FIRST-TIER TRIBUNAL

TAX CHAMBER INCOME TAX - late appeal to HMRC –permission to extend the time in which to appeal - whether reasonable excuse -whether proportionality of penalties in comparison to the amount of tax amounted to special circumstances - appeal dismissed

|

FIRST-TIER TRIBUNAL

TAX CHAMBER

|

|

Appeal number: TC/2019/01275

|

BETWEEN

SIMON

CLARKE Appellant

- and -

THE COMMISSIONERS FOR

HER MAJESTY’S Respondents

REVENUE

& CUSTOMS

|

TRIBUNAL:

|

JUDGE Jennifer TRIGGER SUSAN STOTT

|

Sitting in public at Manchester Tribunals

Service Tax, Alexandra House, 14-22 The Parsonage M3 JA on 08 August 2019

The Appellant was not present

Victoria Halfpenny Solicitor for HM Revenue and

Customs for the Respondents

DECISION

By letter, undated, received by the respondents on

04 June Mr Simon Clarke notified the Tribunal that he would not be attending

the Tribunal hearing. The Tribunal decided to proceed with the appeal hearing

in the absence of Mr Clarke because it was satisfied that there was sufficient

information in the appeal papers before the Tribunal to proceed; that there was

no information before the Tribunal to suggest that there were issues of

vulnerability that would make it unfair to proceed in the absence of Mr Scott; that

there had been a clear expression by Mr Scott to proceed in his absence. The

Tribunal considered the Tribunal Procedure (First- tier Tribunal) (Tax Chamber)

Rules 2009 and the overriding objective and the parties obligation to

co-operate with the Tribunal. The delays inherent in adjourning the hearing and

the proportionality of adjourning in relation to Mr Scott and other appellants

and the respondents were also factors relied on by the Tribunal in reaching its

decision to procced to hear the appeal in the absence of Mr Scott.

1. Simon

Clarke, ”the appellant”, appealed against penalties that the respondents,

(HMRC), imposed under Schedule 55 of the Finance Act 2009 (“Schedule 55 “) for failure

to submit a annual self-assessment return on time for the tax years 2010-11; 2011-12;

2012-13 and 2013-14.

2.The penalties that have been charged can be

summarised as follows:

2010-11

(1) £100.00 late filing

penalty under paragraph 3 of Schedule 55 imposed on 14 February 2012,

(2) Late filing “daily”

penalties totalling £900.00 under paragraph 4 of Schedule 55 imposed on 07

August 2012,

(3) A £300.00 “six” month

late filing penalty under paragraph 5 of Schedule 55 imposed on 07 August 2012.

2011-12

(1) A £100.00 late filing

penalty under paragraph 3 of Schedule 55 imposed on 12 February 2013,

(2) Late filing “daily”

penalties totalling £900.00 under paragraph 4 of Schedule 55 imposed on 14

August 2013

(3) A £300.00 six” month

late filing penalty under paragraph 5 of Schedule 55 imposed on 14 August 2013.

2012-13

(1) A £100.00 late filing

penalty under paragraph 3 of Schedule 55 imposed on18 February 2014,

(2) Late filing “daily”

penalties totalling £900.00 under paragraph 4 of Schedule 55 imposed on 18

August 2015,

(3) A £300.00 “six” month,

late filing penalty under paragraph 5 of Schedule 55 imposed on 18 August 2014,

(4) A £300.00 “twelve” month

late filing penalty under paragraph 6 of Schedule 66 imposed on 24 February

2015,

2013-14

(1) A £100.00 late filing

penalty under paragraph 3 of Schedule 55 imposed on 18 February 2015,

(2) Late filing “daily”

penalties totalling £900.00 under paragraph 4 of Schedule 55 imposed on 14

August 2015,

(3) A £300.00 “six” month

late filing penalty under paragraph 5 of Schedule 55 imposed on 14 august 2015,

(4) A £300.00 “twelve”

month late filing penalty under paragraph 6 of schedule 55 imposed on 23

February 2016.

The total penalties levied were £5,800.00.

