This can mean a discovery of race, sexuality, or perhaps unfulfilled dreams.

More distressingly at a macro level the journey towards individual identity

may fuel nationalistic politics and territorial disputes (Bastow and Martin

2003, p 93). On one level the search for identity can generate a certain amount

of excitement for the individual, on another it can cause a good deal of pain

and consternation we should never be too sure about what we think we are

because it could easily happen that, at that precise moment, we are, in fact,

something completely different (Saramago 2002, p 98) . It places the individual

in a position of making choices and decisions in a world in which the opposing

diametric of flexibility or uncertainty, depending on ones situation, reign

supreme. This is illustrated by the material I present in the next section.

Thus far I have sought to demonstrate that occupational pensions have always

played an important role in state planning around retirement. Post 1997 policy

maintains this and seeks to spread the gospel of occupational provision through

stakeholder pensions. Despite the failure of this policy it is clear that

the intention is that individuals are to become lifestyle managers rather

than passive subjects (Deacon 2002). Choice is compelled for individuals and

there will be serious consequences for those who do not make the right choice.

Individual choice is dependant on the volunteerist nature of the firms that

employ them. As the legislative structure that surrounds pensions currently

exists firms can simply decide to close their defined benefit schemes and

offer a defined contribution schemes instead. Individuals then move, through

no choice of their, from the certainty of a final salary scheme to the uncertainty

of individualised market return.

In simple terms in a defined benefit scheme the risk of losses and surpluses

accrues to the scheme sponsor, the employer, in a defined contribution scheme

the amount that has to be saved to achieve a particular income on retirement

has to be decided upon by the individual. Defined benefit schemes are not

entirely risk free for the employee. There is a possibility of under-funding

or of firm insolvency. The recent intervention of the Parliamentary Ombudsman

(TSO 2006) demonstrates both that these risks exist and that the consequences

of their occurrence is often catastrophic for the individual (Ring 2005, Hyde

and Dixon 2004) but I would suggest that they pale considerably as risks when

placed next to the decisions that an individual has to make when in a defined

contribution scheme. There are two decisions. First what income will be necessary

on retirement to attain the desired standard of living and second what investment

pattern to choose in order to generate this income. Given the dependence of

retirement welfare provision on the occupational pension system it seems strange

or perhaps even negligent of the present administration not to intervene to

stem the tide of change that has been sweeping occupational pensions, the

converse of this is that intervention by the state takes away the element

of individual choice, that itself rests on the assumption that the individual

is in a position to make this choice.

Additionally the move from defined benefit to defined contribution schemes

has the potential to reconfigure shareholder capitalism. The creation of a

class of worker/shareholders goes to the heart of the debates about short-termism

and shareholder-driven notions of value (Fung et al 2001). It raises the question

of in whose interests institutional investors operate and to whom they are

accountable (Ghilarducci et al 1997). The traditional analysis of the firm

sees the employment interest categorised as one that is exposed to risk as

a fixed claimant for wages only and as one that has no other claims of immediate

substance outside the employing firm. This is contrasted with shareholders

who are seen as residual claimants exposed to risk across the market place.

Defined contribution plans in particular expose employees to the risk of market

performance in relation to their diversified portfolio thus eliding the difference

in interests. This too is the beginning of another story but in the context

of this paper it serves to point how fundamental occupational pension provision

not only to post retirement income but also to capital market structure and

behaviour (Proffitt and Spicer 2006).

