This judgment was delivered in public. The judge has made a direction that the children of the parties are not to be named, nor any photograph of them printed, in any report of the proceedings or this judgment. This direction does not prevent the parties being named. All persons, including representatives of the media, must ensure that this direction on is strictly complied with. Failure to do so will be a contempt of court.

Mr Justice Mostyn:

1. I shall refer to the appellant as ‘the mother’ and to the respondent as ‘the father’.

2. The mother is 50 and is a journalist although she is not currently working. She has a degree in Russian and Eurasia Affairs, a Masters in International Relations and a PhD. She lives in Oxfordshire with her husband who she married in August 2022 and the parties’ two children who are 12 and 10 years of age. The parties’ children are privately educated and the father pays for their school fees and extras.

3. The father is 47 and works in private equity. He lives in London with his wife who he married in January 2020 and their two children, a 2-year-old and 1-month-old.

4. The parties married on 14 December 2010 and their marriage lasted for 2 years. The mother petitioned for divorce in February 2013 which was duly granted.

5. The mother applied for financial remedies which were settled by a consent order made on 3 July 2014. The total assets of the parties comprised a house with equity of £700,000. The order provided for the mother to receive a total of £525,000 in cash to be paid by the father in instalments in part linked to the size of the father’s bonus over a period potentially as long as 10 years. The father was to pay (a) child maintenance of £10,000 per annum per child and (b) spousal maintenance of £52,000 per annum until 2024, thereafter decreasing to £40,000 per annum payable until the younger child reached the age of 18 or finished her full-time secondary education if earlier (i.e., potentially for a further 16 years).

6. In 2014 the mother removed the children from their schools, moved to Oxford with them and withheld contact with the father. Proceedings under the Children Act 1989 ensued which were resolved by consent in September 2014, the father having agreed to the relocation and contact resuming.

7. Unfortunately, there have since been repeated proceedings relating to the children. There have been three separate sets of proceedings regarding the father’s general or holiday contact with the children. In addition, in 2018 the mother applied for permission to relocate the children to Pakistan where she had obtained employment. This application was refused by Theis J in April 2018. The mother took up the position nonetheless and the father assumed primary care of the children. In October 2018 the mother retained the children in Pakistan following an agreed holiday visit by the children to her there. The mother sought to ratify this unlawful conduct by applying again for the children to be allowed to relocate to Pakistan; this was refused by Theis J in February 2019. The mother thereafter returned to this jurisdiction and a child arrangements order was made by Theis J which provided for the parties to share the care of the children, so that they lived principally with the mother and spent time with the father every other weekend and in the school holidays. That order was in force as at the date of the hearing in September 2022 before HHJ Vincent with which I am concerned. Those contact arrangements had again been breached by the mother and a yet further set of Children Act proceedings were in train as at the date of that hearing.

8. In 2015 the mother applied to vary the consent order of 3 July 2014 to accelerate receipt by her of the cash element so as to rehouse herself and the children. A consent order dated 17 July 2015 varied the dates on which the father was to make payments to the mother. £350,000 originally ordered to be paid in instalments potentially stretching to 2024 was now to be paid no later than February 2018. The quid pro quo was a variation of the global annual spousal and child maintenance to bring forward the step-down from £72,000 to £60,000 from August 2024 to February 2020.

9. By July 2015 the mother had received a total of £490,000 from the father under the terms of the 2014 and 2015 orders, at which point she purchased a cottage in Oxfordshire for £460,000.

10. In January 2020 the father remarried. At the time of the hearing before the judge he and his wife had a child born in October 2020.

11. The mother began a relationship with Mr James in early 2020. He purchased a country house in May 2021 and the mother and children then moved into it with him. She married Mr James on 23 August 2022.

12. On 5 January 2021, the mother applied to vary the consent order of 17 July 2015, seeking increased payments of spousal and child maintenance. It is those proceedings that were determined by HHJ Vincent and with which I am concerned on appeal.

13. The mother should have disclosed in the proceedings her cohabitation with Mr James as soon as it happened in May 2021. She did not do so, and only definitively confirmed that fact in her s. 25 statement dated 16 March 2022 . Remarkably, the mother’s case in that statement was that although she was cohabiting with Mr James she nonetheless should be awarded capitalised spousal maintenance.

14. The mother disclosed her remarriage to the father on 1 September 2022.

15. The FDR took place on 20 September 2021. Neither party had made open offers beforehand. The father made an open offer after the FDR for spousal maintenance to cease and for child maintenance to continue to be paid at the current level. The mother never made a reasoned open offer.

16. The variation application was listed to be heard on 15 March 2022. The mother applied for an adjournment which was refused on 3 March 2022. She was ordered to pay the father ’s costs of the application. However, the final hearing was later removed from the list due to the lack of judicial availability.