3. The appellant’s grounds for appealing against the

penalties are set out in a letter to Her Majesty’s Courts and Tribunals Service,

(HMCTS), dated 20 January 2019 and can be summarised as follows:

(a) The appellant left

the UK 40 years ago;

(b) He took a contract to

work in Manchester for Jacobs Engineering;

(c) He started in

September 2011 and left in December 2013;

(d) He returned to the UK

in September 2014 and had a number of meetings with his accountants who

informed him that his tax returns were done;

(e) He has received

penalty demands for periods that he was not in the UK;

(f) The appellant

was not aware of the current legislation;

(g) He relied on his

accountants to do everything;

(h) The accountant failed

to submit the appellant’s self-assessment returns and the appellant was unaware

of that fact for a period of three years. This was because the appellant had

left the UK;

(i) Eventually

after many meetings with the accountants, after returning as a PAYE employee in

September 2014, the appellant’s zero tax accounts were issued in 2017.

(j) The

appellant accepts that the returns for the tax years, the subject of this

appeal, were submitted late. He asserts that the returns were late because all

the accountants and the CEO of the accountancy company had left after he had

been told and promised that the returns were done.

(k) The appellant has been

given the incorrect tax code and questions whether that fact will reduce the

penalties imposed.

The appellant did not

expressly claim that he had a reasonable excuse in the grounds of appeal

pleaded but the Tribunal determined that he had raised matters indicative that

a reasonable excuse was claimed.

4.On 27 March 2018 the appellant appealed to HMRC against

the penalties imposed by HMRC for the tax years ending 05 April 2013 and 05

April 2014.

5. By letter dated 12 July 2018 HMRC rejected that

appeal because the deadline for appealing had passed.

6.By letter dated 27 December 2018 HMRC notified

the appellant that HMRC could not accept his appeal against the penalties

charged for the years 2013-14, 2012-13, 2011-12 and 2010-11 because the

deadline for making an appeal had passed. HMRC advised the appellant of his

right to appeal to HMCTS and further advised that the appellant should write to

them by 26 January 2019. (Paragraph 21 of Schedule 55).

7. The appellant’s appeal to HMRC under section

39A of the Taxes Management Act 1970, (the “TMA 1970”), was made outside the

statutory deadline. HMRC refused to admit the late appeal on 12 July 2018 and also

on 27 December 2018 and issued to the appellant a notice rejecting the appeal

as late.

8. By letter dated 20 January 2019, received by

the Tribunal on 22 January 2019, the appellant appealed against the penalties

for failure to file on time, and also the refusal by HMRC to admit the late

appeal.

9. In their statement of case HMRC refused to

extend the deadline to serve the notice of appeal out of time under section

49(2) of the TMA 1970. The grounds for HMRC’s refusal are that the notice of

appeal, against each of the late filing penalties, was not received within 30

days of each penalty date. The last day to appeal the penalties detailed above

was as follows:

2010-11

LFP 14 March 2012 received 27 March 2018

DP 05 August 2012 received 27 March 2018

6MP 05 August 2012 received 27 March 2018

2011-12

LFP 13March 2013 received 27 March 2018

DP 12 September 2013received 27 march 2018

6MP12 September 2013 received 27 March 2018

2012-13

LFP 19 March 2014 received 27 March 2018

DP16 September 2014 received 27 March 2018

6MP 16 September 2014 received 27 March 2018

12MP 25 March 2015 received 27 March 2018

2013-14

LFP 19 March 2015 received 27 March 2018

DP 12 September 2015 received 27 March 2018

6MP 12 September 2015 received 27 March 2018

12MP 23 March 2016 received 27 March 2018

10. In deciding whether to extend the time limit

in which to file an appeal the Tribunal had regard to the three tier test laid

down in Martland v HMRC [2018] UKUT 178 namely to consider - the length

of the delay, the reasons for the delay and then to contrast the merits of the

reasons given for the delay against the prejudice which would be caused to both

parties by granting or refusing permission.