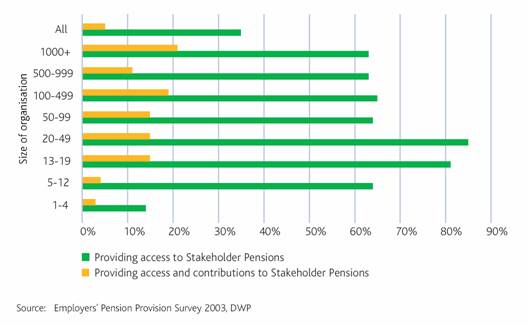

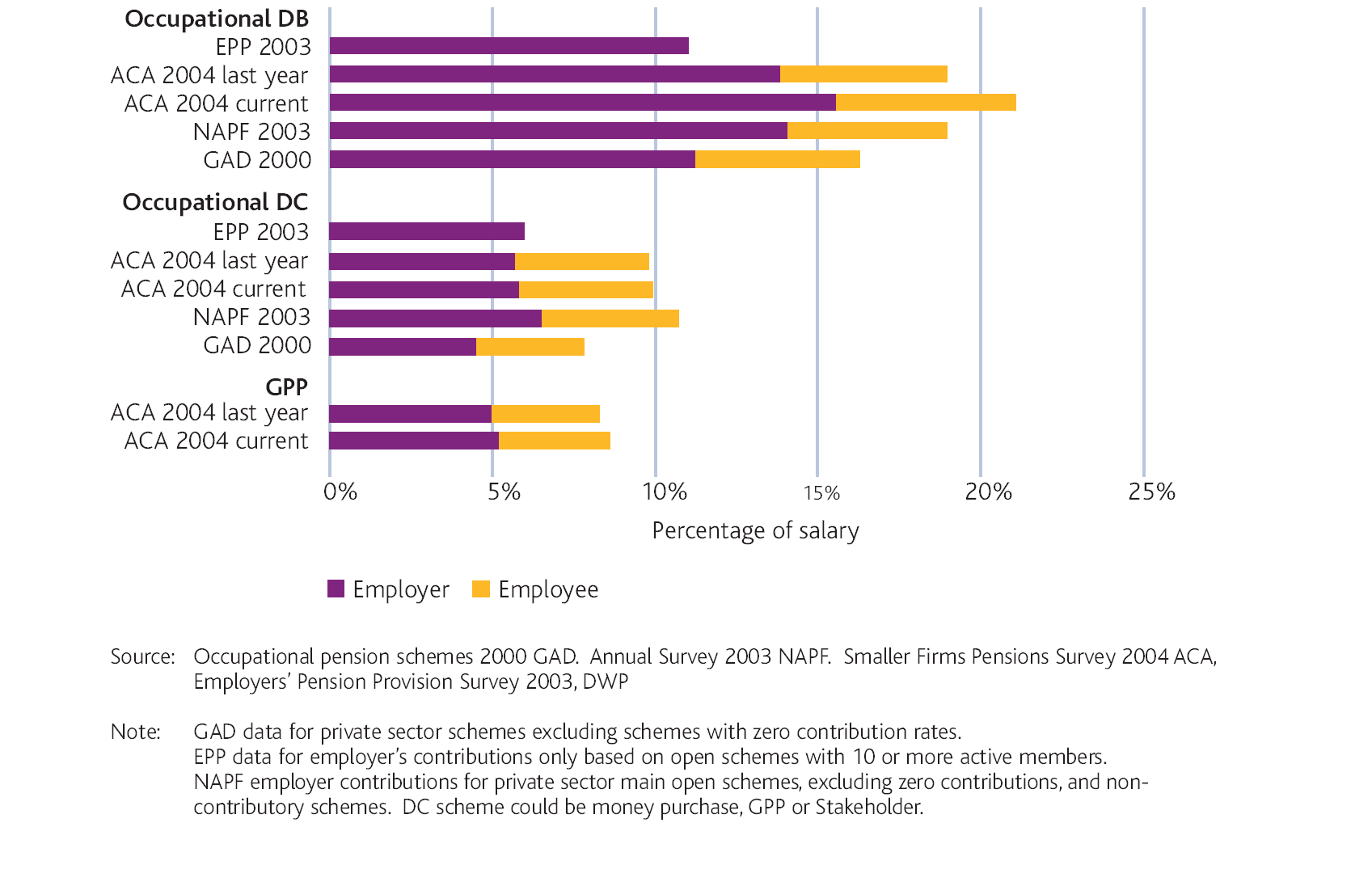

The figures below (6 and 7) make it clear that employers have used the move

from defined benefit schemes to defined contribution schemes as an opportunity

to reduce their contribution to post retirement provision. Employees are also

making substantially smaller pension contributions in the era of defined contribution

schemes than they were when defined benefit schemes were the norm. The effect

of this is that there is a much smaller amount of contribution capital accruing

to each individuals pension plan from which retirement income must be generated.