17. The final hearing took place on 15 and 16 September 2022 before HHJ Vincent. The mother accepted that she no longer had a claim for spousal maintenance. Her case before the court was that the existing child periodical payments were insufficient to meet their needs; that there was a disparity of lifestyle between her and the father; and that she had accrued substantial debt. It was submitted on her behalf that “the Mostyn formula” should apply to the calculation of child maintenance so that she should receive child maintenance of £2,184 per child per month, a substantial increase of the existing order of £833 per month per child. At the final hearing the father offered to increase this to £1,100 per month per child, as well as to pay school fees and extra-curricular activities.

18. Prior to the hearing the father had applied under section 33 of the Matrimonial Causes Act 1973 for repayment of £48,000 of spousal maintenance. He also had applied to enforce an indemnity given in the 2014 order. He sought an order for costs and enforcement of the costs order made against the mother on 3 March 2022.

19. HHJ Vincent handed down judgment on 6 December 2022. She found that the children’s needs had not substantially changed since the time that the previous orders were made. She adopted the father’s proposal and ordered him to pay the mother child maintenance of £1,100 per month per child, amounting to £26,400 per annum. Second, she ordered the father to pay the children’s school fees as well as school travel and other extras. She held the mother to her indemnity given on 3 July 2014 in the sum of £3,598. Finally, she ordered the mother to pay half of the father ’s costs, summarily assessed at £66,627.70. She did not order the mother to repay to the father any spousal maintenance.

20. The judgment is reported on Bailii as A Wife v A Husband [2022] EWFC 154.

21. Permission to appeal was refused by HHJ Vincent on 9 December 2022.

22. The mother filed her appeal notice and grounds of appeal in the High Court on 12 December 2022. On 19 December 2022 Roberts J ordered that the application for permission to appeal (PTA), with the appeal to follow if permission was granted, were to be heard by me together on 5 April 2023.

23. There are three grounds of appeal:

i) Ground 1: the judge failed to follow the approach set down in leading authorities that the ‘starting point’ for a child maintenance calculation should be the figure given by the CMS formula up to incomes of £650,000.

ii) Ground 2: the assessment of the quantum of child maintenance was too low and insufficient (or no) weight was placed on the inevitable disparity of lifestyle as a consequence.

iii) Ground 3: the order as to costs was wrong.

24. The test for the grant of PTA is arguability. The standard for allowing an appeal is wrongness (FPR r. 30.12(3)(a)).

25. The mother’s case advanced to me by Mr Finch was that the judge disregarded the authorities on child maintenance and did not provide an adequate reason for departing from the starting point proposed therein; that she unfairly disregarded the principle that the children’s lifestyle should not be out of kilter with their father’s when she overly harshly reduced the mother’s budget; and that the costs order was wrong insofar as the mother’s late filings had no bearing on the proceedings whatsoever.

26. The father ’s case advanced to me by Mr Tatton-Bennett was that the judge was entirely entitled within her discretion to have departed from this starting point; that the child maintenance ordered was entirely in kilter with the father’s lifestyle; and that the costs order was justly made in circumstances where the mother had been dishonest about the issue of cohabitation, had sought to capitalise her spousal maintenance when she had remarried, and remarkably had violated every procedural direction (13 altogether) requiring her to take steps in the proceedings.

27. I now turn to the individual grounds.

Ground 1: “The judge failed to follow [the] approach set down in leading authorities that the ‘starting point’ for a child maintenance calculation should be the figure given by the Child Maintenance Service formula applied up to incomes of £650,000.”

28. 20 years ago, in GW v RW [2003] EWHC 611 (Fam) I suggested that, where the court has jurisdiction, a useful starting point (and normal finishing point) in assessing the quantum of child support maintenance (CSM) to be paid by the father would be the figure given by the statutory formula.

29. In Re M-M (Schedule 1 Provision) [2014] EWCA Civ 276, [2014] 2 FLR 1391 the Court of Appeal approved my suggestion. At [38] McFarlane LJ stated:

“In this case the child support scheme has no direct application as the father lives abroad. However, in my view, it is informative to consider what the position would be were he to be resident in England and Wales.”

30. The following year I expressed the view in Re TW & TM (Minors) [2015] EWHC 3054 (Fam) that even where the father’s income for child support purposes exceeded the statutory ceiling, but was not “unadjacent” to it, the formula would continue to provide useful guidance. At [7] I stated:

“It would be an example of arbitrary law-making if the computation of child maintenance were radically different depending on whether it was done by the secretary of state under the 1999 Act or whether it was done by a court under sch.1 of the Children Act or s.23 of the Matrimonial Causes Act. Consistency of approach is obviously desirable in order to satisfy the need for the law, particularly in these days when so many people are unrepresented, to be predictable and accessible. Arbitrariness is to be avoided wherever possible.”

