. He attempted to downplay this somewhat in cross-examination, but I conclude it is likely that he was involved. He obtained the valuation of the site from Savills. As one of the two directors of CV Resorts, he was included with Mr Hume-Kendall in communications relating to the drafting of the agreement with Paradise Beach SA.

- As already explained, Mr Thomson therefore knew that the market value of the Paradise Beach site was substantially less than the €57 million that CV Resorts was required to pay to acquire it.

- Mr Thomson was also given a copy of the variation agreement of May 2016, which maintained the €57 million price. I am satisfied that he was aware of the dispute between CV Resorts and Paradise Beach SA and knew that CV Resorts had not paid any of the sums due under the contract.

- By an email of 6 February 2017, Mr Sedgwick informed a Cape Verde lawyer that LCF "are ready to provide the €2 million to purchase the first set of units but they require proper security". It is probable that Mr Sedgwick had previously discussed this with Mr Thomson. I am satisfied that this shows that Mr Thomson was aware that, by that date, no units had been acquired. Mr Thomson also knew that CV Resorts had still not completed the purchase of any of the units at Paradise Beach by 21 April 2017 from an email to Alex Lee, copied to Mr Thomson, saying, "CV Resorts does not at the moment have any property in its name only the contracts to acquire the land in the Cape Verde". Mr Thomson said he could not remember this email in his oral evidence. I consider it likely that he read this and other emails as a matter of practice as they affected the security given to LCF.

- Mr Thomson said in his evidence that he thought CV Resorts was in fact buying units. There was no contemporaneous evidence supporting that and the emails just referred to show that he knew until at least until mid-2017 that no units had been bought. He was unable to explain these, other than to say that he did not read emails unless the subject line showed he had to. I have rejected this evidence.

- No units were in fact purchased and the contract was terminated by the sellers in June 2017. I find it inherently improbable that any of the people then involved would have lied to him about this. I conclude that his oral evidence that he thought that units had been bought at some stage was deliberately untruthful.

- I am also satisfied that Mr Thomson knew that CV Resorts never acquired any interest in the Paradise Beach resort (other than the right to buy it for substantially more than its market value).

- Mr Golding was also involved in arranging the Paradise Beach deal, along with Mr Thomson, Mr Hume-Kendall, Mr Sedgwick and Mr Ingham. Mr Golding knew that CV Resorts had defaulted under the agreement because he was forwarded the letters dated 19 November 2015 and 15 February 2016 from Paradise Beach SA in which the defaults of CV Resorts were set out.

- The first of these letters was forwarded by Mr Sedgwick to Mr Barker who, it is to be inferred, passed it on to Mr Golding. I find that Mr Barker generally communicated his knowledge of material events to Mr Golding. Mr Barker was Mr Golding's right-hand man and functioned as his nominee in holding shares. Mr Golding had been disqualified as a director and sought to keep his involvement in the various companies hidden.

- The second letter concerning the dispute with Paradise Beach SA was forwarded directly to Mr Golding by Mr Sedgwick. On 23 February 2016 Mr Golding received an analysis prepared by Mr Sedgwick of the claims made against CV Resorts by Paradise Beach SA.

- Mr Golding was then involved in discussions with John and Ned Cotter to resolve the dispute and authorised the entry by CV Resorts into the variation agreement in May 2016.