This creates a knock-on effect of future dependency on state welfare provision.

Figure 6 Contribution rates of Employers and Employees to Occupational Pension

Schemes

Figure 7 Average Contribution Rates by Scheme Type

The Trajectory of the Switch from Defined Benefit to Defined Contribution

The years from 1995 onwards have seen a large drop in the numbers of open

defined benefit schemes in the private sector and a consequent rise in the

number defined contribution schemes. (See the First Report of the Pensions

Commission issued in October 2004; Pensions: Challenges and Choices. The annex

to chapter three of the report suggests that there has been a 60 per cent

drop in defined benefit schemes since 1995 and predicts a potential further

fall of 20 per cent.) If we quantify the level of change uses the figures

provided by the Government Actuary Service we get the following picture:-

In 1995 there were 5.2 million people contributing to private sector DB

schemes

5 million of these were in open schemes and 0.2 million were in closed schemes.

In 2000 there were 4.6 million people contributing to private sector DB schemes

4.1 million of these were in open schemes, 0.5 million in closed schemes.

On GADs own figures then this implies a closure rate for Defined Benefit

schemes of 16 per cent between 1995 and 2000. It seems that the closure rate

for defined benefit schemes has gathered pace since 2000. There have been

numerous surveys, all using slightly different methods of calculation, that

point to this. While the exact figures reported by each may not be the most

robust the general trend that they illustrate is the following:-

Pensions Commission survey of FTSE350 company accounts to year end 2002

60 per cent of active DB scheme members were in closed schemes

Employers Pension Provision Survey 2003 number of open DB schemes has

fallen 33 per cent between 2000 and 2003 (20 or more employees)

CBI/Mercer survey in 2004 suggests a 41 per cent DB schemes closure rate

to 2004 with a projected 10 per cent closure over the next year.

Figure 8 Defined Benefit and Defined Contribution Schemes by Establishment

Date and Number of Employees

(GAD 2004 data)

In addition the stories of pension fund closures in companies such as British

Telecom are filling publications such as the FT and the Economist on a fairly

frequent basis.

In the text above I have touched on two possible explanations for the decline

first in occupational pension participation and second for the movement from

defined benefit to defined contribution; changing industrial structures and

job mobility. There are other factors which, in common with these two, point

to external macro economic factors as being the reason for the switch. The

argument is this:- corporations realised that factors such as increasing life

expectancy of beneficiaries and the effect in terms of cost of regulations

such so those introduced by the Social Security Act 1985 on index linking,

the potential impact of the Pension Act 2004 and the protection fund for under-funded

schemes that it introduced (Cass 2005) left defined benefit schemes with promises

that could not be fulfilled. There are other regulatory factors that could

be cited here such as the introduction of new accounting standards for the

reporting of the funding arrangements for occupational pensions such as FRS

17 and changes to the corporation tax regime which altered the amount of tax

relief that could be applied to their funds dividends. If we add to this

the use of supposed pension surpluses to provide generous early retirement

provision during the recessions of the early 1980s and early 1990s and the

peaks and troughs of the equity market (Langley 2004) then it looks very much

as though the decision to switch scheme types is an informed decision made

for sound business reasons.

However when subjected to critical examination none of these economic factors

taken collectively or singularly would appear to provide a completely convincing

explanation. There has been a gradual increase in longevity over the last

twenty years. This is surely something that careful planning could have overcome.