31. In CB v KB [2019] EWFC 78 at [49] I went further and suggested that for incomes up to £650,000 the formula would give useful guidance.

32. In Collardeau-Fuchs v Fuchs [2022] EWFC 135 at [120] - [121] I qualified that view to make clear that the formula would be irrelevant where the claim was for the type of CSM award which I described at [109] and [129(b)] as a Household Expenditure Child Support Award or HECSA, but would continue to provide useful guidance in a case seeking a conventional assessment of the contribution that the father should make to the children’s direct and indirect costs (where the indirect costs comprise a fair proportion of utility bills, council tax and other infrastructural expenses referable to the children’s primary residence).

33. That view was followed by Cobb J in Re Z (No 4) (Schedule 1 award) [2023] EWFC 25 at [21].

34. I continue to believe that the formula provides a useful and logical starting point in a child maintenance case, whether heard under the Matrimonial Causes Act 1973 or under Schedule 1 to the Children Act 1989, where

i) the income of the father for child support purposes is more than the statutory ceiling of £156,000 but less than £650,000; but

ii) where the application does not seek a HECSA but a conventional assessment of the quantum of CSM; and

iii) where it is not a variation application.

35. Mr Finch has told me that there are now about 629,000 taxpayers earning more than £150,000, a 2.3-times increase in the ten years since the ceiling of £150,000 was introduced. In contrast there are only around 40,000 taxpayers earning more than £600,000. Given the large number of taxpayers earning between £150,000 and £600,000, there will likely be a correspondingly high number of child maintenance cases where the earnings will fall in that range. It obviously makes sense to seek to have simple, clear and logical guidelines to help parents settle such cases, and where they do not settle, for the Financial Remedies Court to be able to decide them consistently and efficiently.

36. However, on reflection, I do accept Moor J’s criticism in CMX v EJX (French Marriage Contract) [2022] EWFC 136 at [86]:

“I have to decide on periodical payments for C. I have jurisdiction as there has been a maximum CMS assessment of £15,288 per annum. Mr Boydell refers me to a decision of Mostyn J in CB v KB [2019] EWFC 78 in which he suggested that the easiest way to calculate the top-up maintenance was to apply the same rate as the CMS to the Husband’s income, namely 9.8% between the CMS maximum of £156,000 and an income of £650,000. This would give a total award of £63,804 per annum in this case. I do, of course, accept that the beauty of the decision of Mostyn J is that it makes it easy to calculate the figure, so avoiding dispute. There are, however, significant disadvantages. There were four children in CB v KB so the Wife got £12,600 per annum per child. Given that I have to apply section 25, it is impossible to see why the Wife in CB v KB gets £12,600 per child but this Wife receives £63,804 for one child just because the two eldest children in this case are no longer part of the calculation. If they were, the figure would reduce to £21,268 each.”

37. While the formula does make adjustments for the number of children, its primary driver is the percentage of F’s adjusted gross income to be paid in child support maintenance. This leads to the per capita anomalies identified by Moor J. The amount that would be payable under the formula where the father’s income is £650,000 (and there is no shared care, and no other child living with him) is (when rounded to the nearest £1,000) £60,000 for a single child, £40,000 for each of two children, and £33,000 for each of three children. While it is true that there will be economies of scale where there is more than one child in a family unit, it is obvious, at least to me, that a single child does not cost anything like 50% more to rear than each of a pair of children, let alone 80% more than each of a trio of children.