Length of delay

8. In Romasave (Property Services) Ltd v HMRC

[2015] UKUT 254 (TCC) it was stated that permission to appeal out of time

should only be granted exceptionally. It should be the exception rather than

the rule and it should not be granted routinely. Furthermore a delay of more

than three months was serious and significant.

9. The Tribunal found as a fact that the delay was

serious and significant. The Schedule below sets the number of days late:

2010-11 LFP 2203 days.

2010-11 DP 2028 days.

2010-11 6MP 2028 days.

2011-12 LFP 1839 days.

2011-12 DP 1656 days.

2011-12 6MP 1656 days.

2012-13 LFP 1468 days.

2012-13 DP 1287 days.

2012-13 6MP 1287 days.

2012-13 12 MP 1097 days.

2013-14 LFP 1103 days,

2013-14 DP 926 days,

2013-14 6MP 926 days.

2013-24 12MP 733 days.

Reasons for the delay

10. The appellant relied on the grounds of appeal

cited above as the reasons for the delay. HMRC could not accept that there was

a reasonable excuse shown either for the failure to file the returns by the due

date or in the alternative for the failure to file without undue delay after

the reasonable excuse had expired. It was the view of HMRC that the appellant

had failed to act with due diligence and had not demonstrated any form of

control over his accountants.

11 The appellant had failed to inform HMRC of a

change of circumstances, namely that he had left the UK. Reminders, penalty

notices, statements and request for payment were served on the appellant at the

address held for the appellant by HMRC as notified to HMRC by the appellant.

None of those documents were returned to HMRC under the returned mail service

provided to HMRC by the Royal Mail. They were therefore deemed to have been

served on the appellant under Part XI section 115 of the Taxes Management Act

1970. It follows that the documents were deemed also to have been served within

the ordinary course of postal delivery in accordance with section 7 of the

Interpretation Act 1978.

12 The appellant had failed to provide HMRC with

any change of address until 06 December 2016.

13. Furthermore, the appellant had not notified

HMRC until 27 March 2018 that Umbrella Accountancy Ltd were his accountants

which was not the action of a responsible taxpayer seeking to comply with his

legal obligation to submit timely tax returns.

14. The appellant accepted that the returns were

late and that he had taken no steps to ensure that the returns were submitted

on time.

15. The appellant had filed his return late in

each of the years, the subject of this appeal. The appellant admitted that he

did not understand the law but took no steps to appraise himself of the same or

to contact HMRC for help.

Prejudice to the parties in granting or refusing

permission

16. There was considerable prejudice to HMRC in

extending the time in which to appeal. The papers relating to the tax years

2010-11 and 2011-12 were likely to have been destroyed by HMRC either in their

entirety or in part in the normal course of business and in accordance with HMRC’s

various policies. This meant that HMRC would have difficulty in defending the

appeal for those tax years.

17. There would be prejudice to the appellant. He

would have to pay the penalties imposed. However, the appellant has already

paid a substantial amount of the outstanding penalties. There were no details

of any loan income to meet that liability before the Tribunal which could be an

option to meet the liabilities. In the alternative the appellant had the option

to arrange terms with HMRC to pay the outstanding penalties.

18. There was no prejudice to the appellant in the

fact that there was no tax payable. The penalties have been imposed because the

appellant failed to submit the returns on time. The penalties levied were fixed

by law and applied to all taxpayers. There was no discretion in either HMRC or

the Tribunal to alter those penalties save in express circumstances which are set

out in paragraphs 22 and 23 of Schedule 55. The penalties were not

disproportionate and those penalties had been correctly calculated and imposed

by HMRC for the late filing of the returns. The Tribunal considered the case

of Barry Edwards v HMRC [2019[ YKUT 0131 (TCC) which held that the mere

fact that a taxpayer had little tax liability for the relevant tax year does

not justify the reduction in the penalty on either the grounds of

proportionality generally or because of the presence of “special circumstances”.

The appellant had asked that the penalties be reduced because he had been

allocated an incorrect tax code.