The majority of schemes closures, as the figures tracking the switch set out

above demonstrate, have occurred post 2000 and yet the equity market was been

unstable throughout the 1980s and there was a crash in 1987 (Bridgen and Meyer

2005). This did not provoke mass scheme closure. Changing regulation of fund

accounting and the restructuring of taxation is not normally sufficient to

spark a radical change in behaviour. Research that has looked at the effect

of financial regulation on corporate behaviour has shown that corporations

invest in developing avoidance tactics and devising evasive compliance strategies

(McBarnet 1984 and McBarnet and Whelan 1991). Anecdotal evidence from Towers

Perrin (Towers Perrin 2004), a large business support enterprise offering

services from corporate investment consultancy to human resource management

consultancy, indicates that the impact of FRS17 was a factor in switching

schemes for only 24per cent of the employers surveyed.

The clustering of scheme closures could be explained by herd behaviour (Banerjee

1992). While the actual modelling of herd behaviour may belong within micro-economics,

at a conceptual level its tools for understanding imitation in firms are relatively

straightforward (Lieberman and Asaba 2006). Two broad categories of explanation

exist within the literature information based theories of imitation and

rivalry based theories of imitation. Information based theories suggest that

firms follow other firms that they perceive, rightly or wrongly, to possess

superior information and rivalry based theories suggest that firms follow

each other either to respond to or to limit competition. These two categories

do not necessarily work in isolation and imitation behaviour may occur as

a combination of both information and competition. The rise and fall of the

dot.com bubble is a very good example of imitation behaviour that draws on

information and rivalry. Many businesses rushed to join the world of internet

based business only to find that this was an innovation that was not suitable

for their product. Their enthusiasm was based on following others and competing

in innovation. Within this paradigm there are fashion leaders; those firms

who it is supposed have superior information (Bikhchandani et al 1998) based

on size or longevity in the market.

If we consider imitation or herd behaviour in relation to pension schemes

then emerging as fashion leaders are those long established and large PLCs

and other bodies that closed their defined benefit schemes to new entrants

in the late 1990s, for example Sainsburys, the Abbey National and Age Concern.

Crucial to imitation are informal contact situations through which Information

can cascades. Information cascades when fashion is followed without recourse

to personally held or acquired information (Hirshleifer and Teoh 2003). Informal

networks and contacts between firms could exist in the medium of trade fairs,

trade associations and business dinners (Bridgen and Meyer 2005, pp 778-9).

A more significant source of informal contact is investment consultants. Figures

9 and 10 below demonstrate the value of pension fund assets and the relatively

small club of investment consultants that act as advisors to scheme trustees

(Kakabadse and Kakabadse 2004, pp 14-15). Just four firms provide investment

consultancy advice to 70 per cent plus of funds with assets of over £25 million

pounds. The Towers Perrin survey (Towers Perrin 2004) reports that 39 per

cent of employers surveyed switched their pension scheme to match trends in

the market ie among other firms.

Figure 9 Pension Fund Assets as a percentage of GDP

Figure 10 Market Share for Pension Advisers, by size of Pension Scheme (%)

1999

(Myners Report 2001, p 65)

Given the information produced by the Myners Report (Myners 2001, p40) on

the lack of training given to pension fund trustees, a position not unique

to the UK (Conley and OBarr 1992), it seems likely that the trend in switching

from defined benefit to defined contribution schemes is driven by the advice

of a small number of investment consultants. The only consolation in this

is that decisions made as a result of herding are fragile and liable to reversal

on the receipt of negative signals (Bikhchandani et al 1992). One such negative

signal could be a change in investor behaviour as a result of pension fund

capitalism (Ring 2003, p 73).