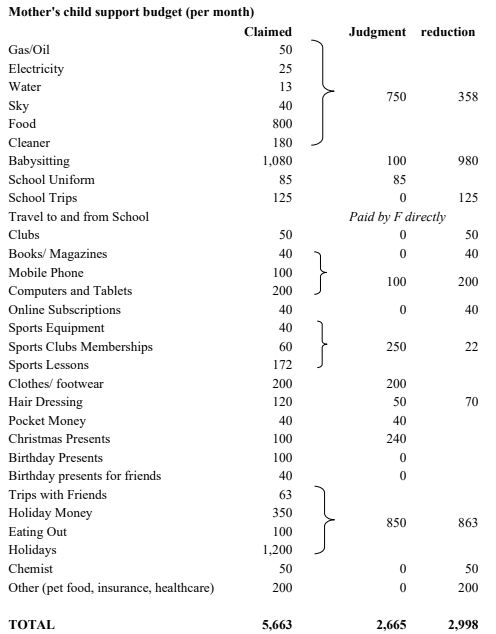

38. The second, and arguably more important criticism, which I also acknowledge having subjected the data to intense scrutiny, is that the amounts generated by an extension of the formula to incomes up to £650,000 are consistently higher, in my fairly considerable experience, than the levels of awards typically made by the court, whether by consent or otherwise, in conventional (i.e., non-HECSA) cases. It is true that the figures would be reduced if there was a degree of shared care but that mitigation does not alter the fact that the headline figures produced by an extension of the formula to incomes in the range £156,001 - £650,000 are unrealistically high and are in my opinion unhelpful as starting points. In the Appendix to this judgment, I have included a table (Table 1) which gives the full range of figures produced by the application of the formula to that range. This shows that at every level the figures produced are plainly excessive and that the calculation for a single child is not reasonably proportionate to the calculation for a child in a sibling duo or trio.

39. In my opinion, the reconciliation of these criticisms with the “beauty” (as Moor J put it) of having a formula-based starting point is achieved by making an adjustment to the functioning of the formula for the income range £156,001 - £650,000. I have set out the adjustments and how they might work in the Appendix to this judgment. The Appendix describes what might be called an Adjusted Formula Methodology (or AFM) to give a Child Support Starting Point (CSSP).

40. I would like to think that this AFM, or something like it, might be used to help settle, or to help decide, what I suspect will be an increasing number of child support cases where the income of F lies between £156,001 and £650,000.

41. I make it clear, however, that if (i) there are 4 or more children for whom CSM is to be paid, or (ii) E is more than £650,000, or (iii) F’s income is largely unearned, or (iv) F lives on capital, then use of the AFM is not apt. Any figure thus calculated could be misleading as a starting point. In such circumstances CSM should be worked out by reference to the statutory provisions, without using the AFM and without the benefit of a CSSP .

42. If the application is for a variation of an existing child maintenance order, the AFM should not be used. The terms of section 31(7) Matrimonial Causes Act 1973, and of para 6(1) of Schedule 1 of the Children Act 1989, require identification of the changes of circumstances since the original order was made. This means that the value of the original order adjusted by inflation should normally be used as the CSSP.

43. I emphasise that child support can only lawfully be awarded if the discretionary balancing exercise mandated by s25(3) Matrimonial Causes Act 1973 or para 4(1) of Schedule 1 of the Children Act 1989 has been undertaken. Every child maintenance case, whether it is formulated as a claim for a HECSA or for a conventional award, requires a budget, which the court will consider carefully, holding in mind a relevant CSSP. I emphasise that at its highest the AFM produces a loose starting point which a decision-maker can summarily choose to accept or reject without fear of appellate review. That is what the judge did in this case. She dismissed the reliance by the mother on the figure produced by the formula as “misconceived” (see para 141). She was completely entitled to do so, and her decision to have no regard to the formula result lay within her unfettered discretion.

44. When the judge gave her judgment on 6 December 2022 Collardeau-Fuchs v Fuchs, CMX v EJX (French Marriage Contract) and Re Z (No 4) (Schedule 1 award) had not been reported. In the light of these and the earlier authorities, Ground 1 was plainly arguable, but my clear conclusion is that it cannot be said that the judge’s refusal to take into account the result of the formula was wrong. The appeal on Ground 1 is therefore dismissed.

Ground 2: “The assessment of quantum of child maintenance was too low and insufficient (or no) weight was placed on the inevitable disparity of lifestyle as a consequence.”

45. This being a variation case the appropriate CSSP was the value of the current order adjusted by inflation. The order was fixed at £10,000 per annum per child on 3 July 2014. The value of that order adjusted by the CPI as at the date of hearing on 15 September 2022 was £12,392 (when adjusted by the RPI it was £13,578).

46. If this case were not a variation application and the AFM was used the CSSP would have been £10,300, calculated as follows:

|

H earnings 2020/21 |

424,658 |

Note 1 |

|

reduce by 11% for one other child in household |

(46,712) |

Note 2 |

|

Pension |

(4,000) |

Note 3 |

|

school fees etc grossed up |

(78,387) |

Note 4 |

|

Exigible earnings for child support purposes: |

295,558 |

|

|

rounded to |

295,000 |

|

|

Adjusted formula result per child |

10,300 |

Note 5 |

| |

|

Note 1: F’s 2021/22 tax return would not have been available until January 2023. His historic earnings are therefore to be used to give a gross weekly income on the effective date of the calculation

Note 2: F’s weekly income is to be reduced by 11% as F then had one other child living in his household

Note 3: I have assumed F is making pension contributions as at the effective date of the calculation in the amount of the reduced annual allowance of £4,000 for someone of these earnings.