18. HMRC

considered whether there were special circumstances which would warrant a special

reduction but found that there were none. The Tribunal found that the decision

of the HMRC was not flawed when considered in the light of the principles

applicable in proceedings by way of judicial review and in the light of the

decision in Barry Edwards referred to above. It followed therefore that

the Tribunal could not substitute its own decision for that of HMRC to reduce

the penalties. Accordingly, there was no prejudice to the appellant.

19. The Tribunal had to decide if there was a

reasonable excuse demonstrated by the appellant.

20. In order to reach a conclusion the Tribunal

considered the decision of the Upper Tribunal in Perrin v HMRC [2018] UKUT 156 (TCC) which Held that a Tribunal is required to deal with the following

issues when considering whether there is a reasonable excuse:

(a) Firstly,

establish what facts the taxpayer asserts give rise to a reasonable excuse. The

appellant relies on the contents of his notice of appeal to demonstrate a

reasonable excuse. The failure of the appellant’s accountants could not amount

to a reasonable excuse because the appellant had failed to exercise any control

or any adequate control over those accountants to prevent the delay. (Paragraph

23 Schedule 55). The delay in filing the returns was serious and significant.

( b) Secondly, decide which of those facts are

proven. All the facts are proved.

( c) Thirdly,

decide whether, viewed objectively, those proven facts do indeed amount to a

reasonable excuse. The appellant was intelligent and articulate as was evident

from the letter of appeal and the various letters in the appeal bundle. However,

a prudent and responsible taxpayer would have recognised the duty to require

his accountants to produce evidence that his tax returns for each of the tax

years in question had been filed. A diligent taxpayer would have maintained regular

contact with his accountant at least annually to ensure that his tax affairs

were being handled in accordance with the law. If the appellant had acted with

due diligence he would have discovered much earlier than he did that returns

had not been filed and he could have taken action to avoid any further delay

and the continued accrual of penalties. The appellant had failed to act as a

responsible taxpayer. He had failed to notify HMRC of his change of address,

contact number or email until after the penalties had accrued. Furthermore, the

appellant had failed also to make contact or keep any contact with HMRC during

the period of default in the relevant tax years and thereby failed to comply

with his legal responsibility to file the returns on time.

(d) Fourthly, having decided when any reasonable

excuse ceased. No reasonable excuse having been demonstrated by the appellant

the Tribunal did not consider this point.

28 The time limit imposed in which to file an

appeal was to provide finality in proceedings. There would be no finality if

the time limit were extended and HMRC would be prejudiced to a far greater

extent that the appellant.

29. The Tribunal relied on the following cases

pleaded by HMRC:

Martland v HMRC [2018] UKUT 178 which

established the three tier test to be considered by a Tribunal to determine the

lateness of an appeal.

Romasave (Property Services) Ltd v HMRC [2015] UKUT 254 (TCC) which found a delay of more than three months in submitting

an appeal is serious and significant. Permission to admit a late appeal should

be the exception rather than the rule.

The Clean Car Co ltd (1991) was cited but

the Tribunal relied on the case of Perrin referred to above which

established the test to determine whether a reasonable excuse has been shown on

both a subjective and an objective test.

30. For the reasons given in the body of this

judgment the Tribunal refused to extend the time in which to file the appeal. (Section

49(2) TMA)

31. Accordingly, the penalties totalling £5,800.00

are due and payable by the appellant and remain outstanding for the tax years

2010-11, 2011-12, 2012-13 and 2013-14.

Right to apply for permission to appeal.

32. This document contains full findings of fact and

reasons for the decision. Any party dissatisfied with this decision has a

right to apply for permission to appeal against it pursuant to Rule 39 of the

Tribunal Procedure (First-tier Tribunal) (Tax Chamber) Rules 2009. The

application must be received by this Tribunal not later than 56 days after this

decision is sent to that party. The parties are referred to “Guidance to

accompany a Decision from the First-tier Tribunal (Tax Chamber)” which

accompanies and forms part of this decision notice.