In the era of defined contribution occupational pension schemes investor

activism is dependant upon the financial literacy of the individual. The need

for financial literacy has its first impact in relation to individuals in

defined benefit contribution schemes in the decision around how much of their

present salary to put into the various options offered by their scheme to

produce a viable retirement income. An individual employee needs to know how

much income will be required in retirement years to maintain a particular

living standard. The various options available within the scheme have to be

evaluated and then monitored continuously against performance. Individuals

have to be able to make decisions about whether to opt for long-term investment

growth or higher short-term return (Byrne 2004). These decisions require a

life plan and an idea of risk evaluation about events in the life course,

such as how long children will be financial dependant for, the likelihood

of early death or job loss, and about other financial issues such as mortgage

finance and repayment. The advantage of a defined benefit scheme is that while

these life course events may still occur the one (almost, see text above on

insolvency and under funding risks) certainty is the level of lump sum available

on retirement and income levels thereafter.

This idea of individuals being exposed to risks, their calculations of

these risks, the extent to which certain responses to risk should be encouraged

through public policy and the assumptions that policy makers make about attitudes

to risk is part of a much larger debate within the fields of social policy

(Taylor-Gooby 1998, 2000) and increasingly behavioural economics (Bernartzi

and Thaler 2002). There are two related points to be made here. One is to

point out that despite its apparent discovery of behavioural economics and

the effect that it has on models of personal saving in May of this year (DWP

2006), the present Government has funded much of the work in the UK (all cited

in Rowlingson 2002), that has highlighted the poor choices that are made by

individuals in relation to savings and vehicles for saving in recent years.

The second is to summarise this work.

Rowlingson (2002) draws together this work which is both qualitative and

quantitative. It provides an evidence base for much that we might have thought

already from anecdotal evidence. It seems that within the life cycle a three

stage process exists in relation to financial planning. For those in their

20s and early 30s current consumption is the most pressing financial objective,

the next stage involves prioritising mortgage payments. Only from late 40s

onwards is pension planning and finance an issue. This would suggest that

minimum contributions only will be made to employer defined contribution schemes

until the final third of working life. If we add to this evidence on attitudes

to saving the evidence that individuals find not only the calculation of risk

difficult but the understanding of financial products and how these products

do or do not hedge particular risks or provide particular benefits (Burchardt

1997) then the position becomes more serious.

The majority of Individuals are not in a position to take advantage of the

welfare choices that are reposed in them. Occupational pensions could provide

a buffer for many people against the consequences of making the wrong choice

or no effective choice. State design of welfare provision has long been

conducted around the assumption that occupational schemes would provide the

majority of income for those eligible for them in retirement. This is no longer

the case. The move from defined benefit to defined contribution schemes exposes

individual employees to the risks of the market in a way not seen before.

Government seems reluctant to acknowledge this move or its consequences.

Banerjee, A (1992) A Simple Model of Herd Behavior 107 Quart J of Economics

797.

Banks, J and Emmerson, C (2000) Public and Private Pension Spending: Principles,

Practice and the Need for Reform 21 Fiscal Studies 1.

Bastow, S and Martin, J (2003) Third Way Discourse (Edinburgh: Edinburgh

Univ Press).

Beck, U (1994) The Reinvention of Politics: Towards a Theory of Reflexive

Modernization in Beck U, Giddens A, Lash S, Reflexive Modernization: Politics,

Tradition and Aesthetics in the Modern Social Order (Cambridge: Polity Press)

p 1.

Bernartzi, S (2002) How Much is Investor Autonomy Worth? 57 J of Finance

1593.

Bikhchandani, S et al (1992) A Theory of Fads, Fashion, Custom and Cultural

Change as Information Cascades 100 J Pol Econ 992.

Bikhchandani, S et al (1998) Learning from the Behavior of Others: Conformity,

fads and information cascades 12 J Economic Perspectives 151.

Black, J and Nobles, R (1998) Personal Pensions Misselling: The Causes

and Lessons of Regulatory Failure 61 MLR 789.

Blackburn, R (2002) Banking on Death (London: Verso)

Blake, D (2000) Two Decades of Pension Reform in the UK 22 Employee Review

223.