Note 4: School fees of £33,000 + extras of £6,000 + school bus £4,113 = £ 43,113. £43,113 ÷ 0.55 = £78,387

Note 5: Under the child arrangements order F should have had the children with him for no less than 108 nights each year, entitling a reduction of 2/7ths .

47. This figure of £10,300 is rather less than either of the CSSP figures applicable in a variation case. It is thus doubly irrelevant and I need say no more about it.

48. The father’s proposal was £13,200 per child, and this was held by the judge to be fair. As it happens, it was extremely close to the two figures that could have been used as a CSSP viz £12,392 and £13,578.

49. The mother produced a budget, late in the day, formulated on the conventional basis (as explained above), claiming £5,663 per month. Between paras 107 and 126 the judge went through the budget with scrupulous care and decided that the true fair cost of the children was £2,665 per month. The following table shows the sums claimed, allowed and disallowed:

50. As explained above, the judge adopted the father’s proposal of £2,200 per month, leaving the mother to meet a shortfall of £465 per month. The judge decided that this was well within mother’s capacity to meet, either by exploiting her earning capacity, or from the return on, or the value of, her former home which she had rented out following her cohabitation with Mr James.

51. The overall sum to be paid by the Father under the varied order would be as follows:

|

CSM |

26,400 |

|

school fees |

33,000 |

|

extras |

6,000 |

|

school bus |

4,113 |

|

69,513 |

If this amount were to be seen as paid by F from that part of his income taxed at his top rate then the payments account for £126,300 of his pre-tax remuneration. This represents 33% of his gross earnings excluding pension payments.

52. I turn to the mother’s argument before me that, as a result of the level of child maintenance ordered by the judge, the lifestyle of these children, living with their mother and stepfather, would be out of kilter to that enjoyed by the father and his new family.

53. Generally speaking, this comparison is only meaningful where the child maintenance claim is for a HECSA.

54. The variation sought in this case was not for a HECSA. It was for a conventional assessment of CSM. At para 146(f) the judge held:

“The argument that there should be an increase in maintenance to reflect the 'disparity of lifestyle' is ill-founded. Firstly, it is questionable whether there is any real disparity. If anything, the wife now enjoys a significantly more luxurious lifestyle than the husband and his wife. She does not work whereas they are both working and incurring childcare costs. Secondly, this was an exceptionally short marriage and there is no obligation upon the husband to continue to account to her for any share of his income or for there to be parity. If either of them were to inherit large sums of money or win the lottery they would not be required to account to the other for a share, and nor do they need to in the event of an upturn in income.”

55. I agree with this and would add that it would have been invidious for the judge to have attempted a detailed comparison of lifestyles of the two households in circumstances where very little was known about the mother’s new husband other than that he is clearly of means being a successful figure in the aviation world, and the owner of a fine country house where he lives with the mother and the children.

56. It is clear to me that the judge undertook the section 25(3) Matrimonial Causes Act 1973 exercise impeccably. It is not arguable that her decision was wrong.

57. Permission to appeal under Ground 2 is therefore refused.

Ground 3: “The order for costs was wrong”

58. Between paras 169 and 195 the judge exhaustively analysed the principles governing a claim for costs. She formulated the following summary of the principles, which she then applied to the litigation conduct of the mother.

i) Deliberate non-disclosure or other dishonest behaviour aside, a refusal to negotiate openly amounts to serious misconduct in respect of which the Court will consider making an order for costs: OG v AG [2020] EWFC 52 at [30].

ii) A failure by a party (Party A ) to explain the basis of a claim, or a failure by her to comply with the court’s procedural directions aimed, inter alia at requiring her to give a true picture of her circumstances, will have the effect of preventing the other party (Party B) from gaining a clear view of the financial landscape and is tantamount to a refusal by Party A to negotiate openly.

iii) Making a ludicrous claim (such as a demand for an award of capitalised spousal maintenance advanced after she has admitted she is permanently cohabiting with another person) which has the effect of stymying any chance of settlement is also tantamount to a refusal to negotiate openly.

iv) Where Party A has been guilty of an actual refusal to negotiate, and/or is treated as having refused to negotiate by (a) a failure to give clear and honest evidence about all material facts and/or (b) by making a ludicrous claim, then it will be fair and proportionate to require Party A to pay all or some of Party B’s costs provided that the court is satisfied that Party A has the means to do so.

59. I fully agree with these principles and endorse them as strongly as I can. In my opinion they should become widely known. In my opinion they should be printed out and handed to all financial remedy litigants at the very beginning of every case.