JENNIFER

TRIGGER

TRIBUNAL

JUDGE

Release

date: 16 September 2019

APPENDIX

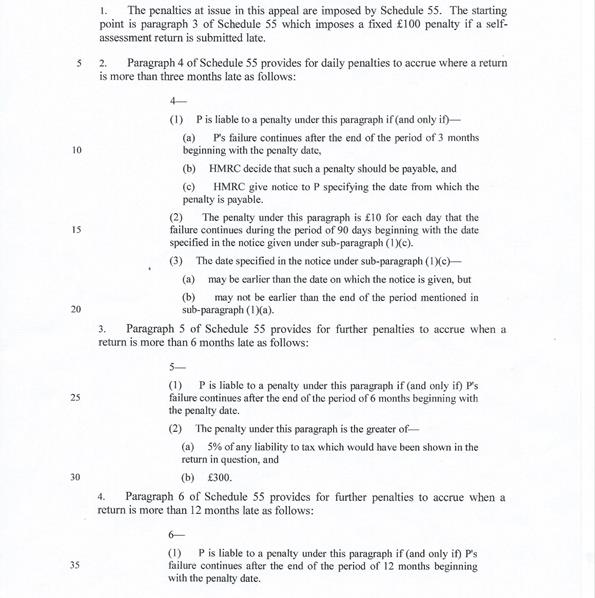

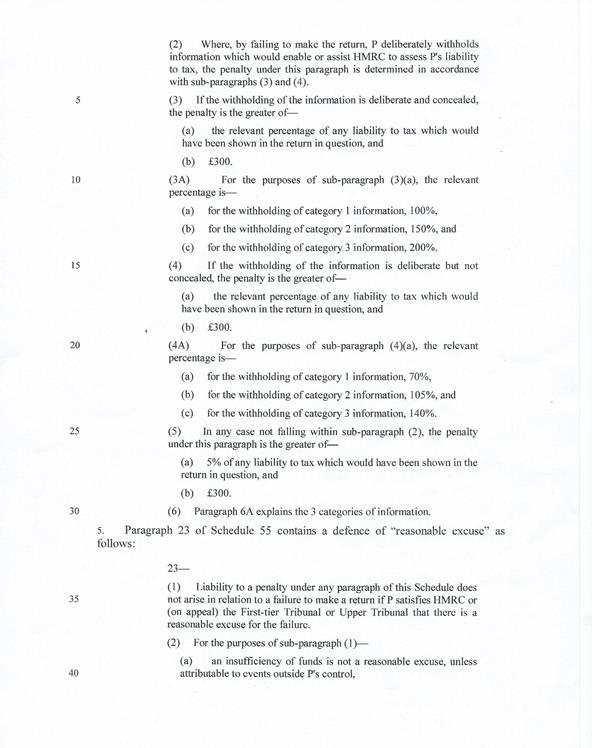

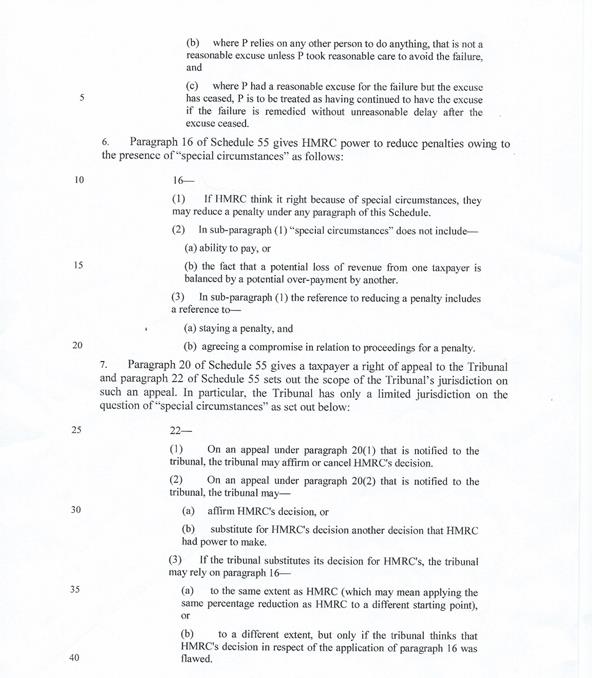

Relevant provisions

of Schedule 55 of the Finance Act 2009