Bonoli, G (2003) Two Worlds of Pension Reform in Western Europe 35 Comparative

Politics 399.

Bridgen, P and Meyer, T (2005) When Do Benevolent Capitalists Change Their

Mind? Explaining the Retrenchment of Defined-benefit Pensions in Britain?

39 Soc Pol and Admin 764.

Budd, A and Campbell, N (1998) The Roles of the Public and Private Sectors

in the UK Pensions System in Feldstein M (ed) Privatising Social Security

(Chicago: Chicago Univ Press) page 99.

Burchardt, T (1997) What Price Security (London: London School of Economics)

Byrne, A (2004) Employee Saving and Investment Decisions in Defined Contribution

Plans: Survey Evidence from the UK The Pensions Institute Discussion Paper

PI-0412.

Clark, G The UK Occupational Pension System in Crisis www.ouce.ox.ac.uk/news/phclcs/Clark.pdf

Clark, G and Emmerson, C (2003) Privatising provision and attacking poverty?

The direction of UK Pension Policy under New Labour J of Pension Economics

and Finance 67

Conley, J and OBarr, W (1992) The Culture of Capital: An Anthropological

Investigation of Institutional Investment 70 NCL Rev 823.

Deacon, A (2002) Perspectives on Welfare (Buckingham: Open University Press).

Deakin, N (1987) The Politics of Welfare (London: Methuen).

Disney, R (1996) Can we afford to grow older? A perspective on the economics

of ageing (Cambridge: MIT Press).

Disney, R and Emmerson, C (2002) Choice of Pension Scheme and Job Mobility

in Britain IFS Working Paper 02/09 (London: Institute for Fiscal Studies).

DSS (1990) The Governments Expenditure Plans 1990-1 to 1992-93 Department

CM 1014, HMSO

Duncan, S and Williams, F (2002) New Divisions of Labour 22 Crit Soc Pol

5.

Esping Anderson, E (1999) Social Foundations of Post-Industrial Economics

(Oxford:OUP).

Field, F (1996) Stakeholder Welfare (London: Institute of Economic Affairs).

Finlayson, A (2003) Making Sense of New Labour (London: Lawrence and Wishart).

Fung, A et al (2001) Working Capital (Ithica: Cornell Univ Press).

Gall, G and McKay, S (1994) Trade Union Derecognition in Britain, 1988-1994

32 Brit J of Industrial Relations 433.

Giddens, A (1995) Beyond Right and Left (Cambridge: Polity Press).

Ghilarducci, T et al (1997) Labours Paradoxical Interests and the Evolution

of Corporate Governance 24 JLS 26.

Hannah, L (1986) Inventing Retirement (Cambridge: CUP).

OHiggins, M (1986) Public/Private Interaction and Pension Provision in

Rein, M and Rainwater, L (eds) Public/Private Interplay in Social Protection

(London: Sharpe) p 99.

Hirshleifer, D and Teoh, S (2003) Herd Behaviour and Cascading in Capital

Markets: a Review and Synthesis 9 European Financial Management 25.

Hyde, M and Dixon, J (2004) Working and Saving for Retirement: New Labours

reform of Company Pensions 24 Critical Social Policy 270.

Kakabadse, N and Kakabadse, A (2004) Pension Funds Governance: An Overview

of the Role of Trustees 1 Int J Business Gov and Ethics 3.

Langley, P (2004) In the Eye of the Perfect Storm: The Final Salary Pensions

Crisis and Financialisation of Anglo-American Capitalism New Political Economy

539.

Levitas, R (2001) Against Work: a utopian incursion into social policy

21 Crit Soc Pol 449.

Lewis, J (2001) The Decline of the Male Breadwinner: Implications for Work

and Care 8 Social Politics 152.

Lieberman, M and Asaba, S (2006) Why do Firms Imitate Each Other 31 Academy

of Management Review 366.

Mann, K (2005) Three Steps to Heaven? Tensions in the Management of Welfare:

Retirement Pensions and Active Consumers 35 Jnl Soc Pol 77.