60. In this case the judge found the mother guilty of breach of all of these principles and concluded her findings thus:

“188 I agree with the submissions made on behalf of the husband that the wife's litigation conduct has been such that what would otherwise have been a relatively straightforward case has become needlessly complex. I take into account that it cannot be said that each and every episode of poor litigation conduct can be linked to wasted costs, but I am entitled to look at her conduct as a whole. In my judgment, taken as a whole, it has led to an unnecessary waste of time and expense and has prevented the parties from entering into meaningful negotiations in what should have been a straightforward case.

190 In my judgment it is appropriate to exercise my discretion so as to make a costs order against the wife as a result of her litigation conduct. I am satisfied that the husband has been put to significant additional expense as his solicitors have had to (i) chase the wife in respect of her non-compliance with Court orders; (ii) respond to the ever-changing cohabitation issue.

191 In addition, her failure to set out her position at an early stage, invite negotiations, or make an open offer (until 6 September 2022) has meant that the application proceeded inexorably on to an expensive contested final hearing. The application has essentially failed, as the change of circumstances argued for has not been identified. The Court has made an award which is consistent with the position put forward by the husband.”

61. The father’s costs amounted to £133,253.40. The judge considered that the mother’s conduct, which had the effect of stymying settlement and drove the parties into a two-day final hearing, had to be marked by an order for costs. Her decision, which might be regarded as merciful, was that the mother should pay only half of those costs namely £66,627.

62. The judge was satisfied that the mother had the means to pay those costs, holding at para 194:

“The financial effect on the wife of this order is not unmanageable because she has the resource to meet the costs from her unutilised earning capacity, or by generating rent or capital from [her house].”

63. In my judgement Ground 3 is not arguable. Permission to appeal is refused on it.

Conclusion

64. Accordingly, the formal disposal of this appeal is that:

i) permission to appeal is granted on Ground 1, and the appeal is dismissed; and

ii) Permission to appeal is refused on Grounds 2 and 3.

For the avoidance of any doubt I give permission for this judgment to be cited notwithstanding that it refuses permission to appeal on two of the three grounds.

Anonymity

65. My only reproach of the excellent judgment of HHJ Vincent is that it has been anonymised. It is true that the hearing before her, being in private and mainly concerned with child maintenance, technically fell within s. 12(1)(a)(iii) of the Administration of Justice Act 1960. Therefore, the publication of “information relating to the proceedings” would, in the absence of an order lifting this secrecy be a contempt of court. However, s. 12 does not cast a blanket reporting ban over this case, and it does not prevent the parties, or the children being identified in any report of the proceedings. Absent an order under s.12(1)(e), or under the common law, the following could have been reported:

i) that the proceedings relate mainly to the maintenance of a minor;

ii) the name, address or photograph of the children.

iii) the name, address or photograph of the mother and father;

iv) the text or summary of the whole or part of the orders made in the proceedings.

See Re PP (A Child: Anonymisation) [2023] EWHC 330 (Fam) at [9].

66. The judge’s judgment bears a rubric:

“IMPORTANT NOTICE This judgment was delivered in private. The judge has given leave for this version of the judgment to be published on condition that (irrespective of what is contained in the judgment) in any published version of the judgment the anonymity of the child[ren] and members of their [or his/her] family must be strictly preserved. All persons, including representatives of the media, must ensure that this condition is strictly complied with. Failure to do so will be a contempt of court.”

I have not seen a reporting restriction order made under s.12(1)(e) of the 1960 Act, or under the common law, in the terms of this rubric, and I do not believe that one was made.

67. I cannot identify any good reasons why the judge’s judgment should be subjected to the secrecy referred to in the rubric, or even to that level of secrecy provided for in s. 12 of the 1960 Act. There is nothing in the judgment which:

i) recognises that anonymisation is a derogation from the core principle of open justice;

ii) sets out the findings made by the court, applying a test of necessity, in an intensely focussed balancing exercise when determining whether to impose anonymity on the proceedings;

iii) sets out the court’s reasoning why it was necessary and proportionate, in order to enable justice to be done, to grant anonymity; or

iv) sets out the terms of the anonymity order.

See TT v Essex County Council [2023] EWHC 826 (Admin) at [76], where I sought to summarise all the recent case-law.

68. This appeal was heard by me in public in the normal way. Where an appeal is heard in public any report of the proceedings and of the appeal judgment may name names unless there has been an order prohibiting the same. I have received no application or evidence asking for me to do so.

69. I propose to lift the secrecy imposed by s.12 and the rubric (assuming that the rubric was effective to do so) in respect of the proceedings before, and the judgment by, HHJ Vincent. However, I cannot see any good reason why justice requires the two children to be named, or their photographs printed, in any report of the appeal proceedings or of this judgment or of the judgment of HHJ Vincent. This judgment therefore contains a rubric which says:

“This judgment was delivered in public. The judge has made a direction that the children of the parties are not to be named, nor any photograph of them printed, in any report of (i) these appeal proceedings, or (ii) this judgment, or (iii) the proceedings at first instance, or (iv) the judgment of HHJ Vincent dated 6 December 2022. This direction does not prevent the parties being named. All persons, including representatives of the media, must ensure that this direction is strictly complied with. Failure to do so will be a contempt of court.”

70. It is my opinion that a rubric such as this only acts as a warning notice of the existence of a proper reporting restriction or permission order. It is not itself a reporting restriction or permission order.

71. Counsel shall agree the terms of the reporting order which I have made.

______________________________

APPENDIX

The calculation of E

1. The exigible income (E) is calculated by taking F’s gross earned income as disclosed in his most recent P60 or tax return and making the following adjustments to it.

i) First, it is to be reduced by reference to the number of other children living in his household. This is stipulated in the statutory formula. If there is one child the reducing factor is 11%; if there are two it is 14%; if there are three or more it is 16%.

ii) Next, F’s relievable pension contributions currently being made are to be annualised and deducted. This is also stipulated in the statutory formula.

iii) I agree with Mr Finch that there should be further subtracted the grossed-up school fees currently being paid by F. The grossing-up is done by taking the figure for the school fees paid by F and dividing it by 0.55. Thus if the fees are £30,000 the grossed up figure is £54,545. The justification for doing this is that it would not be reasonable or fair to apply the formula to that part of the father’s gross income which is, after tax, spent on the children’s school fees.

2. The child support scheme seeks to establish a figure for gross weekly income on the effective date, which is the date on which the application is made. The evidence used will always be that closest in time to the effective date, although for some pieces of evidence, such as accounts filed with a self-assessment tax return, may be well over a year old.

3. For the algebraically minded the algorithm is:

E = (G x (1-Z)) - P - (S ÷ 0.55)

Where:

G is the father’s gross income as disclosed in his most recent P60 or tax return.

Z is the reducing factor referable to the number of children living in the father’s household. The factors are 0.11 (one child in his household), 0.14 (two such children) and 0.16 (three such children).

P is the amount of pension payments currently being paid.

S is the amount of school fees and extras currently being paid.

The results from the application of the formula unadjusted

4. Table 1 below shows the results that would be produced if the formula were to be applied unadjusted to exigible incomes from £156,001 to £650,000.

5. It can be seen that at £156,000 the formula gives a figure for a single child of £15,300 which is 50% more than the figure for a child in a sibling duo (£10,200) and 82% more than a child in a sibling trio (£8,400). These relative proportions are almost exactly the same at every level of income. They are not realistic. Further, the figures overall are not consistent with the levels of award typically made for incomes in this range.

Adjusting the formula

6. Clearly the absolute and relative amounts calculated in respect of an exigible income of £156,000 cannot be changed, as these have been determined by statute.

7. At the other end of the spectrum, I consider that for an exigible income of £650,000 a reasonable figure of CSM for each of two children would be about £25,000. A single child would cost more, perhaps £27,000 (an 8% increase). A family unit with three children would have the benefit of economies of scale and the sharing of indirect costs suggesting that the figure for such a child should be in the region of £23,000 (a saving of 8% compared to the two-child family).

8. These figures all fall to be adjusted where there is shared care (see below).

9. To attain these results the following adjustments must be made to the operation of the formula in this range:

i) First, the results are taken for one-, two-, and three-children families reached by applying the formula to an income of £156,000. As explained above, the figures are respectively £15,300, £10,200 and £8,400.

ii) Second, those figures are augmented by the product of a tariff applied to the exigible income above £156,000 up to £650,000. The tariff is 2.4% for a single child and 3% for each of two or three children. The reason for the slightly lower rate for a single child is that the formula produces the disproportionately high figure of £15,300 for such a child, and it is that figure which is the base for the secondary augmentation.

10. Where E is £650,000 the result of this exercise is £27,100 for a single child, £25,000 for each of two children, and £23,200 for each of three children. These figures all appear to me to be extremely reasonable and typical of the sort of awards which might be made against a father earning at this level. I have noted that in CMX v EJX (French Marriage Contract) where the father’s most recent total annual compensation was $3 million, Moor J awarded £25,000 p.a. for one relevant child aged 17.

The CSSP

11. If E is £156,000 or less then the court should simply apply the formula (subject to the appropriate reduction for shared care (see below)) to produce the Child Support Starting Point (CSSP) for such a case.