McBarnet, D (1984) Law and Capital: The Role of Legal Form and Legal Capital

12 Int J of Soc of Law 231.

McBarnet, D and Whelan, C(1991) The Elusive Spirit of the Law: Formalism

and the Struggle for Legal Control 54 MLR 848.

Pierson, P (1995) Dismantling the Welfare State? Regan, Thatcher and the

Politics of Retrenchment (Cambridge: CUP).

Proffitt, W and Spicer, A (2006) Shaping the Shareholder Activism Agenda:

Institutional Investors and Global Social Issues 4 Strategic Organization

165.

Ring, P (2002) The Implications of the New Insurance Contract for UK

Pension Provision: Rights, Responsibilities and Risks 22 Critical Social

Policy 551.

Ring, P (2003) Risk and Uk Pension Reform 37 Soc Pol and Admin 65.

Ring, P (2005) Security in Pension Provision: A Critical Analysis of UK

Government Policy J of Soc Pol 343.

Rose, N (1999) Powers of Freedom (Cambridge: CUP).

Saramago, J (2002) The Cave (London: Harvill Press).

Sass, S (1997) The Promise of Private Pensions (Cambridge Mass: Harvard Univ

Press).

Skinner, C and Ford J, (2000) Planning, Postponing or Hesitating: understanding

financial planning (York: Centre for Housing Policy)

Taylor-Gooby, P (1998) Choice and Public Policy (Basingstoke: Macmillan)

Taylor-Gooby, P (2000) Risk, Trust and Welfare (Basingstoke: Macmillan)

Taylor-Gooby, P and Larsen T (2004) The UK-A Test Case for the Liberal

Welfare State? in Taylor-Gooby, P (ed) New Risks, New Welfare (Oxford: OUP)

55.

Waine, B (1995) A Disaster Foretold 29 Social Administration and Policy

317.

Wheeler, S (2006) Labour and the Corporation (2006) 6 Corporate Law Studies

(forthcoming).

Whiteside, N (2003) Historical Perspectives and the Politics of Pension

Reform in Clark, G and Whiteside, N (eds) Pension Security in the 21st Century

(Oxford: OUP).

Whiteside N (2006) Adapting private pensions to public purposes: historical

perspectives on the politics of reform 16 J of European Social Policy 43.

Beveridge Report 1942, p6-7

Pension Law Review Committee 1993

A New Contract for Welfare: Partnership in Pensions Cm 4179 (1998) HMSO London

New Ambitions for our country: a new contract for welfare (1998b) Cm 3805

TSO London

Institutional Investment in the United Kingdom (the Myners Review) 2001

Simplicity, security and choice: working and saving for retirement (2002)

TSO London

The Pickering Report A Simpler Way to Better Pensions: An Independent Report

(2002) DWP p29

House of Lords Select Committee on Economic Affairs 2003 Aspects of the

Economics of an Ageing Population vol 1

GAD 2004 Survey of Occupational Pension schemes

Pensions: Challenges and Choices Pensions Commission, October 2004

Towers Perrin Human Resources Services (2004) Defined Contribution Pension

Arrangements

A New Pension Settlement for the Twenty First Century Pensions Commission,

May 2005

Cass Business School, Pyrrhic Victory October 2005

Trusting in the Pensions Promise: Government Bodies and the Security of Final

Salary Occupational Pensions (March 2006) TSO HC 984

Security in Retirement: towards a new pension system (May 2006) DWP, TSO,

London Cm6841

[1] See for example

the Speech of Gordon Brown, Chancellor of the Exchequer, at the launch

of the Charity Bank, 17th October 2002. There Browns vision of Britain

included networks of local volunteers supplying services that were previously

supplied by the state. In 2004 Brown designated 2005 as the Year of the

Volunteer. Two of the aims of this initiative were to increase the number

of volunteers and increase the number of volunteering opportunities.