12. If E is more than £156,000, but less than £650,000, then the CSSP is the figure taken from Table 2 below using the cohort which corresponds to the applicable level of shared care. That level is determined by the number of nights per annum the children spend with the father as follows:

|

Nights p.a. with F |

F’s level of shared care |

Cohort to use |

|

<52 |

Nil | |

A |

|

52–103 |

1/7th |

B |

|

104–155 |

2/7ths |

C |

|

156– 175 |

3/7ths |

D |

|

176 - 183 |

Equal |

E |

| | | |

13. E should be rounded to the nearest figure offered for it in the table Thus, if E is calculated as £370,000, the figure of £375,000 should be used .

Anomalies

14. It is true that there remain some anomalies. For example, a father earning £156,000 and paying £20,000 in school fees for two children (but making no relievable pension payments) will have his maintenance liability calculated by the SoS, who will not take into account the school fees, at £10,200 per child. He will thus be paying overall (£10,200 x 2) + £20,000 = £40,400. By contrast, an otherwise identical father earning £157,000 but paying the same £20,000 in school fees for two children, can expect the court to calculate his E as £157,000 - (20,000 ÷ 0.55) = £120,636 giving rise to a maintenance liability of £8,000 per child. That latter father will be paying overall £8,000 x 2 + £20,000 = £36,000. He will be paying £4,400 less than the first father, even though the fathers have virtually identical incomes.

15. This difference arises because of the different treatment of school fees. The statutory formula used by the Secretary of State as applied to earnings of £156,000 does not allow the deduction of a penny of school fees. By contrast I have suggested that in those cases where the court is making the decision it is only fair that the grossed up value of the school fees is deducted from the father's gross income as it would be unjust that he should be mulcted with a child support liability in respect of that element of his gross income which he will use, after tax, to pay school fees.

16. Other anomalies arise where the actual amount of shared care is very close to the boundary between two cohorts of shared care. So, for example, if two children spend 175 nights a year with their father, who earns £500,000 p.a, the maintenance liability will be £11,700 per child (calculated using the figures in Cohort D). But, if they spend just one more night each year with their father, then Cohort E’s figures are to be used giving rise to a liability of £9,500 per child. The difference caused by just one extra night is £4,400.

17. Differences like this look arbitrary, but they are a feature of any system that applies different rates to different categories. In R (Carson and Reynolds) v Secretary of State for Work and Pensions [2005] UKHL 37, [2006] 1 AC 173, Ms Reynolds complained that because she was under the age of 25, she was paid jobseeker's allowance and then income support at the reduced rate of £41.35 a week instead of the full rate of £52.20. She argued that this was unlawful age discrimination in breach of Article 14 of the European Convention on Human Rights. In his opinion rejecting this contention Lord Hoffmann stated at [41]:

“Mr Gill emphasised that the 25th birthday was a very arbitrary line. There could be no relevant difference between a person the day before and the day after his or her birthday. That is true, but a line must be drawn somewhere. All that is necessary is that it should reflect a difference between the substantial majority of the people on either side of the line. If one wants to analyse the question pedantically, a person one day under 25 is in an analogous, indeed virtually identical, situation to a person aged 25 but there is an objective justification for such discrimination, namely the need for legal certainty and a workable rule.”

18. In R(RF) v Secretary of State for Work and Pensions [2017] EWHC 3375 (Admin) at [57] I put it this way:

“I accept entirely that when a formulaic system for assessing needs and thus entitlements is introduced there will be some hard, arguably unfair, results particularly for those cases near the frontiers of descriptors or thresholds.”

19. So here. But here for the overwhelming majority of cases there are substantive differences between the cohorts in the amount of actual shared care of the children. The indicated figures are produced by a rule which is certain, workable and rational for each cohort. That eyebrows are raised for the figures produced by a few cases near the frontier of each cohort does not mean that the rule overall is irrational.

Summary

20. In a non-HECSA case the relevant CSSP is deduced as follows.

i) Where the application is to vary an existing order the CSSP is the value of the original order adjusted by the higher of the CPI or RPI index.

ii) Where the application is the original application and the father’s exigible income is no more than £156,000 then the CSSP is the formula result, reduced to reflect shared care.

iii) Where the application is the original application and the father’s exigible income is more than £156,000 but less than £650,000 then the CSSP is the figure derived from Table 2 using the cohort that corresponds to the level of shared care. Interpolations of E will give an acceptable result.

iv) E is calculated in accordance with the rules in para 1 above.

v) Where

· the original application is for four or more children; or

· E is greater than £650,000; or

· F’s income is largely unearned; or

· F has no income and lives on capital,

then no CSSP should be used and the child maintenance should be worked out from first principles applying s. 25(3) Matrimonial Causes Act 1973 or para 4(1) of Schedule 1 of the Children Act 1989.